Advertisement

- South Korea

- /

- Entertainment

- /

- KOSE:A352820

High Growth Tech Stocks in South Korea for October 2024

Simply Wall St

Reviewed by Simply Wall St

The South Korean market has experienced a modest uptick, rising 1.3% over the last week and showing a 4.1% increase over the past year, with earnings expected to grow by 30% annually. In this environment, identifying high growth tech stocks involves focusing on companies that demonstrate strong innovation and adaptability to capitalize on these favorable conditions.

Top 10 High Growth Tech Companies In South Korea

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| IMLtd | 21.80% | 111.43% | ★★★★★★ |

| Seojin SystemLtd | 33.39% | 49.13% | ★★★★★★ |

| Bioneer | 23.53% | 97.58% | ★★★★★★ |

| NEXON Games | 29.64% | 66.98% | ★★★★★★ |

| FLITTO | 32.60% | 106.82% | ★★★★★★ |

| ALTEOGEN | 64.22% | 99.46% | ★★★★★★ |

| Devsisters | 29.08% | 63.02% | ★★★★★★ |

| Park Systems | 23.21% | 34.63% | ★★★★★★ |

| AmosenseLtd | 24.04% | 71.97% | ★★★★★★ |

| UTI | 114.97% | 134.60% | ★★★★★★ |

Click here to see the full list of 48 stocks from our KRX High Growth Tech and AI Stocks screener.

Let's dive into some prime choices out of from the screener.

ALTEOGEN (KOSDAQ:A196170)

Simply Wall St Growth Rating: ★★★★★★

Overview: ALTEOGEN Inc. is a biotechnology company that specializes in the development of long-acting biobetters, proprietary antibody-drug conjugates, and antibody biosimilars, with a market cap of ₩19.60 trillion.

Operations: ALTEOGEN Inc. generates revenue primarily from its biotechnology segment, amounting to ₩90.79 billion. The company focuses on developing innovative biotechnological products such as long-acting biobetters and antibody biosimilars.

ALTEOGEN, a South Korean biotech firm, is navigating a challenging yet promising landscape marked by robust growth forecasts. With revenue expected to surge by 64.2% annually, the company outpaces the broader KR market's growth rate of 10.5%. This aggressive expansion is underpinned by significant R&D investments, aligning with an industry shift towards more innovation-driven business models. Despite current unprofitability, ALTEOGEN is projected to pivot into profitability within three years, boasting an anticipated annual profit growth of 99.5%. Moreover, its strategic focus on specialized biotechnologies could position it advantageously as market dynamics evolve. While shareholder dilution has occurred over the past year, the potential for a high return on equity of 66.3% in the near future suggests a trajectory towards stronger financial health and shareholder value creation.

- Navigate through the intricacies of ALTEOGEN with our comprehensive health report here.

Gain insights into ALTEOGEN's past trends and performance with our Past report.

Celltrion (KOSE:A068270)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Celltrion, Inc., along with its subsidiaries, focuses on developing and manufacturing protein-based drugs for oncology treatment in South Korea, with a market capitalization of approximately ₩40.10 trillion.

Operations: Celltrion, Inc. generates revenue primarily from its Bio Medical Supply segment, which accounts for ₩3.54 trillion, followed by Chemical Drugs at ₩507.02 billion. The company focuses on developing and producing protein-based oncology drugs in South Korea.

Celltrion's strategic maneuvers, including a recent agreement with Cigna and Express Scripts for ZYMFENTRA®, underscore its growing influence in the biopharmaceutical sector. This partnership, poised to enhance access for 16.1 million insured individuals, dovetails with a robust R&D commitment that has seen expenses climb to significant figures, reinforcing its innovation trajectory. Moreover, Celltrion’s aggressive buyback strategy, repurchasing shares worth KRW 75.89 billion recently, reflects confidence in its operational direction and potential to enhance shareholder value amidst a challenging yet dynamic market landscape.

- Click to explore a detailed breakdown of our findings in Celltrion's health report.

Understand Celltrion's track record by examining our Past report.

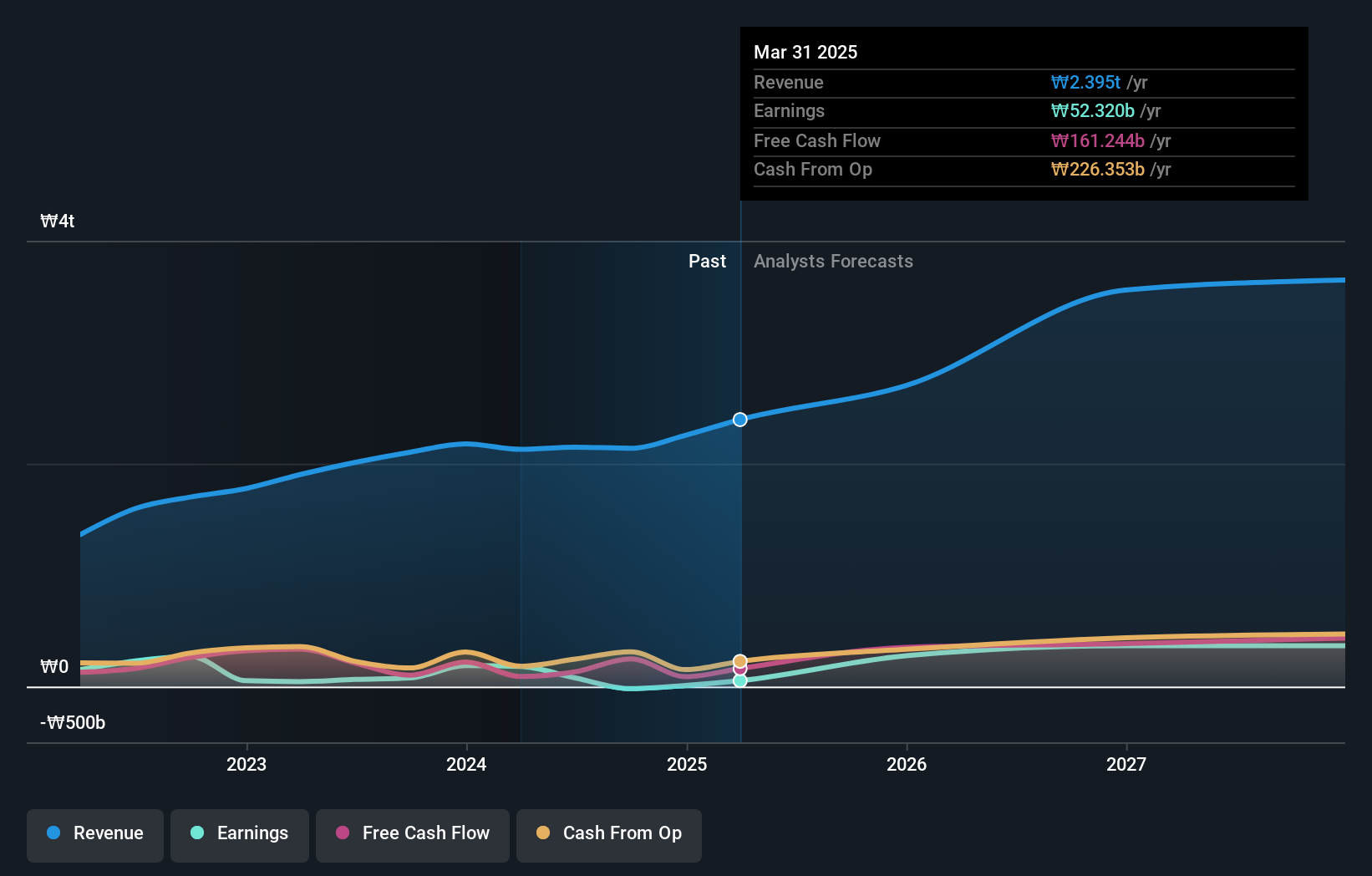

HYBE (KOSE:A352820)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: HYBE Co., Ltd. operates in music production, publishing, and artist development and management businesses with a market cap of approximately ₩7.44 trillion.

Operations: HYBE generates revenue primarily from its Label and Solution segments, contributing approximately ₩1.28 trillion and ₩1.24 trillion respectively, with additional income from its Platform segment at around ₩361.12 billion.

HYBE's recent strategic maneuvers, including a robust share repurchase program, underscore its confidence amid volatile markets; the company repurchased 150,000 shares for KRW 26.09 billion to stabilize stock prices. This move aligns with its solid earnings growth of 21.6% over the past year, surpassing the industry average of 7.3%. Moreover, HYBE is set to outpace market expectations with projected revenue and earnings growth at 14% and 42.2% per year respectively, supported by significant R&D investments that fuel innovation and competitiveness in the entertainment sector.

Seize The Opportunity

- Take a closer look at our KRX High Growth Tech and AI Stocks list of 48 companies by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HYBE might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A352820

HYBE

Engages in the music production, publishing, and artist development and management businesses.

Excellent balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|17.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|4.3% undervalued

RO

Community Contributor