Advertisement

- South Korea

- /

- Electrical

- /

- KOSE:A112610

Are CS Wind Corporation's (KRX:112610) Mixed Financials The Reason For Its Gloomy Performance on The Stock Market?

CS Wind (KRX:112610) has had a rough three months with its share price down 27%. We, however decided to study the company's financials to determine if they have got anything to do with the price decline. Fundamentals usually dictate market outcomes so it makes sense to study the company's financials. In this article, we decided to focus on CS Wind's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for CS Wind

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for CS Wind is:

10% = ₩114b ÷ ₩1.1t (Based on the trailing twelve months to September 2024).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each ₩1 of shareholders' capital it has, the company made ₩0.10 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

CS Wind's Earnings Growth And 10% ROE

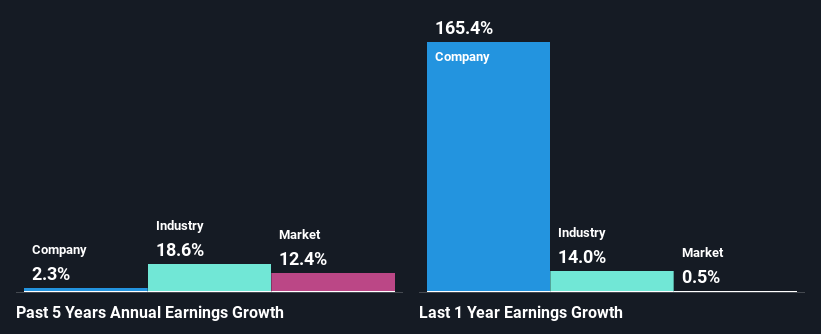

At first glance, CS Wind's ROE doesn't look very promising. Although a closer study shows that the company's ROE is higher than the industry average of 8.3% which we definitely can't overlook. However, CS Wind's five year net income growth was quite low averaging at only 2.3%. Remember, the company's ROE is quite low to begin with, just that it is higher than the industry average. Hence, this goes some way in explaining the low earnings growth.

We then compared CS Wind's net income growth with the industry and found that the company's growth figure is lower than the average industry growth rate of 19% in the same 5-year period, which is a bit concerning.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is CS Wind fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is CS Wind Using Its Retained Earnings Effectively?

With a high three-year median payout ratio of 75% (or a retention ratio of 25%), most of CS Wind's profits are being paid to shareholders. This definitely contributes to the low earnings growth seen by the company.

Additionally, CS Wind has paid dividends over a period of five years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 13% over the next three years. As a result, the expected drop in CS Wind's payout ratio explains the anticipated rise in the company's future ROE to 18%, over the same period.

Summary

On the whole, we feel that the performance shown by CS Wind can be open to many interpretations. On the one hand, the company does have a decent rate of return, however, its earnings growth number is quite disappointing and as discussed earlier, the low retained earnings is hampering the growth. With that said, the latest industry analyst forecasts reveal that the company's earnings are expected to accelerate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A112610

CS Wind

Manufactures and sells wind towers in the Vietnam, China, Canada, the United Kingdom, Turkey, Taiwan, Malaysia, Australia, and internationally.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor