- South Korea

- /

- Trade Distributors

- /

- KOSE:A005440

Unveiling 3 Undiscovered Gems in South Korea with Strong Potential

Reviewed by Simply Wall St

The South Korea stock market has experienced a challenging period, finishing lower in six consecutive sessions and shedding more than 160 points, with the KOSPI index now resting just above the 2,520-point mark. Despite this recent downturn, there is cautious optimism as investors look ahead to key inflation data that could influence future market movements. In such a volatile environment, identifying stocks with strong fundamentals and growth potential becomes crucial. Here are three undiscovered gems in South Korea that stand out for their resilience and promising outlook amidst current market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In South Korea

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| NOROO PAINT & COATINGS | 13.99% | 5.04% | 7.98% | ★★★★★★ |

| Miwon Chemicals | 0.08% | 11.70% | 14.38% | ★★★★★★ |

| Korea Cast Iron Pipe Ind | NA | 1.97% | 8.84% | ★★★★★★ |

| Korea Airport ServiceLtd | NA | 3.97% | 42.22% | ★★★★★★ |

| Samyang | 49.49% | 6.68% | 23.96% | ★★★★★★ |

| Korea Ratings | NA | 1.13% | 0.54% | ★★★★★★ |

| Woori Technology Investment | NA | 25.66% | -1.45% | ★★★★★★ |

| ONEJOON | 10.13% | 35.30% | -5.78% | ★★★★★☆ |

| iMarketKorea | 28.53% | 5.35% | 1.30% | ★★★★★☆ |

| Daewon Cable | 30.50% | 8.72% | 60.38% | ★★★★★☆ |

We're going to check out a few of the best picks from our screener tool.

VT (KOSDAQ:A018290)

Simply Wall St Value Rating: ★★★★★★

Overview: VT Co., Ltd. produces and exports laminating machines and films worldwide, with a market cap of ₩1.20 trillion.

Operations: VT Co., Ltd. generates revenue primarily from its Cosmetic segment (₩256.27 billion), followed by Entertainment (₩93.74 billion) and Laminating (₩33.86 billion).

VT Co., Ltd. has shown remarkable growth, with earnings surging 563.7% over the past year, far outpacing the Personal Products industry average of 30.2%. The company reported second-quarter sales of KRW 113.35 billion (US$84.99 million), up from KRW 74.69 billion (US$56 million) a year ago, and net income jumped to KRW 15.40 billion (US$11.55 million). Despite recent shareholder dilution, VT's debt-to-equity ratio improved significantly from 71.2% to 22.4% over five years.

- Click here to discover the nuances of VT with our detailed analytical health report.

Evaluate VT's historical performance by accessing our past performance report.

Hankook (KOSE:A000240)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hankook & Company Co., Ltd. manufactures and sells storage batteries, with a market cap of ₩1.70 trillion.

Operations: Hankook & Company Co., Ltd. generates revenue primarily from the sale of storage batteries. With a market cap of ₩1.70 trillion, the company's financial performance is driven by its core product line in this segment.

Hankook has shown impressive performance with net income soaring to ₩108.48 billion in Q2 2024 from ₩36.32 billion a year ago, and basic earnings per share climbing to ₩1,145 from ₩383. The company trades at a favorable P/E ratio of 5x compared to the KR market's 11.1x, indicating good value. Additionally, interest payments are well covered by EBIT at 40x coverage, and earnings growth over the past year outpaced the Auto Components industry significantly at 267%.

- Get an in-depth perspective on Hankook's performance by reading our health report here.

Assess Hankook's past performance with our detailed historical performance reports.

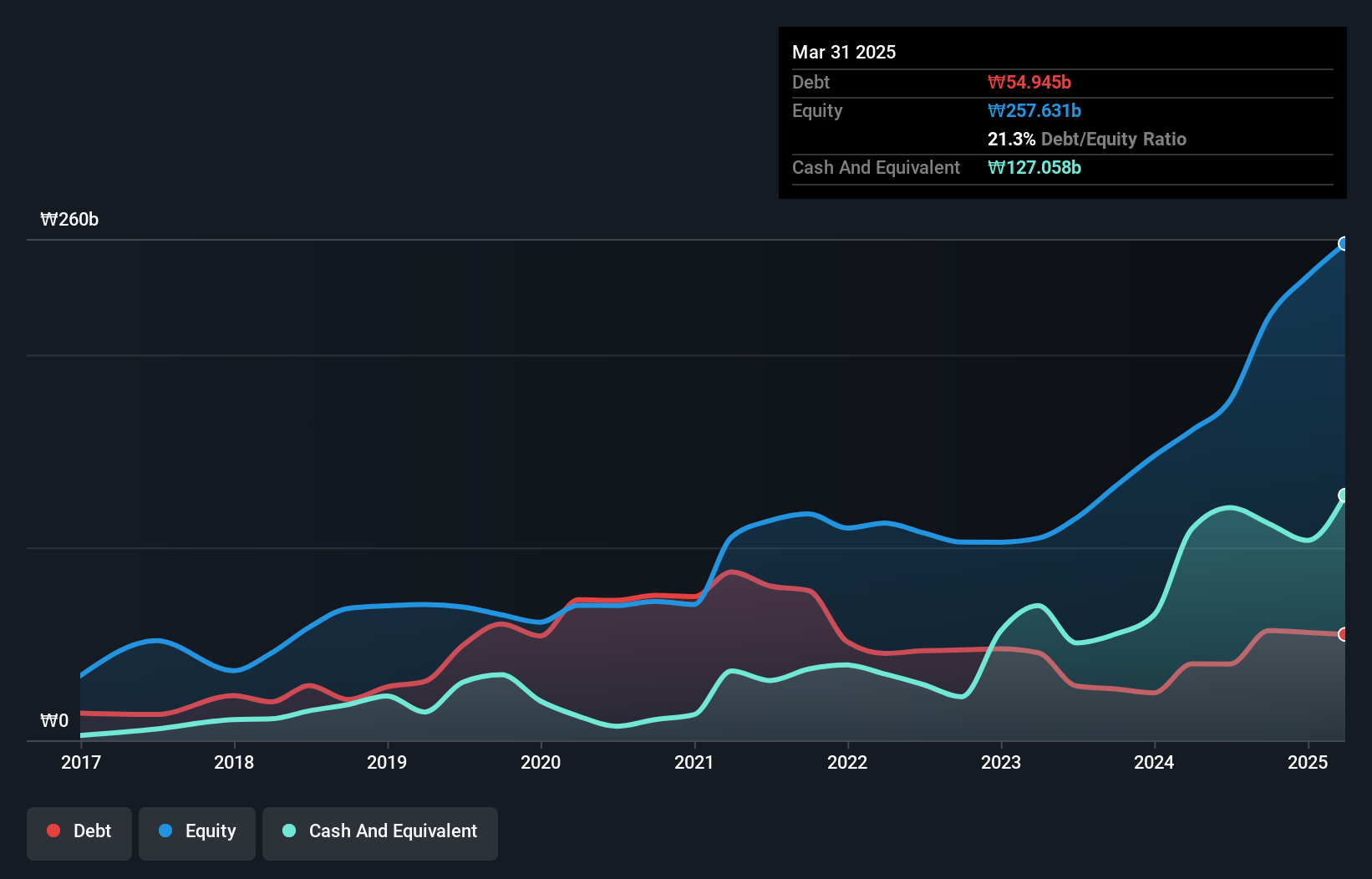

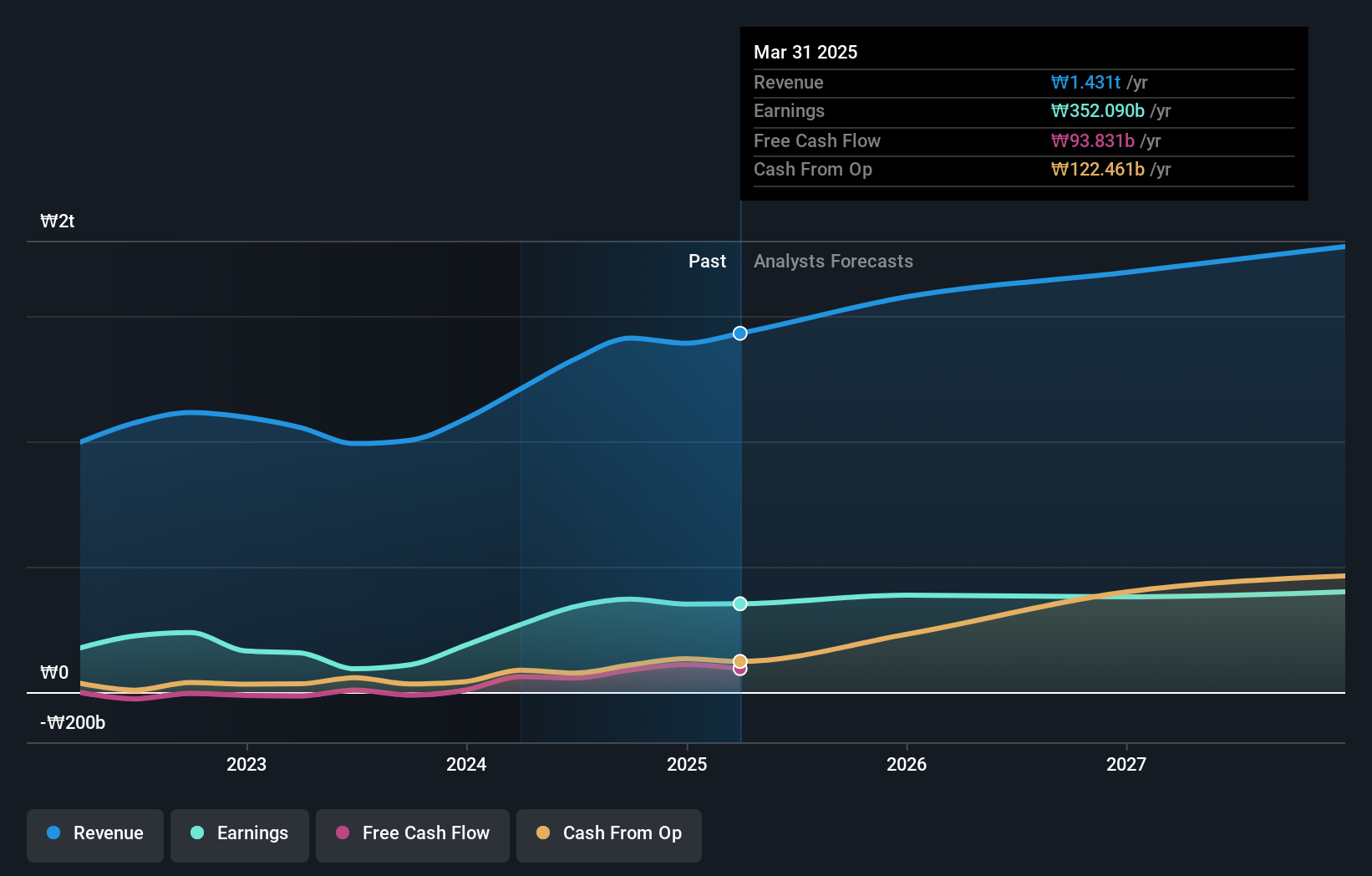

Hyundai G.F. Holdings (KOSE:A005440)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hyundai G.F. Holdings Co., Ltd. engages in rental and investment businesses with a market cap of ₩777.96 billion.

Operations: Hyundai G.F. Holdings generates revenue primarily through its rental and investment activities. The company's market cap stands at ₩777.96 billion, reflecting its significant presence in these sectors.

Hyundai G.F. Holdings, a lesser-known player in South Korea's market, has shown remarkable earnings growth of 242291% over the past year, significantly outpacing the Trade Distributors industry at 21.7%. The company is trading at 43.2% below its estimated fair value and boasts a strong balance sheet with more cash than total debt. Additionally, Hyundai G.F.'s revenue is projected to grow by 20.82% annually, indicating promising future prospects for this small-cap stock.

Taking Advantage

- Click through to start exploring the rest of the 180 KRX Undiscovered Gems With Strong Fundamentals now.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hyundai G.F. Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A005440

Undervalued with excellent balance sheet and pays a dividend.