Advertisement

- South Korea

- /

- Consumer Durables

- /

- KOSE:A192400

Three Undiscovered Gems in South Korea to Enhance Your Portfolio

Simply Wall St

Reviewed by Simply Wall St

South Korea's market has been navigating a mixed economic landscape, with a current account surplus of $9.13 billion in July, down from $12.26 billion in June, and notable increases in both exports and imports. In this environment, identifying promising small-cap stocks can be key to enhancing your portfolio, especially those that show resilience and growth potential amid fluctuating economic conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In South Korea

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Korea Airport ServiceLtd | NA | 3.97% | 42.22% | ★★★★★★ |

| Miwon Chemicals | 0.08% | 11.70% | 14.38% | ★★★★★★ |

| Korea Ratings | NA | 1.13% | 0.54% | ★★★★★★ |

| Samyang | 49.49% | 6.68% | 23.96% | ★★★★★★ |

| Kyung Dong Navien | 22.40% | 11.19% | 18.84% | ★★★★★★ |

| Namuga | 14.47% | 0.88% | 38.25% | ★★★★★★ |

| ONEJOON | 10.13% | 35.30% | -5.78% | ★★★★★☆ |

| iMarketKorea | 28.53% | 5.35% | 1.30% | ★★★★★☆ |

| PaperCorea | 53.09% | 1.31% | 77.27% | ★★★★★☆ |

| FnGuide | 36.10% | 8.92% | 10.27% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

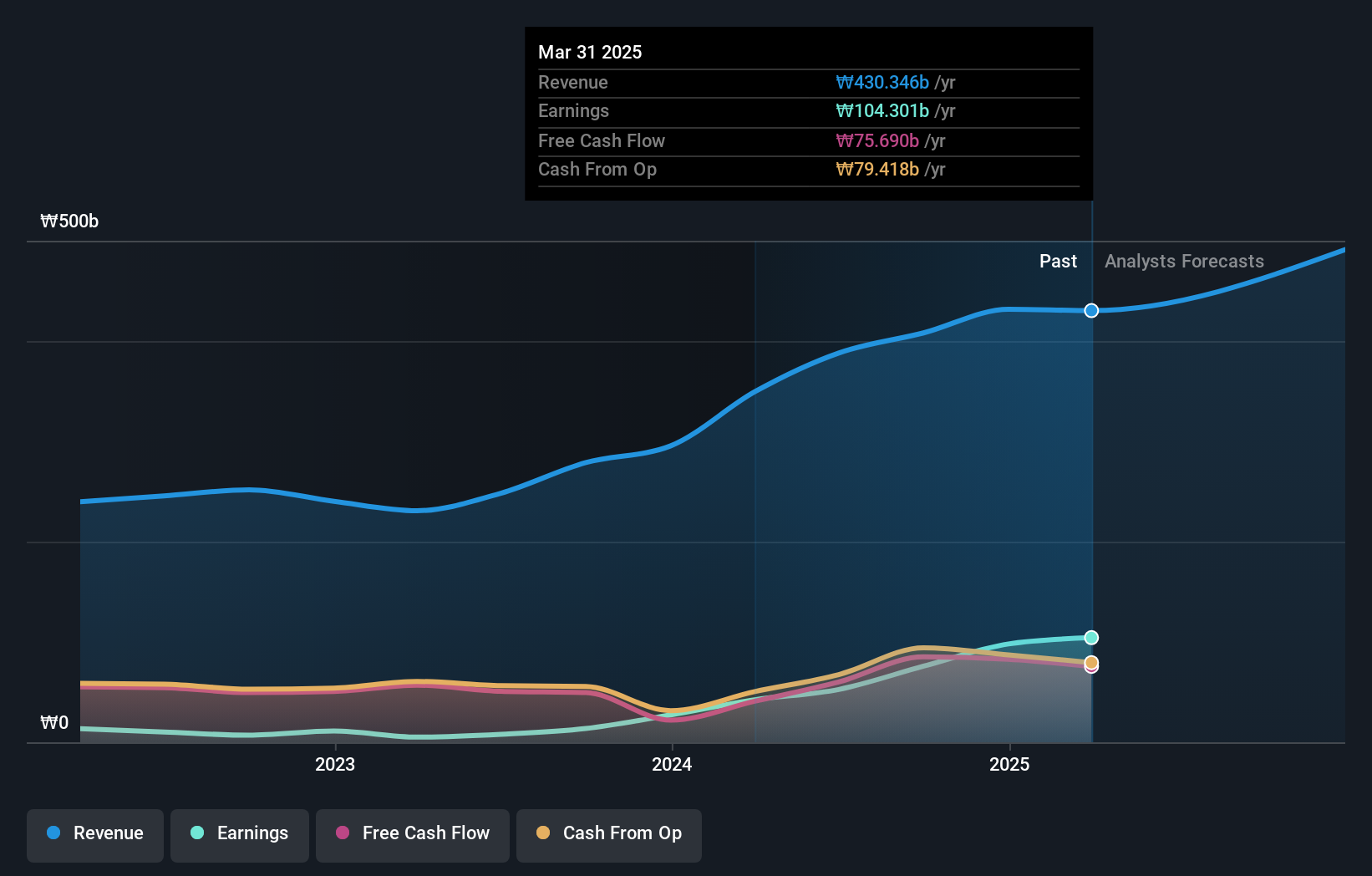

VT (KOSDAQ:A018290)

Simply Wall St Value Rating: ★★★★★★

Overview: VT Co., Ltd. produces and exports laminating machines and films worldwide, with a market cap of ₩1.09 billion.

Operations: VT Co., Ltd. generates revenue primarily from its Cosmetic segment (₩256.27 billion), followed by Entertainment (₩93.74 billion) and Laminating (₩33.86 billion).

VT Co., Ltd. has shown impressive earnings growth, with a 563.7% increase over the past year, significantly outpacing the Personal Products industry's 30.2%. Recent reports indicate second-quarter sales of KRW 113.35 billion and net income of KRW 15.40 billion, compared to KRW 74.69 billion and KRW 5.09 billion respectively a year ago. Despite its highly volatile share price in recent months, VT trades at about 21% below its estimated fair value and has reduced its debt-to-equity ratio from 71% to just over 22% in five years.

- Click here and access our complete health analysis report to understand the dynamics of VT.

Assess VT's past performance with our detailed historical performance reports.

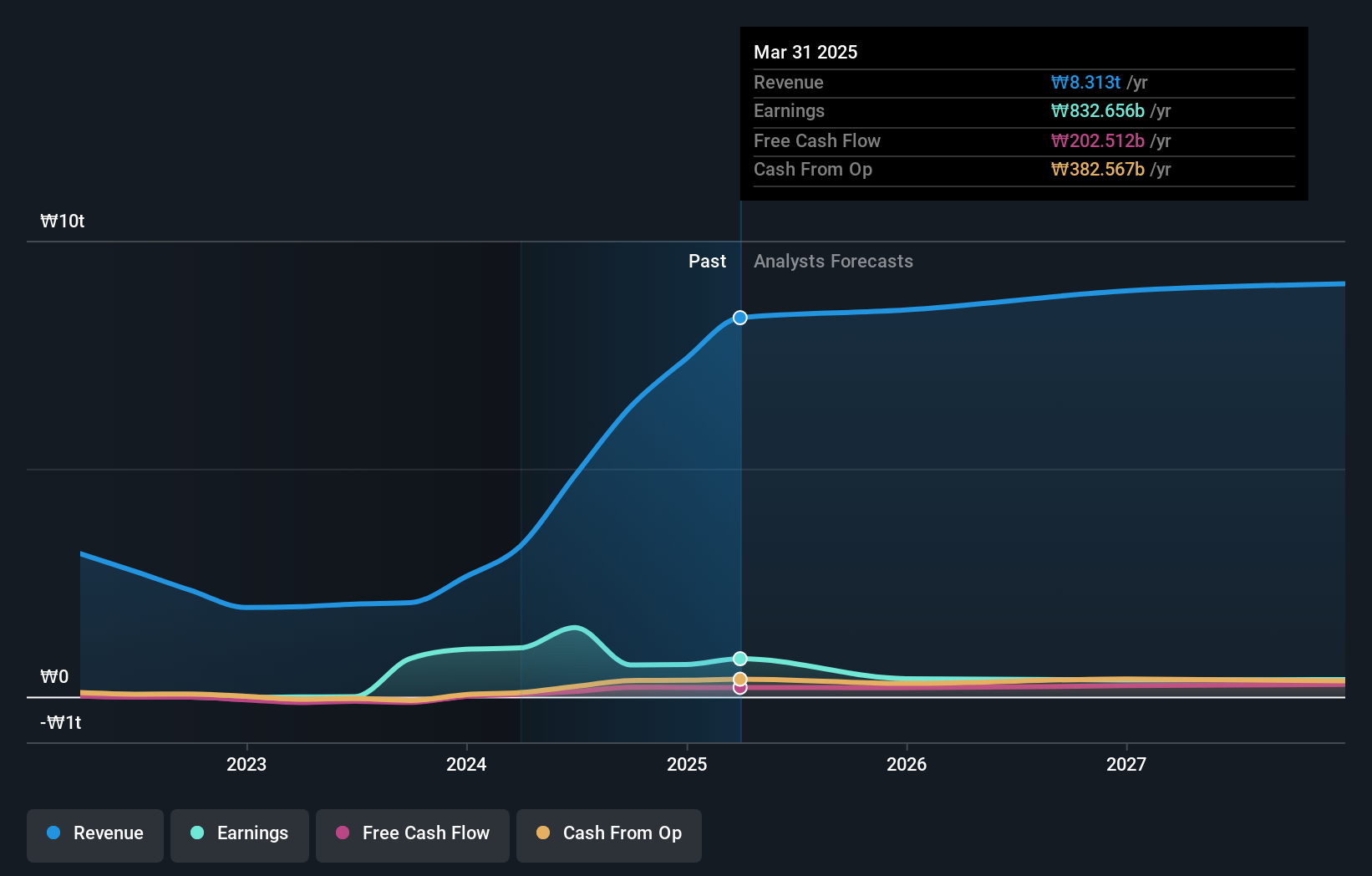

Hyundai G.F. Holdings (KOSE:A005440)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hyundai G.F. Holdings Co., Ltd. engages in the rental and investment businesses with a market cap of ₩767.05 billion.

Operations: Hyundai G.F. Holdings generates its revenue primarily through rental and investment activities. The company operates with a market cap of ₩767.05 billion.

Hyundai G.F. Holdings, a lesser-known entity in South Korea's market, has shown remarkable growth potential. The company’s earnings surged by 242291% over the past year, significantly outpacing the Trade Distributors industry’s 21.7%. Trading at 43.8% below its estimated fair value, it offers an attractive entry point for investors. Additionally, Hyundai G.F.'s debt to equity ratio increased from 1.6 to 10.7 over five years and remains profitable with positive free cash flow projections enhancing its financial stability and future prospects.

- Delve into the full analysis health report here for a deeper understanding of Hyundai G.F. Holdings.

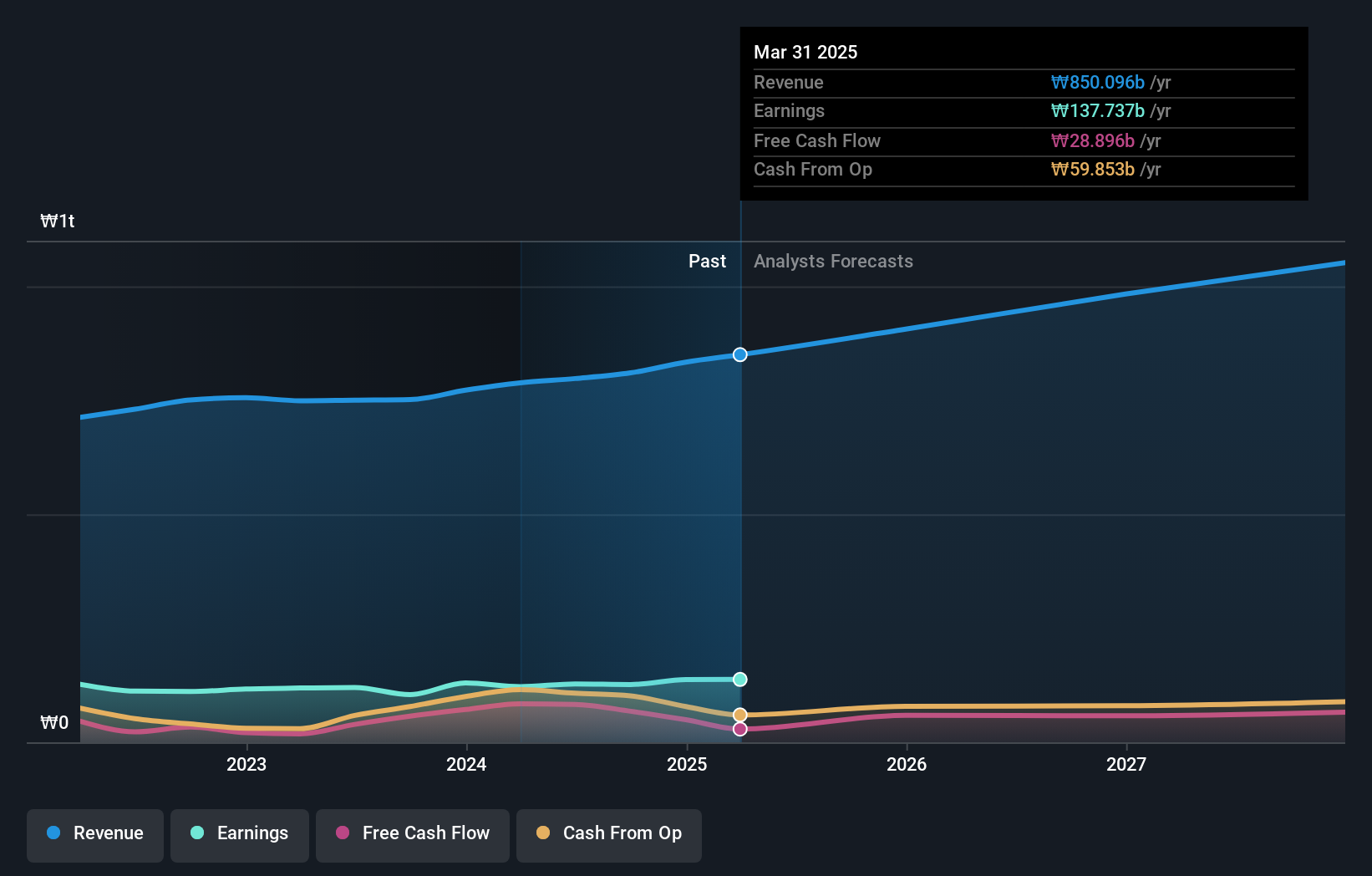

Cuckoo Holdings (KOSE:A192400)

Simply Wall St Value Rating: ★★★★★☆

Overview: Cuckoo Holdings Co., Ltd., along with its subsidiaries, manufactures and sells electric heaters and daily necessities in South Korea and internationally, with a market cap of ₩764.53 billion.

Operations: Cuckoo Holdings generates revenue primarily from its electric heating appliances segment, which reported ₩797.73 billion in sales.

Cuckoo Holdings, a notable player in the South Korean market, offers an intriguing investment case. Over the past five years, earnings have grown at 8.8% annually. Despite this steady growth, recent performance lagged behind the Consumer Durables industry with a 6.5% rise in earnings last year compared to the industry's 26.5%. The company’s debt to equity ratio has increased from 0% to 0.04%, indicating prudent financial management while trading significantly below its estimated fair value by around 79%.

- Take a closer look at Cuckoo Holdings' potential here in our health report.

Examine Cuckoo Holdings' past performance report to understand how it has performed in the past.

Summing It All Up

- Navigate through the entire inventory of 184 KRX Undiscovered Gems With Strong Fundamentals here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A192400

Cuckoo Holdings

Manufactures and sells electric heaters and daily necessities in South Korea and internationally.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative