Advertisement

- South Korea

- /

- Trade Distributors

- /

- KOSDAQ:A162300

Shin SteelLtd's (KOSDAQ:162300) one-year decline in earnings translates into losses for shareholders

Shin Steel Co.,Ltd. (KOSDAQ:162300) shareholders should be happy to see the share price up 17% in the last quarter. But that is minimal compensation for the share price under-performance over the last year. The cold reality is that the stock has dropped 29% in one year, under-performing the market.

While the stock has risen 12% in the past week but long term shareholders are still in the red, let's see what the fundamentals can tell us.

View our latest analysis for Shin SteelLtd

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

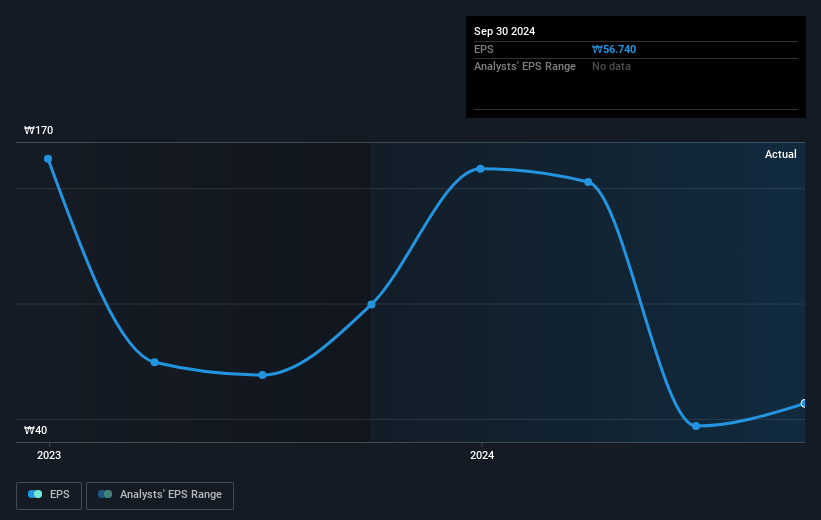

Unfortunately Shin SteelLtd reported an EPS drop of 43% for the last year. This fall in the EPS is significantly worse than the 29% the share price fall. It may have been that the weak EPS was not as bad as some had feared. Indeed, with a P/E ratio of 46.79 there is obviously some real optimism that earnings will bounce back.

The image below shows how EPS has tracked over time (if you click on the image you can see greater detail).

Before buying or selling a stock, we always recommend a close examination of historic growth trends, available here.

A Different Perspective

We regret to report that Shin SteelLtd shareholders are down 28% for the year (even including dividends). Unfortunately, that's worse than the broader market decline of 2.7%. However, it could simply be that the share price has been impacted by broader market jitters. It might be worth keeping an eye on the fundamentals, in case there's a good opportunity. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 0.3% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Even so, be aware that Shin SteelLtd is showing 4 warning signs in our investment analysis , and 2 of those make us uncomfortable...

If you are like me, then you will not want to miss this free list of undervalued small caps that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on South Korean exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A162300

Shin SteelLtd

A steel distribution company, engages in the supplying of various steel products for applications in home appliances and construction fields.

Mediocre balance sheet low.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.9% undervalued

TO

Community Contributor