- South Korea

- /

- Machinery

- /

- KOSE:A075580

Sejin Heavy Industries Co., Ltd.'s (KRX:075580) 27% Price Boost Is Out Of Tune With Earnings

The Sejin Heavy Industries Co., Ltd. (KRX:075580) share price has done very well over the last month, posting an excellent gain of 27%. The last 30 days bring the annual gain to a very sharp 29%.

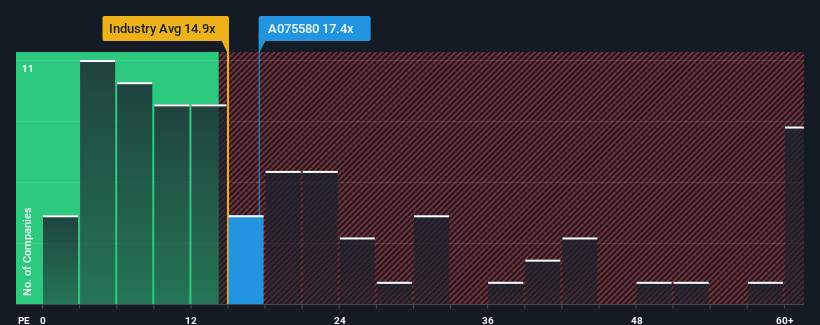

After such a large jump in price, given around half the companies in Korea have price-to-earnings ratios (or "P/E's") below 12x, you may consider Sejin Heavy Industries as a stock to potentially avoid with its 17.4x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Sejin Heavy Industries has been doing quite well of late. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. If not, then existing shareholders might be a little nervous about the viability of the share price.

See our latest analysis for Sejin Heavy Industries

Is There Enough Growth For Sejin Heavy Industries?

The only time you'd be truly comfortable seeing a P/E as high as Sejin Heavy Industries' is when the company's growth is on track to outshine the market.

If we review the last year of earnings growth, the company posted a terrific increase of 94%. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 26% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to slump, contracting by 5.8% during the coming year according to the two analysts following the company. With the market predicted to deliver 33% growth , that's a disappointing outcome.

In light of this, it's alarming that Sejin Heavy Industries' P/E sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a very good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the negative growth outlook.

The Key Takeaway

Sejin Heavy Industries' P/E is getting right up there since its shares have risen strongly. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Sejin Heavy Industries' analyst forecasts revealed that its outlook for shrinking earnings isn't impacting its high P/E anywhere near as much as we would have predicted. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings are highly unlikely to support such positive sentiment for long. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

There are also other vital risk factors to consider before investing and we've discovered 3 warning signs for Sejin Heavy Industries that you should be aware of.

If you're unsure about the strength of Sejin Heavy Industries' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A075580

Sejin Heavy Industries

Manufactures and sells shipbuilding equipment in South Korea.

High growth potential with solid track record.