- South Korea

- /

- Machinery

- /

- KOSDAQ:A101930

Optimistic Investors Push Inhwa Precision Co., Ltd (KOSDAQ:101930) Shares Up 26% But Growth Is Lacking

Despite an already strong run, Inhwa Precision Co., Ltd (KOSDAQ:101930) shares have been powering on, with a gain of 26% in the last thirty days. The annual gain comes to 245% following the latest surge, making investors sit up and take notice.

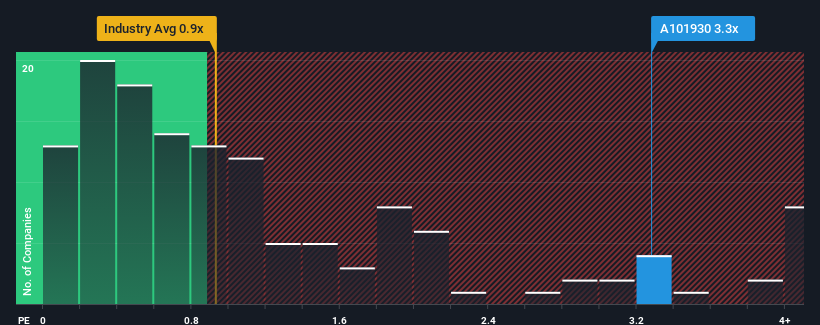

After such a large jump in price, you could be forgiven for thinking Inhwa Precision is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 3.3x, considering almost half the companies in Korea's Machinery industry have P/S ratios below 0.9x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Inhwa Precision

What Does Inhwa Precision's P/S Mean For Shareholders?

Recent times have been quite advantageous for Inhwa Precision as its revenue has been rising very briskly. The P/S ratio is probably high because investors think this strong revenue growth will be enough to outperform the broader industry in the near future. However, if this isn't the case, investors might get caught out paying too much for the stock.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Inhwa Precision's earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Inhwa Precision?

Inhwa Precision's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 59% last year. Still, revenue has barely risen at all from three years ago in total, which is not ideal. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

Comparing that to the industry, which is predicted to deliver 45% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

In light of this, it's alarming that Inhwa Precision's P/S sits above the majority of other companies. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Final Word

Inhwa Precision's P/S has grown nicely over the last month thanks to a handy boost in the share price. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

The fact that Inhwa Precision currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we observe slower-than-industry revenue growth alongside a high P/S ratio, we assume there to be a significant risk of the share price decreasing, which would result in a lower P/S ratio. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these the share price as being reasonable.

Before you take the next step, you should know about the 3 warning signs for Inhwa Precision that we have uncovered.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A101930

Inhwa Precision

Manufactures and sells marine engine parts, automobile parts, metal forming machines, and metal structural materials in South Korea and internationally.

Good value with adequate balance sheet.

Market Insights

Community Narratives