Advertisement

- South Korea

- /

- Chemicals

- /

- KOSDAQ:A110020

With A 38% Price Drop For Jeonjinbio Co., Ltd. (KOSDAQ:110020) You'll Still Get What You Pay For

The Jeonjinbio Co., Ltd. (KOSDAQ:110020) share price has fared very poorly over the last month, falling by a substantial 38%. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 13% in that time.

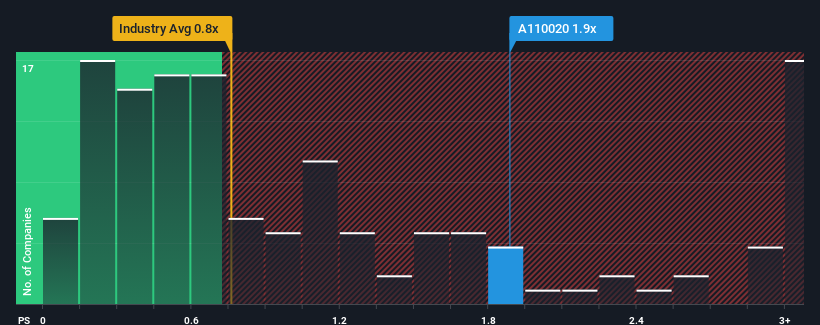

Even after such a large drop in price, when almost half of the companies in Korea's Chemicals industry have price-to-sales ratios (or "P/S") below 0.8x, you may still consider Jeonjinbio as a stock probably not worth researching with its 1.9x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

See our latest analysis for Jeonjinbio

How Jeonjinbio Has Been Performing

Jeonjinbio certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. It seems that many are expecting the strong revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Jeonjinbio will help you shine a light on its historical performance.How Is Jeonjinbio's Revenue Growth Trending?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Jeonjinbio's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 95% last year. This great performance means it was also able to deliver immense revenue growth over the last three years. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 30% shows it's noticeably more attractive.

In light of this, it's understandable that Jeonjinbio's P/S sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

What We Can Learn From Jeonjinbio's P/S?

Despite the recent share price weakness, Jeonjinbio's P/S remains higher than most other companies in the industry. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Jeonjinbio maintains its high P/S on the strength of its recent three-year growth being higher than the wider industry forecast, as expected. In the eyes of shareholders, the probability of a continued growth trajectory is great enough to prevent the P/S from pulling back. Barring any significant changes to the company's ability to make money, the share price should continue to be propped up.

Plus, you should also learn about these 4 warning signs we've spotted with Jeonjinbio (including 2 which don't sit too well with us).

If you're unsure about the strength of Jeonjinbio's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A110020

Jeonjinbio

Develops and produces natural bio-pesticides, alternative chemical products, and other biotechnology products.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor