Advertisement

- South Korea

- /

- Medical Equipment

- /

- KOSDAQ:A208370

What Do The Returns At SELVAS Healthcare (KOSDAQ:208370) Mean Going Forward?

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. With that in mind, we've noticed some promising trends at SELVAS Healthcare (KOSDAQ:208370) so let's look a bit deeper.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on SELVAS Healthcare is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.053 = ₩1.6b ÷ (₩46b - ₩16b) (Based on the trailing twelve months to September 2020).

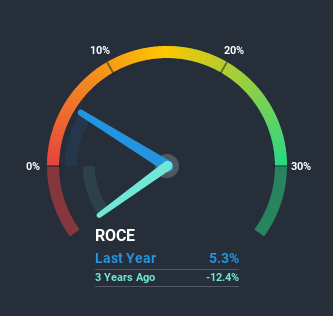

So, SELVAS Healthcare has an ROCE of 5.3%. Ultimately, that's a low return and it under-performs the Medical Equipment industry average of 13%.

See our latest analysis for SELVAS Healthcare

Historical performance is a great place to start when researching a stock so above you can see the gauge for SELVAS Healthcare's ROCE against it's prior returns. If you'd like to look at how SELVAS Healthcare has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

It's great to see that SELVAS Healthcare has started to generate some pre-tax earnings from prior investments. The company was generating losses four years ago, but now it's turned around, earning 5.3% which is no doubt a relief for some early shareholders. In regards to capital employed, SELVAS Healthcare is using 35% less capital than it was four years ago, which on the surface, can indicate that the business has become more efficient at generating these returns. This could potentially mean that the company is selling some of its assets.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. Effectively this means that suppliers or short-term creditors are now funding 35% of the business, which is more than it was four years ago. Keep an eye out for future increases because when the ratio of current liabilities to total assets gets particularly high, this can introduce some new risks for the business.The Key Takeaway

From what we've seen above, SELVAS Healthcare has managed to increase it's returns on capital all the while reducing it's capital base. Astute investors may have an opportunity here because the stock has declined 64% in the last three years. So researching this company further and determining whether or not these trends will continue seems justified.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 3 warning signs for SELVAS Healthcare (of which 1 is a bit concerning!) that you should know about.

While SELVAS Healthcare isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you’re looking to trade SELVAS Healthcare, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A208370

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|59.0% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|22.8% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|4.3% undervalued

RO

Community Contributor