Advertisement

- South Korea

- /

- Machinery

- /

- KOSDAQ:A094820

Pinning Down Iljin Power Co., Ltd.'s (KOSDAQ:094820) P/E Is Difficult Right Now

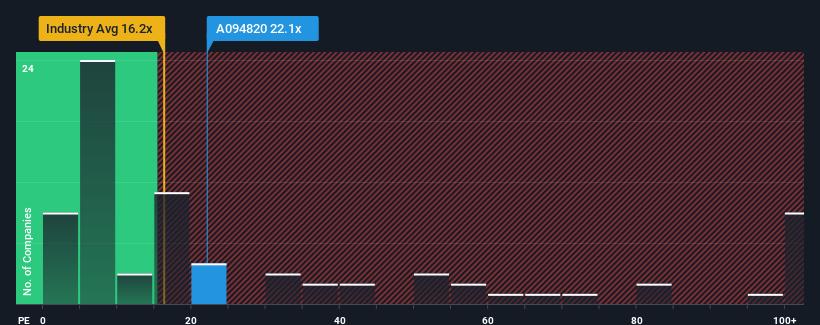

When close to half the companies in Korea have price-to-earnings ratios (or "P/E's") below 14x, you may consider Iljin Power Co., Ltd. (KOSDAQ:094820) as a stock to avoid entirely with its 22.1x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

For example, consider that Iljin Power's financial performance has been poor lately as its earnings have been in decline. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

View our latest analysis for Iljin Power

How Is Iljin Power's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as steep as Iljin Power's is when the company's growth is on track to outshine the market decidedly.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 62%. This means it has also seen a slide in earnings over the longer-term as EPS is down 36% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 35% shows it's an unpleasant look.

In light of this, it's alarming that Iljin Power's P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Final Word

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Iljin Power currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Iljin Power, and understanding these should be part of your investment process.

You might be able to find a better investment than Iljin Power. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A094820

Iljin Power

Engages in the manufacture of nuclear and renewable energy equipment.

Adequate balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets