Readers hoping to buy FOODWELL Co., Ltd. (KOSDAQ:005670) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. You will need to purchase shares before the 29th of December to receive the dividend, which will be paid on the 9th of April.

The upcoming dividend for FOODWELL will put a total of ₩100.00 per share in shareholders' pockets, up from last year's total dividends of ₩60.00. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to check whether the dividend payments are covered, and if earnings are growing.

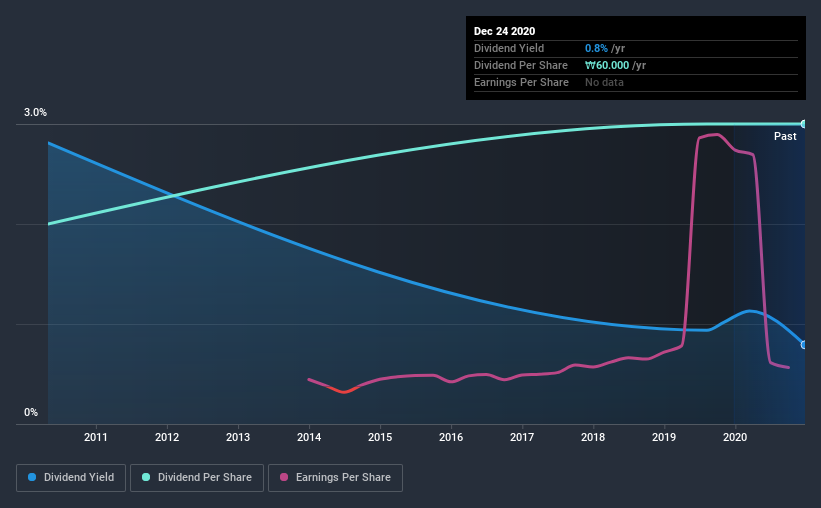

See our latest analysis for FOODWELL

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. That's why it's good to see FOODWELL paying out a modest 39% of its earnings. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. Luckily it paid out just 18% of its free cash flow last year.

It's positive to see that FOODWELL's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see how much of its profit FOODWELL paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. That's why it's comforting to see FOODWELL's earnings have been skyrocketing, up 21% per annum for the past five years. FOODWELL is paying out less than half its earnings and cash flow, while simultaneously growing earnings per share at a rapid clip. This is a very favourable combination that can often lead to the dividend multiplying over the long term, if earnings grow and the company pays out a higher percentage of its earnings.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Since the start of our data, 10 years ago, FOODWELL has lifted its dividend by approximately 4.1% a year on average. Earnings per share have been growing much quicker than dividends, potentially because FOODWELL is keeping back more of its profits to grow the business.

The Bottom Line

Is FOODWELL an attractive dividend stock, or better left on the shelf? FOODWELL has been growing earnings at a rapid rate, and has a conservatively low payout ratio, implying that it is reinvesting heavily in its business; a sterling combination. Overall we think this is an attractive combination and worthy of further research.

While it's tempting to invest in FOODWELL for the dividends alone, you should always be mindful of the risks involved. For example, we've found 4 warning signs for FOODWELL that we recommend you consider before investing in the business.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade FOODWELL, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A005670

FOODWELL

Engages in storing and processing agricultural products in South Korea.

Good value with proven track record.

Market Insights

Community Narratives