Advertisement

Is Nippon Express (TSE:9147) Overvalued or Undervalued Given Its Premium P/E and DCF Upside?

Simply Wall St

Reviewed by Simply Wall St

Recent performance and why investors are watching

Nippon Express Holdings (TSE:9147) has been quietly reshaping its investment story, with shares up about 34% year to date even as returns over the past 3 months have slipped.

See our latest analysis for Nippon Express Holdings.

That strong year to date share price return sits alongside a three year total shareholder return in the mid 30s, suggesting investors are still rewarding Nippon Express Holdings for steady profit growth but have recently cooled on short term momentum.

If the logistics story here has caught your eye, it could be worth scanning other transport heavy names and discovering fast growing stocks with high insider ownership for fresh ideas with strong alignment between management and shareholders.

With profits growing faster than sales and the stock still trading below analyst targets and some intrinsic estimates, the question now is simple: is Nippon Express undervalued or is the market already pricing in its future growth?

Price-to-Earnings of 31.6x: Is it justified?

On a price-to-earnings basis, Nippon Express Holdings looks expensive at a 31.6x multiple versus its last close of ¥3,258, pointing to a rich earnings valuation relative to peers.

The price-to-earnings ratio compares what investors are paying today for each unit of current earnings, a widely used yardstick for asset light, profit focused logistics businesses. At 31.6x, the market is assigning Nippon Express Holdings a premium that implies strong confidence in future profitability, even though recent earnings growth has only just begun to accelerate after several weaker years.

That premium stands out against both the estimated fair price to earnings ratio of 26.6x and the broader JP Logistics industry average of 13.7x, as well as a 16.2x peer average. In other words, the stock trades at well above the levels the market could eventually gravitate toward if expectations cool or forecasts are not met.

Explore the SWS fair ratio for Nippon Express Holdings

Result: Price-to-Earnings of 31.6x (OVERVALUED)

However, investors should watch for any slowdown in global trade volumes or weaker pricing power, which could challenge current earnings momentum and today’s premium valuation.

Find out about the key risks to this Nippon Express Holdings narrative.

Another angle on valuation

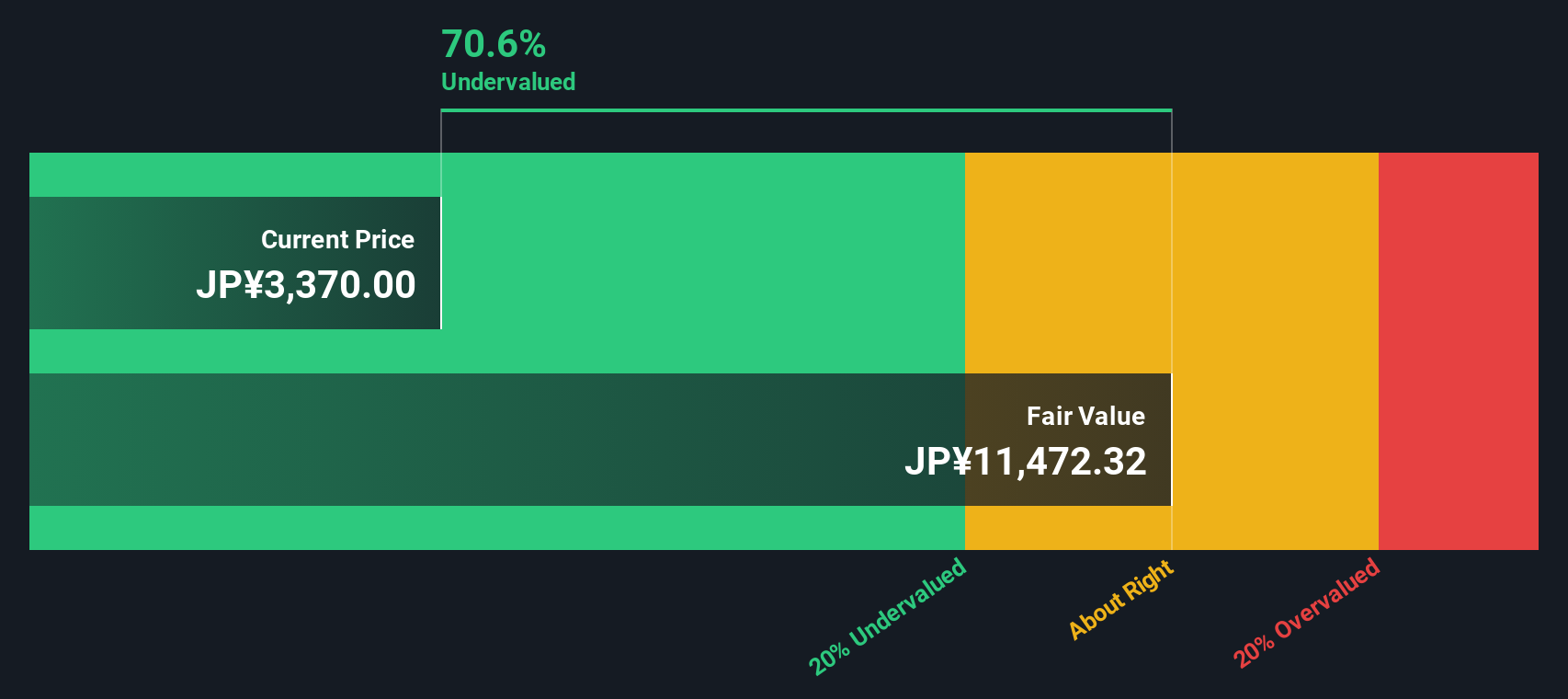

Our DCF model paints a very different picture, suggesting Nippon Express Holdings could be deeply undervalued, with the current ¥3,258 price sitting well below an estimated fair value of about ¥10,515. If the cash flow story is right, the rich earnings multiple could be masking upside rather than risk.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nippon Express Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 928 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Nippon Express Holdings Narrative

If you see the story differently or simply want to dig into the numbers yourself, you can craft a custom view in minutes, Do it your way.

A great starting point for your Nippon Express Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, put your research to work by scanning targeted stock ideas on Simply Wall St’s Screener, so you never miss the next compelling setup.

- Capture potential mispricings by running through these 928 undervalued stocks based on cash flows that may be trading well below the cash flows they generate.

- Ride powerful themes in automation and machine learning by focusing on these 25 AI penny stocks shaping the next wave of digital transformation.

- Strengthen your income stream by zeroing in on these 14 dividend stocks with yields > 3% that can support long term returns with reliable payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nippon Express Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9147

Nippon Express Holdings

Provides logistics services in Japan, the Americas, Europe, East Asia, South Asia, and Oceania.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

32 followersusers have followed this narrative

6 commentsusers have commented on this narrative

9 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1919.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

950 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative