Advertisement

- South Korea

- /

- Healthcare Services

- /

- KOSDAQ:A078160

Health Check: How Prudently Does MEDIPOST (KOSDAQ:078160) Use Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies MEDIPOST Co., Ltd. (KOSDAQ:078160) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is MEDIPOST's Debt?

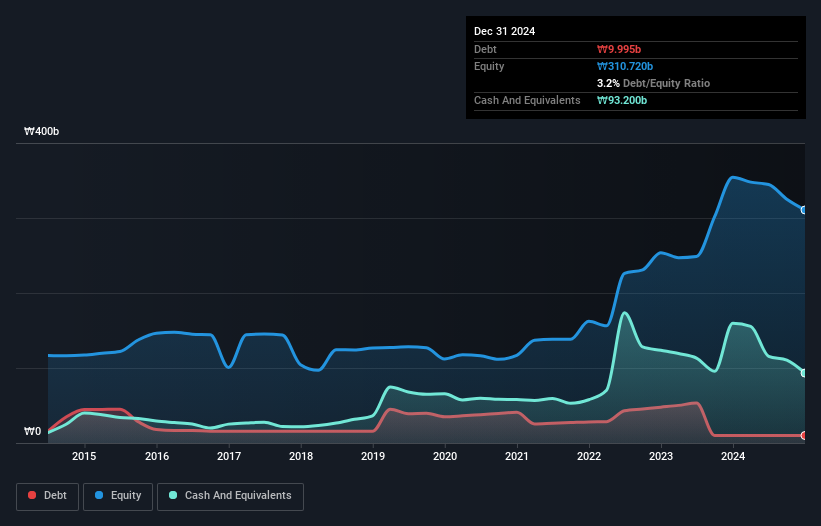

As you can see below, MEDIPOST had ₩9.99b of debt, at December 2024, which is about the same as the year before. You can click the chart for greater detail. However, its balance sheet shows it holds ₩93.2b in cash, so it actually has ₩83.2b net cash.

A Look At MEDIPOST's Liabilities

We can see from the most recent balance sheet that MEDIPOST had liabilities of ₩23.4b falling due within a year, and liabilities of ₩80.2b due beyond that. Offsetting this, it had ₩93.2b in cash and ₩13.4b in receivables that were due within 12 months. So it actually has ₩3.05b more liquid assets than total liabilities.

This state of affairs indicates that MEDIPOST's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the ₩267.7b company is short on cash, but still worth keeping an eye on the balance sheet. Simply put, the fact that MEDIPOST has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since MEDIPOST will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot .

See our latest analysis for MEDIPOST

In the last year MEDIPOST wasn't profitable at an EBIT level, but managed to grow its revenue by 2.9%, to ₩71b. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is MEDIPOST?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year MEDIPOST had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through ₩41b of cash and made a loss of ₩63b. Given it only has net cash of ₩83.2b, the company may need to raise more capital if it doesn't reach break-even soon. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that MEDIPOST is showing 1 warning sign in our investment analysis , you should know about...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A078160

MEDIPOST

Engages in the cord blood bank business in South Korea and internationally.

Adequate balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor