Statistically speaking, it is less risky to invest in profitable companies than in unprofitable ones. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. In this article, we'll look at how useful this year's statutory profit is, when analysing Shinsung Tongsang (KRX:005390).

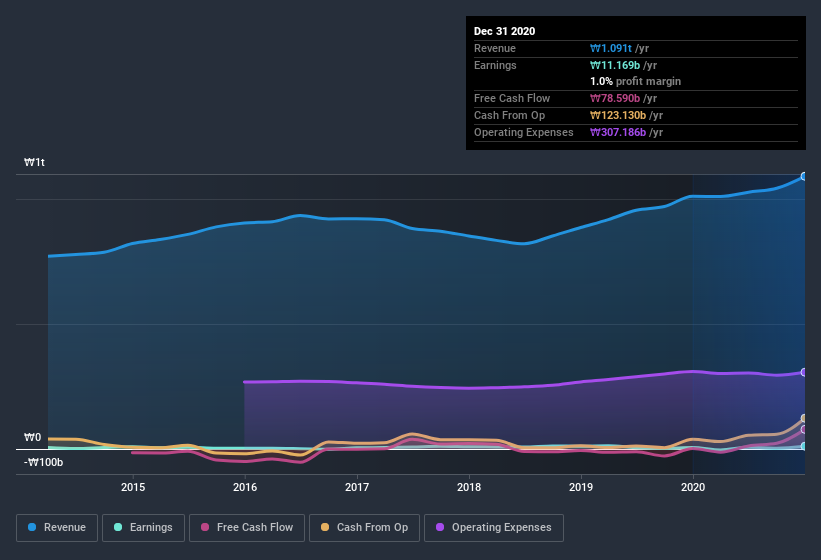

While Shinsung Tongsang was able to generate revenue of ₩1.09t in the last twelve months, we think its profit result of ₩11.2b was more important. Happily, it has grown both its profit and revenue over the last three years, as you can see in the chart below.

See our latest analysis for Shinsung Tongsang

Of course, when it comes to statutory profit, the devil is often in the detail, and we can get a better sense for a company by diving deeper into the financial statements. Today, we'll discuss Shinsung Tongsang's free cashflow relative to its earnings, and consider what that tells us about the company. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Shinsung Tongsang.

Examining Cashflow Against Shinsung Tongsang's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. This ratio tells us how much of a company's profit is not backed by free cashflow.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Over the twelve months to December 2020, Shinsung Tongsang recorded an accrual ratio of -0.13. Therefore, its statutory earnings were quite a lot less than its free cashflow. To wit, it produced free cash flow of ₩79b during the period, dwarfing its reported profit of ₩11.2b. Shinsung Tongsang shareholders are no doubt pleased that free cash flow improved over the last twelve months.

Our Take On Shinsung Tongsang's Profit Performance

Shinsung Tongsang's accrual ratio is solid, and indicates strong free cash flow, as we discussed, above. Because of this, we think Shinsung Tongsang's earnings potential is at least as good as it seems, and maybe even better! Furthermore, it has done a great job growing EPS over the last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you want to do dive deeper into Shinsung Tongsang, you'd also look into what risks it is currently facing. In terms of investment risks, we've identified 1 warning sign with Shinsung Tongsang, and understanding it should be part of your investment process.

This note has only looked at a single factor that sheds light on the nature of Shinsung Tongsang's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

When trading Shinsung Tongsang or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSE:A005390

Shinsung Tongsang

Manufactures, distributes, and sells clothing products in South Korea and internationally.

Flawless balance sheet with proven track record.

Market Insights

Community Narratives