Advertisement

R&D ComputerLtd (TSE:3924) Has Announced That It Will Be Increasing Its Dividend To ¥23.00

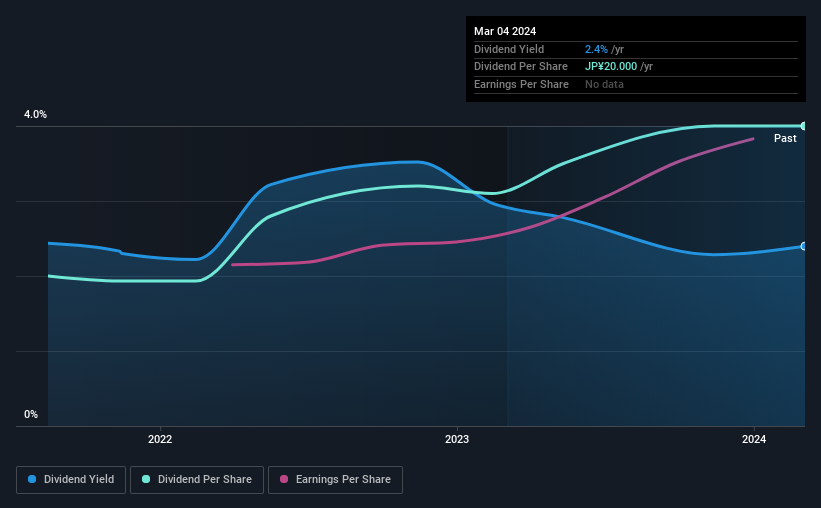

R&D Computer Co.,Ltd.'s (TSE:3924) dividend will be increasing from last year's payment of the same period to ¥23.00 on 7th of June. This will take the annual payment to 2.4% of the stock price, which is above what most companies in the industry pay.

View our latest analysis for R&D ComputerLtd

R&D ComputerLtd's Payment Has Solid Earnings Coverage

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. However, R&D ComputerLtd's earnings easily cover the dividend. This means that most of its earnings are being retained to grow the business.

Looking forward, earnings per share could rise by 12.2% over the next year if the trend from the last few years continues. If the dividend continues on this path, the payout ratio could be 62% by next year, which we think can be pretty sustainable going forward.

R&D ComputerLtd Doesn't Have A Long Payment History

The company has maintained a consistent dividend for a few years now, but we would like to see a longer track record before relying on it. The dividend has gone from an annual total of ¥10.00 in 2021 to the most recent total annual payment of ¥20.00. This means that it has been growing its distributions at 26% per annum over that time. It is always nice to see strong dividend growth, but with such a short payment history we wouldn't be inclined to rely on it until a longer track record can be developed.

The Dividend Looks Likely To Grow

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. We are encouraged to see that R&D ComputerLtd has grown earnings per share at 12% per year over the past five years. R&D ComputerLtd definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

We Really Like R&D ComputerLtd's Dividend

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Distributions are quite easily covered by earnings, which are also being converted to cash flows. All of these factors considered, we think this has solid potential as a dividend stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 3 warning signs for R&D ComputerLtd that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3924

R&D ComputerLtd

Provides system integration, infrastructure, package, cloud, and embedded control system solutions in Japan.

Excellent balance sheet average dividend payer.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Gain Therapeutics ·

The Market Is Sleeping on This Parkinson's Biotech - And I Think That's a Mistake

Fair Value:US$7.672.0% undervalued

40 followersusers have followed this narrative

2 commentsusers have commented on this narrative

20 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.233.9% undervalued

62 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

TE

TechMegaTrends on Bambuser ·

Bambuser is today the only listed company in Europe that simultaneously possesses an 85% gross margin, proprietary AI infrastructure for the

Fair Value:SEK 238.2685.7% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

HE

HedgeY on Constellium ·

Constellium jet another cyclical aluminum processor, or a mispriced aluminum platform?

Fair Value:US$3413.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

WI

WIn2026 on CoreWeave ·

Deep Dive: Assessing the Sustainability of CRWV’s Compute-as-a-Service Model

Fair Value:US$7066.9% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on Moody's ·

MCO 04-2026

Fair Value:US$159186.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

Martimmfonseca on Autodesk ·

Autodesk Could Reach $330–$378 Over the Next Five Years

Fair Value:US$33026.7% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3957.0% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.233.9% undervalued

62 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5727.1% undervalued

1372 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

GT

GT1 on Gulf Keystone Petroleum ·

Have been in and out of this one and Genel for years. I think that delayed and non payments are a bi...

0

|0