Japan Transcity Corporation (TSE:9310) will increase its dividend from last year's comparable payment on the 4th of December to ¥16.50. Despite this raise, the dividend yield of 1.4% is only a modest boost to shareholder returns.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Japan Transcity's stock price has increased by 47% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

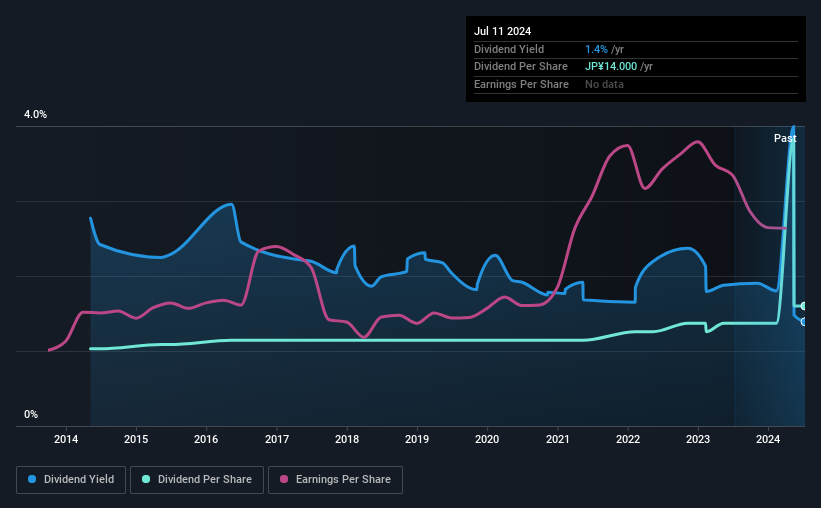

Check out our latest analysis for Japan Transcity

Japan Transcity's Dividend Is Well Covered By Earnings

While yield is important, another factor to consider about a company's dividend is whether the current payout levels are feasible. Japan Transcity is quite easily earning enough to cover the dividend, however it is being let down by weak cash flows. In general, we consider cash flow to be more important than earnings, so we would be cautious about relying on the sustainability of this dividend.

Over the next year, EPS could expand by 12.0% if recent trends continue. If the dividend continues on this path, the payout ratio could be 29% by next year, which we think can be pretty sustainable going forward.

Japan Transcity Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. Since 2014, the annual payment back then was ¥9.00, compared to the most recent full-year payment of ¥14.00. This implies that the company grew its distributions at a yearly rate of about 4.5% over that duration. While the consistency in the dividend payments is impressive, we think the relatively slow rate of growth is less attractive.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. Japan Transcity has impressed us by growing EPS at 12% per year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for Japan Transcity's prospects of growing its dividend payments in the future.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. While the low payout ratio is a redeeming feature, this is offset by the minimal cash to cover the payments. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've picked out 1 warning sign for Japan Transcity that investors should know about before committing capital to this stock. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9310

Japan Transcity

Engages in logistics business in Japan and internationally.

6 star dividend payer with solid track record.