Advertisement

If we're looking to avoid a business that is in decline, what are the trends that can warn us ahead of time? Typically, we'll see the trend of both return on capital employed (ROCE) declining and this usually coincides with a decreasing amount of capital employed. This reveals that the company isn't compounding shareholder wealth because returns are falling and its net asset base is shrinking. In light of that, from a first glance at Chemtros (KOSDAQ:220260), we've spotted some signs that it could be struggling, so let's investigate.

Return On Capital Employed (ROCE): What is it?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Chemtros:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

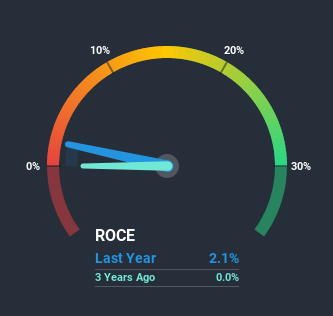

0.021 = ₩1.1b ÷ (₩68b - ₩15b) (Based on the trailing twelve months to June 2020).

Therefore, Chemtros has an ROCE of 2.1%. In absolute terms, that's a low return and it also under-performs the Chemicals industry average of 8.1%.

Check out our latest analysis for Chemtros

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Chemtros' past further, check out this free graph of past earnings, revenue and cash flow.

How Are Returns Trending?

We are a bit worried about the trend of returns on capital at Chemtros. To be more specific, the ROCE was 12% two years ago, but since then it has dropped noticeably. On top of that, it's worth noting that the amount of capital employed within the business has remained relatively steady. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. If these trends continue, we wouldn't expect Chemtros to turn into a multi-bagger.

Our Take On Chemtros' ROCE

All in all, the lower returns from the same amount of capital employed aren't exactly signs of a compounding machine. However the stock has delivered a 52% return to shareholders over the last three years, so investors might be expecting the trends to turn around. Regardless, we don't feel too comfortable with the fundamentals so we'd be steering clear of this stock for now.

If you're still interested in Chemtros it's worth checking out our FREE intrinsic value approximation to see if it's trading at an attractive price in other respects.

While Chemtros isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

When trading Chemtros or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KOSDAQ:A220260

Chemtros

Engages in the manufacture and sale of chemical intermediates, and applied materials and adhesives in South Korea.

Adequate balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor