Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:7314

We Wouldn't Be Too Quick To Buy Odawara Auto-Machine Mfg. Co., Ltd. (TYO:7314) Before It Goes Ex-Dividend

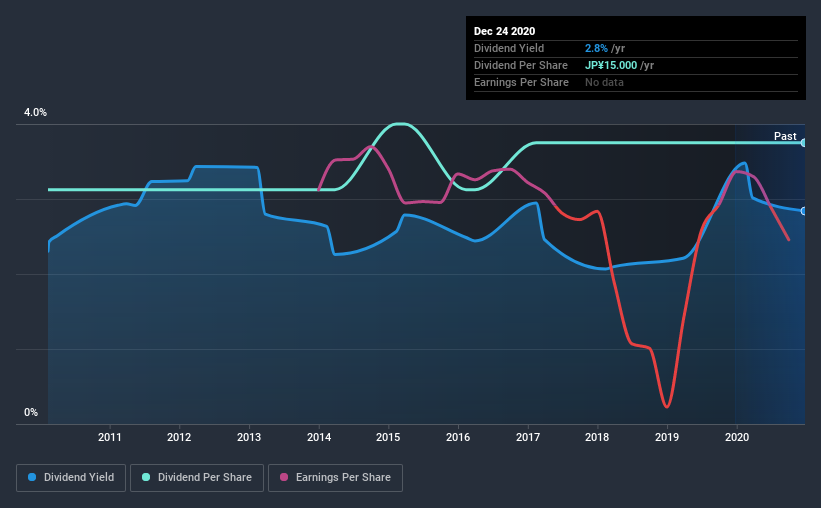

Odawara Auto-Machine Mfg. Co., Ltd. (TYO:7314) is about to trade ex-dividend in the next 3 days. You can purchase shares before the 29th of December in order to receive the dividend, which the company will pay on the 26th of March.

Odawara Auto-Machine Mfg's upcoming dividend is JP¥15.00 a share, following on from the last 12 months, when the company distributed a total of JP¥15.00 per share to shareholders. Last year's total dividend payments show that Odawara Auto-Machine Mfg has a trailing yield of 2.8% on the current share price of ¥528. If you buy this business for its dividend, you should have an idea of whether Odawara Auto-Machine Mfg's dividend is reliable and sustainable. So we need to check whether the dividend payments are covered, and if earnings are growing.

Check out our latest analysis for Odawara Auto-Machine Mfg

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Odawara Auto-Machine Mfg paid a dividend last year despite being unprofitable. This might be a one-off event, but it's not a sustainable state of affairs in the long run. Given that the company reported a loss last year, we now need to see if it generated enough free cash flow to fund the dividend. If Odawara Auto-Machine Mfg didn't generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. It paid out 2.0% of its free cash flow as dividends last year, which is conservatively low.

Click here to see how much of its profit Odawara Auto-Machine Mfg paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If earnings fall far enough, the company could be forced to cut its dividend. Odawara Auto-Machine Mfg reported a loss last year, and the general trend suggests its earnings have also been declining in recent years, making us wonder if the dividend is at risk.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Odawara Auto-Machine Mfg has delivered an average of 1.8% per year annual increase in its dividend, based on the past 10 years of dividend payments.

Remember, you can always get a snapshot of Odawara Auto-Machine Mfg's financial health, by checking our visualisation of its financial health, here.

Final Takeaway

From a dividend perspective, should investors buy or avoid Odawara Auto-Machine Mfg? It's hard to get used to Odawara Auto-Machine Mfg paying a dividend despite reporting a loss over the past year. At least the dividend was covered by free cash flow, however. It's not that we think Odawara Auto-Machine Mfg is a bad company, but these characteristics don't generally lead to outstanding dividend performance.

With that in mind though, if the poor dividend characteristics of Odawara Auto-Machine Mfg don't faze you, it's worth being mindful of the risks involved with this business. We've identified 3 warning signs with Odawara Auto-Machine Mfg (at least 1 which is concerning), and understanding them should be part of your investment process.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade Odawara Auto-Machine Mfg, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSE:7314

Odawara Auto-Machine Mfg

Designs, manufactures, sells, and maintains fare collection equipment for route buses and one-man railway vehicles in Japan.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative