- South Korea

- /

- Personal Products

- /

- KOSDAQ:A018290

Discover These 3 Undiscovered Gems in South Korea

Reviewed by Simply Wall St

In the last week, the South Korean market has stayed flat, with the Consumer Staples sector gaining 3.2%, although it is down 3.1% over the past year. With earnings forecasted to grow by 29% annually, identifying promising stocks that are currently underappreciated can offer significant opportunities for investors looking to capitalize on future growth potential.

Top 10 Undiscovered Gems With Strong Fundamentals In South Korea

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Samyang | 49.49% | 6.68% | 23.96% | ★★★★★★ |

| Korea Airport ServiceLtd | NA | 3.97% | 42.22% | ★★★★★★ |

| Korea Cast Iron Pipe Ind | NA | 1.97% | 8.84% | ★★★★★★ |

| Woori Technology Investment | NA | 25.66% | -1.45% | ★★★★★★ |

| Kyung Dong Navien | 22.40% | 11.19% | 18.84% | ★★★★★★ |

| Namuga | 14.47% | 0.88% | 38.25% | ★★★★★★ |

| SELVAS Healthcare | 13.50% | 9.36% | 71.59% | ★★★★★★ |

| ONEJOON | 10.13% | 35.30% | -5.78% | ★★★★★☆ |

| iMarketKorea | 28.53% | 5.35% | 1.30% | ★★★★★☆ |

| Daewon Cable | 30.50% | 8.72% | 60.28% | ★★★★★☆ |

Let's review some notable picks from our screened stocks.

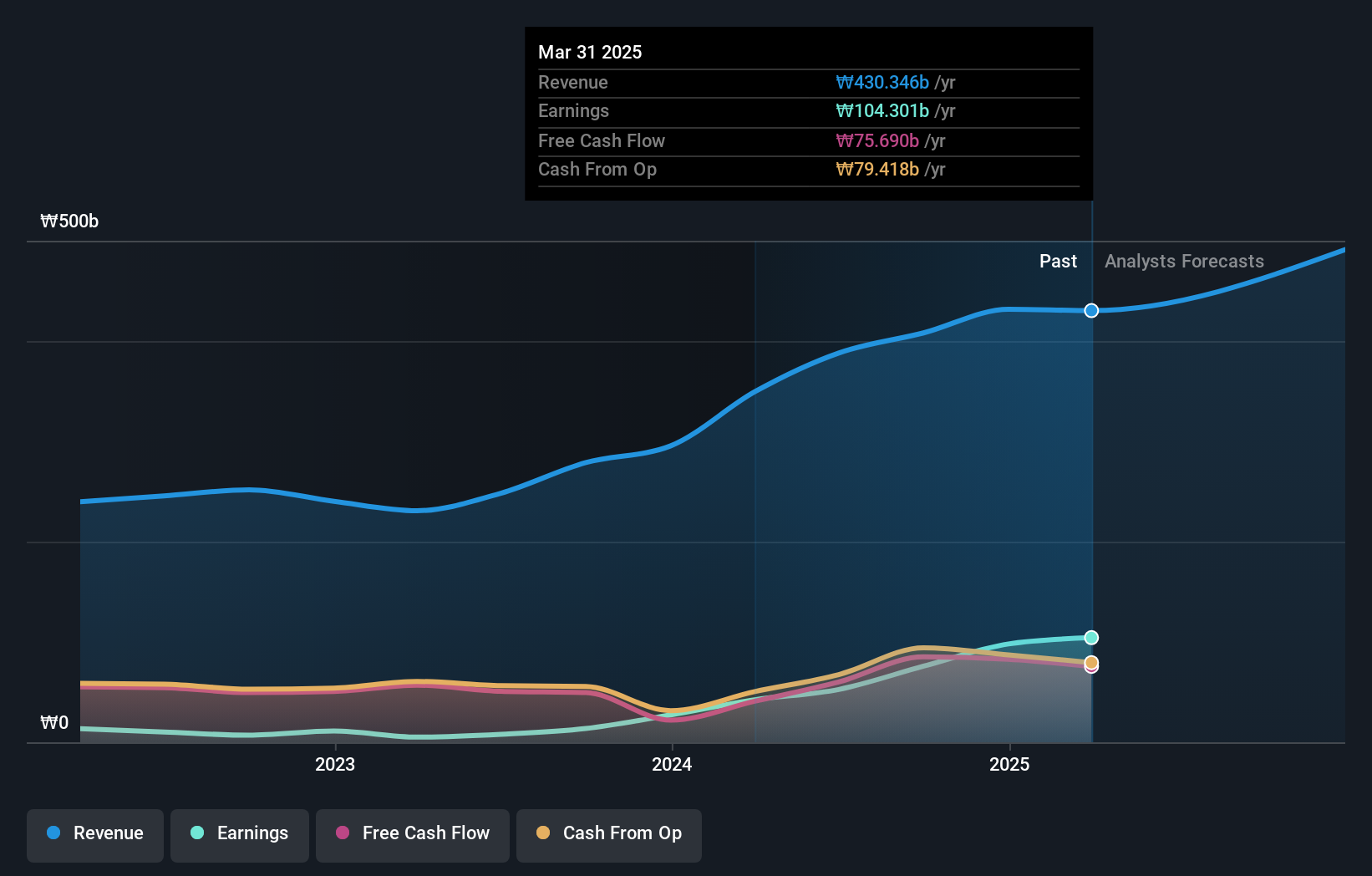

VT (KOSDAQ:A018290)

Simply Wall St Value Rating: ★★★★★★

Overview: VT Co., Ltd. produces and exports laminating machines and films worldwide, with a market cap of ₩1.25 billion.

Operations: VT Co., Ltd. generates revenue primarily from its Cosmetic segment (₩256.27 billion) and Entertainment segment (₩93.74 billion), with additional contributions from Laminating machines and films (₩33.86 billion).

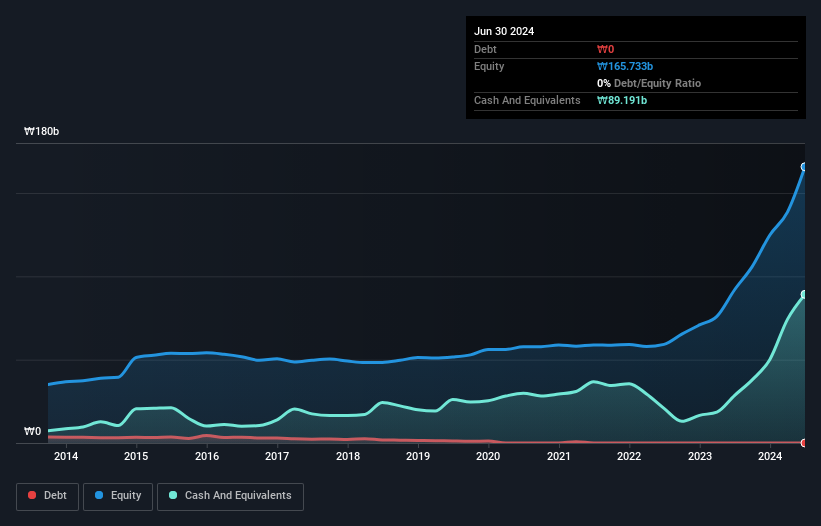

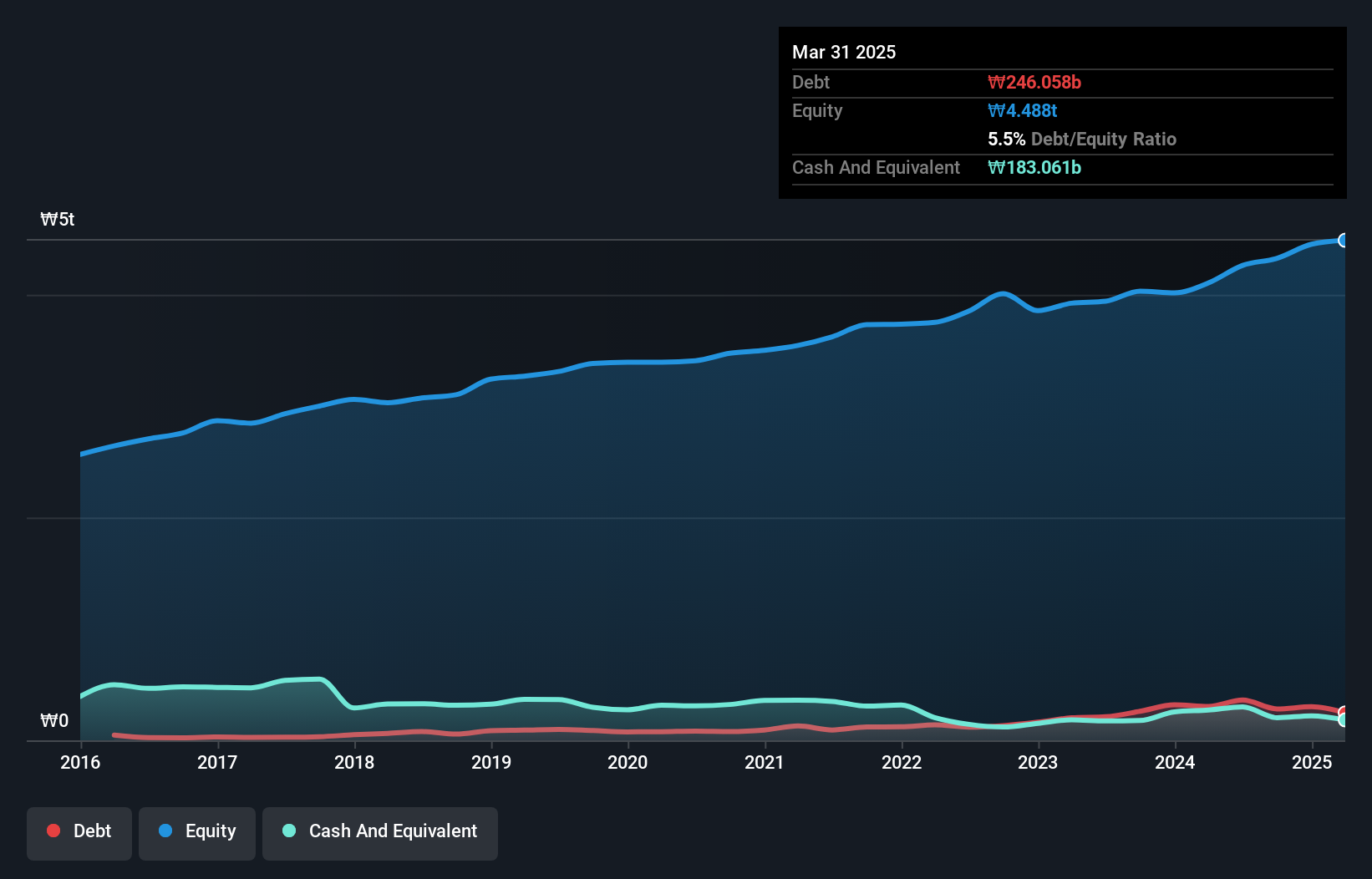

VT Co., Ltd. has shown remarkable performance with its debt to equity ratio dropping from 71.2% to 22.4% over the last five years, indicating improved financial health. Their earnings growth of 563.7% in the past year outpaced the Personal Products industry average of 30.2%. Additionally, VT's basic earnings per share surged from KRW 154 to KRW 481 in Q2-2024 compared to a year ago, reflecting robust profitability and operational efficiency improvements despite recent shareholder dilution and share price volatility.

- Navigate through the intricacies of VT with our comprehensive health report here.

Review our historical performance report to gain insights into VT's's past performance.

Cheryong ElectricLtd (KOSDAQ:A033100)

Simply Wall St Value Rating: ★★★★★★

Overview: Cheryong Electric Co., Ltd. manufactures and sells power electric equipment in South Korea, with a market cap of ₩894.68 billion.

Operations: Cheryong Electric Co., Ltd. generates revenue primarily from the sale of power electric equipment in South Korea, with a market cap of ₩894.68 billion. The company’s financial performance includes notable figures such as its gross profit margin, which reflects its profitability on goods sold before accounting for other expenses.

Cheryong Electric has shown impressive growth, with earnings surging 134% in the past year, outpacing the Electrical industry’s 18.5%. The company is debt-free and trades at 81.2% below its estimated fair value, indicating potential undervaluation. Despite a highly volatile share price over the last three months, Cheryong remains profitable and free cash flow positive. Notably, it has no interest payment concerns due to its zero-debt status compared to five years ago when it had a debt-to-equity ratio of 2.3%.

- Click here and access our complete health analysis report to understand the dynamics of Cheryong ElectricLtd.

Understand Cheryong ElectricLtd's track record by examining our Past report.

Hankook (KOSE:A000240)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hankook & Company Co., Ltd. manufactures and sells storage batteries and has a market cap of ₩1.69 trillion.

Operations: Hankook generates revenue primarily through the sale of storage batteries. The company has a market cap of ₩1.69 trillion.

Hankook has shown significant growth, with earnings increasing by 267% over the past year, outpacing the Auto Components industry. The debt to equity ratio has risen from 3% to 8.5% in five years, yet remains satisfactory at 1.4%. Trading at a P/E ratio of 4.9x, it is considered good value compared to the KR market average of 11.1x. Recent reports show net income for Q2 at KRW108 billion and basic earnings per share at KRW1,145 from continuing operations.

- Unlock comprehensive insights into our analysis of Hankook stock in this health report.

Gain insights into Hankook's historical performance by reviewing our past performance report.

Turning Ideas Into Actions

- Explore the 186 names from our KRX Undiscovered Gems With Strong Fundamentals screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A018290

Outstanding track record with flawless balance sheet.