- Japan

- /

- Electronic Equipment and Components

- /

- TSE:8084

Some Investors May Be Willing To Look Past Ryoden's (TSE:8084) Soft Earnings

The market for Ryoden Corporation's (TSE:8084) shares didn't move much after it posted weak earnings recently. We think that the softer headline numbers might be getting counterbalanced by some positive underlying factors.

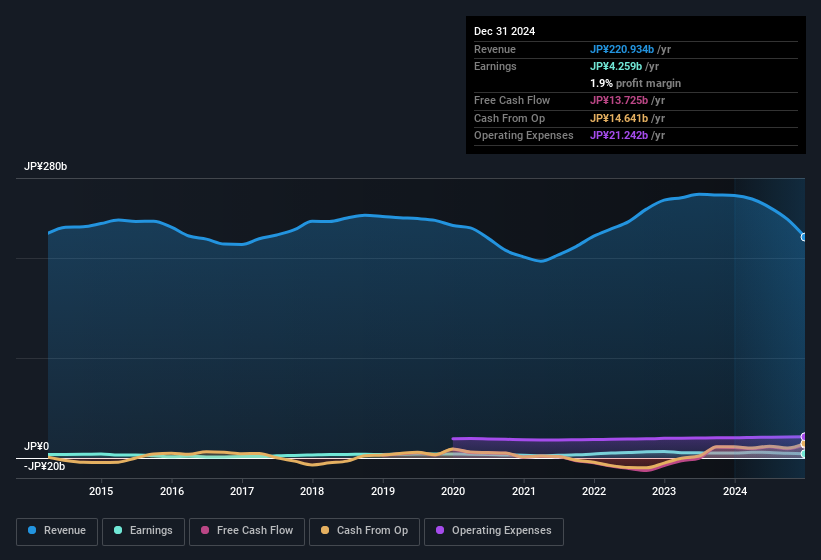

Check out our latest analysis for Ryoden

Zooming In On Ryoden's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. The ratio shows us how much a company's profit exceeds its FCF.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Over the twelve months to December 2024, Ryoden recorded an accrual ratio of -0.15. That indicates that its free cash flow quite significantly exceeded its statutory profit. Indeed, in the last twelve months it reported free cash flow of JP¥14b, well over the JP¥4.26b it reported in profit. Ryoden's free cash flow improved over the last year, which is generally good to see.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Ryoden.

Our Take On Ryoden's Profit Performance

As we discussed above, Ryoden has perfectly satisfactory free cash flow relative to profit. Based on this observation, we consider it likely that Ryoden's statutory profit actually understates its earnings potential! And the EPS is up 5.1% annually, over the last three years. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you want to do dive deeper into Ryoden, you'd also look into what risks it is currently facing. You'd be interested to know, that we found 1 warning sign for Ryoden and you'll want to know about this.

This note has only looked at a single factor that sheds light on the nature of Ryoden's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8084

Ryoden

Sells factory automation (FA) systems, cooling and heating systems, information and communication technologies (ICT) and facilities systems, and electronics in Japan and internationally.

Excellent balance sheet established dividend payer.

Market Insights

Community Narratives