- South Korea

- /

- Food

- /

- KOSE:A264900

Should You Be Impressed By Crown Confectionery's (KRX:264900) Returns on Capital?

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Although, when we looked at Crown Confectionery (KRX:264900), it didn't seem to tick all of these boxes.

Return On Capital Employed (ROCE): What is it?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Crown Confectionery is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.11 = ₩26b ÷ (₩328b - ₩87b) (Based on the trailing twelve months to September 2020).

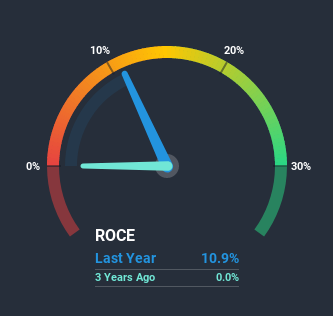

So, Crown Confectionery has an ROCE of 11%. In absolute terms, that's a satisfactory return, but compared to the Food industry average of 6.9% it's much better.

View our latest analysis for Crown Confectionery

Historical performance is a great place to start when researching a stock so above you can see the gauge for Crown Confectionery's ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Crown Confectionery, check out these free graphs here.

The Trend Of ROCE

Things have been pretty stable at Crown Confectionery, with its capital employed and returns on that capital staying somewhat the same for the last two years. It's not uncommon to see this when looking at a mature and stable business that isn't re-investing its earnings because it has likely passed that phase of the business cycle. So don't be surprised if Crown Confectionery doesn't end up being a multi-bagger in a few years time.

In Conclusion...

In a nutshell, Crown Confectionery has been trudging along with the same returns from the same amount of capital over the last two years. Since the stock has declined 26% over the last three years, investors may not be too optimistic on this trend improving either. Therefore based on the analysis done in this article, we don't think Crown Confectionery has the makings of a multi-bagger.

If you'd like to know more about Crown Confectionery, we've spotted 2 warning signs, and 1 of them makes us a bit uncomfortable.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

When trading Crown Confectionery or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A264900

Crown Confectionery

Manufactures and sells confectionery products in Korea.

Flawless balance sheet and slightly overvalued.

Market Insights

Community Narratives