Advertisement

- South Korea

- /

- Medical Equipment

- /

- KOSDAQ:A122310

Genoray Co., Ltd. (KOSDAQ:122310) Looks Interesting, And It's About To Pay A Dividend

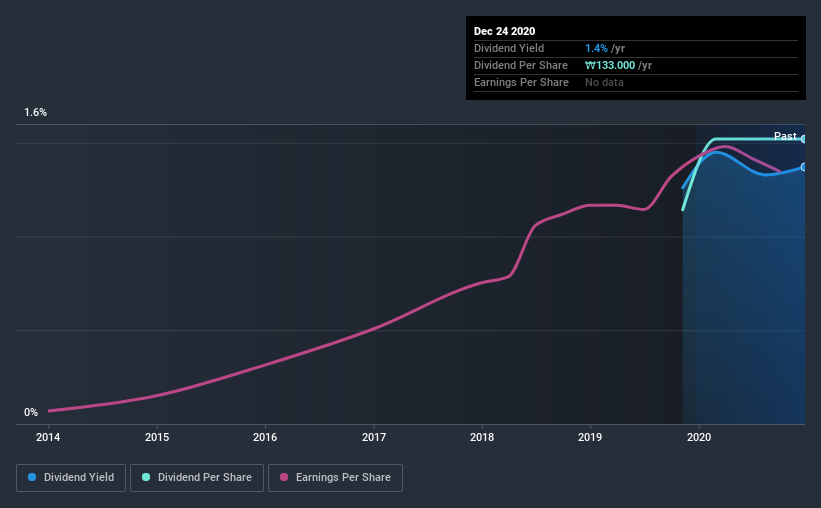

It looks like Genoray Co., Ltd. (KOSDAQ:122310) is about to go ex-dividend in the next three days. You will need to purchase shares before the 29th of December to receive the dividend, which will be paid on the 14th of April.

Genoray's next dividend payment will be ₩133 per share, and in the last 12 months, the company paid a total of ₩133 per share. Calculating the last year's worth of payments shows that Genoray has a trailing yield of 1.4% on the current share price of ₩9700. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. As a result, readers should always check whether Genoray has been able to grow its dividends, or if the dividend might be cut.

View our latest analysis for Genoray

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Genoray has a low and conservative payout ratio of just 14% of its income after tax. A useful secondary check can be to evaluate whether Genoray generated enough free cash flow to afford its dividend. Thankfully its dividend payments took up just 37% of the free cash flow it generated, which is a comfortable payout ratio.

It's positive to see that Genoray's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see how much of its profit Genoray paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings fall far enough, the company could be forced to cut its dividend. It's encouraging to see Genoray has grown its earnings rapidly, up 55% a year for the past five years. Genoray is paying out less than half its earnings and cash flow, while simultaneously growing earnings per share at a rapid clip. This is a very favourable combination that can often lead to the dividend multiplying over the long term, if earnings grow and the company pays out a higher percentage of its earnings.

Unfortunately Genoray has only been paying a dividend for a year or so, so there's not much of a history to draw insight from.

Final Takeaway

Has Genoray got what it takes to maintain its dividend payments? Genoray has been growing earnings at a rapid rate, and has a conservatively low payout ratio, implying that it is reinvesting heavily in its business; a sterling combination. There's a lot to like about Genoray, and we would prioritise taking a closer look at it.

In light of that, while Genoray has an appealing dividend, it's worth knowing the risks involved with this stock. Our analysis shows 2 warning signs for Genoray and you should be aware of them before buying any shares.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade Genoray, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A122310

Genoray

Engages in the research, development, manufacture, and sale of medical and dental x-ray devices in South Korea.

Adequate balance sheet and slightly overvalued.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

41 followersusers have followed this narrative

6 commentsusers have commented on this narrative

12 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8048.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

115 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

954 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative