- South Korea

- /

- Basic Materials

- /

- KOSDAQ:A225530

Bokwang Industry Co., Ltd.'s (KOSDAQ:225530) Stock On An Uptrend: Could Fundamentals Be Driving The Momentum?

Bokwang Industry's (KOSDAQ:225530) stock is up by a considerable 41% over the past three months. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to study its financial indicators more closely to see if they had a hand to play in the recent price move. Particularly, we will be paying attention to Bokwang Industry's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

Check out our latest analysis for Bokwang Industry

How Is ROE Calculated?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Bokwang Industry is:

11% = ₩11b ÷ ₩97b (Based on the trailing twelve months to September 2024).

The 'return' refers to a company's earnings over the last year. So, this means that for every ₩1 of its shareholder's investments, the company generates a profit of ₩0.11.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Bokwang Industry's Earnings Growth And 11% ROE

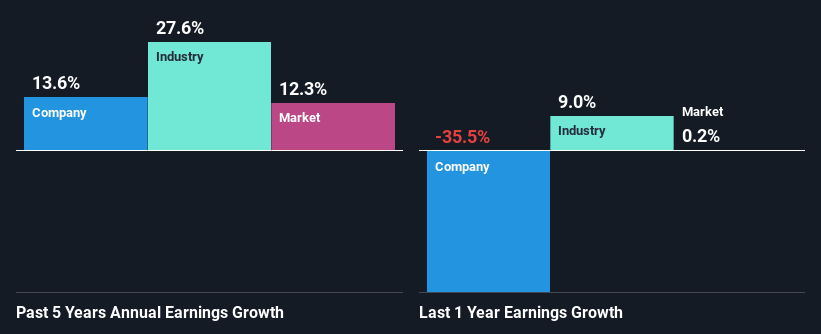

To begin with, Bokwang Industry seems to have a respectable ROE. On comparing with the average industry ROE of 7.4% the company's ROE looks pretty remarkable. Probably as a result of this, Bokwang Industry was able to see a decent growth of 14% over the last five years.

Next, on comparing with the industry net income growth, we found that Bokwang Industry's reported growth was lower than the industry growth of 28% over the last few years, which is not something we like to see.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Is Bokwang Industry fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Bokwang Industry Using Its Retained Earnings Effectively?

While Bokwang Industry has a three-year median payout ratio of 76% (which means it retains 24% of profits), the company has still seen a fair bit of earnings growth in the past, meaning that its high payout ratio hasn't hampered its ability to grow.

Additionally, Bokwang Industry has paid dividends over a period of three years which means that the company is pretty serious about sharing its profits with shareholders.

Summary

Overall, we feel that Bokwang Industry certainly does have some positive factors to consider. Its earnings have grown respectably as we saw earlier, which was likely due to the company reinvesting its earnings at a pretty high rate of return. However, given the high ROE, we do think that the company is reinvesting a small portion of its profits. This could likely be preventing the company from growing to its full extent. Up till now, we've only made a short study of the company's growth data. So it may be worth checking this free detailed graph of Bokwang Industry's past earnings, as well as revenue and cash flows to get a deeper insight into the company's performance.

Valuation is complex, but we're here to simplify it.

Discover if Bokwang Industry might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A225530

Bokwang Industry

Manufactures and sells aggregates, ascons, and ready mixed concrete in South Korea.

Excellent balance sheet and fair value.