- South Korea

- /

- Machinery

- /

- KOSE:A064350

Three Stocks Estimated To Be Undervalued In January 2025

Reviewed by Simply Wall St

As global markets navigate mixed performances and economic uncertainties, investors continue to seek opportunities amidst fluctuating indices and revised GDP forecasts. In this environment, identifying undervalued stocks becomes crucial for those looking to capitalize on potential growth while managing risk.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Corporativo Fragua. de (BMV:FRAGUA B) | MX$633.00 | MX$1257.07 | 49.6% |

| Fevertree Drinks (AIM:FEVR) | £6.605 | £13.12 | 49.7% |

| Elekta (OM:EKTA B) | SEK61.05 | SEK121.91 | 49.9% |

| Atlas Arteria (ASX:ALX) | A$4.83 | A$9.65 | 50% |

| Zhende Medical (SHSE:603301) | CN¥20.99 | CN¥41.92 | 49.9% |

| ReadyTech Holdings (ASX:RDY) | A$3.14 | A$6.25 | 49.8% |

| TSE (KOSDAQ:A131290) | ₩43100.00 | ₩85771.31 | 49.8% |

| Mr. Cooper Group (NasdaqCM:COOP) | US$94.43 | US$187.71 | 49.7% |

| Vogo (ENXTPA:ALVGO) | €2.91 | €5.81 | 49.9% |

| iFLYTEKLTD (SZSE:002230) | CN¥45.21 | CN¥89.80 | 49.7% |

Here's a peek at a few of the choices from the screener.

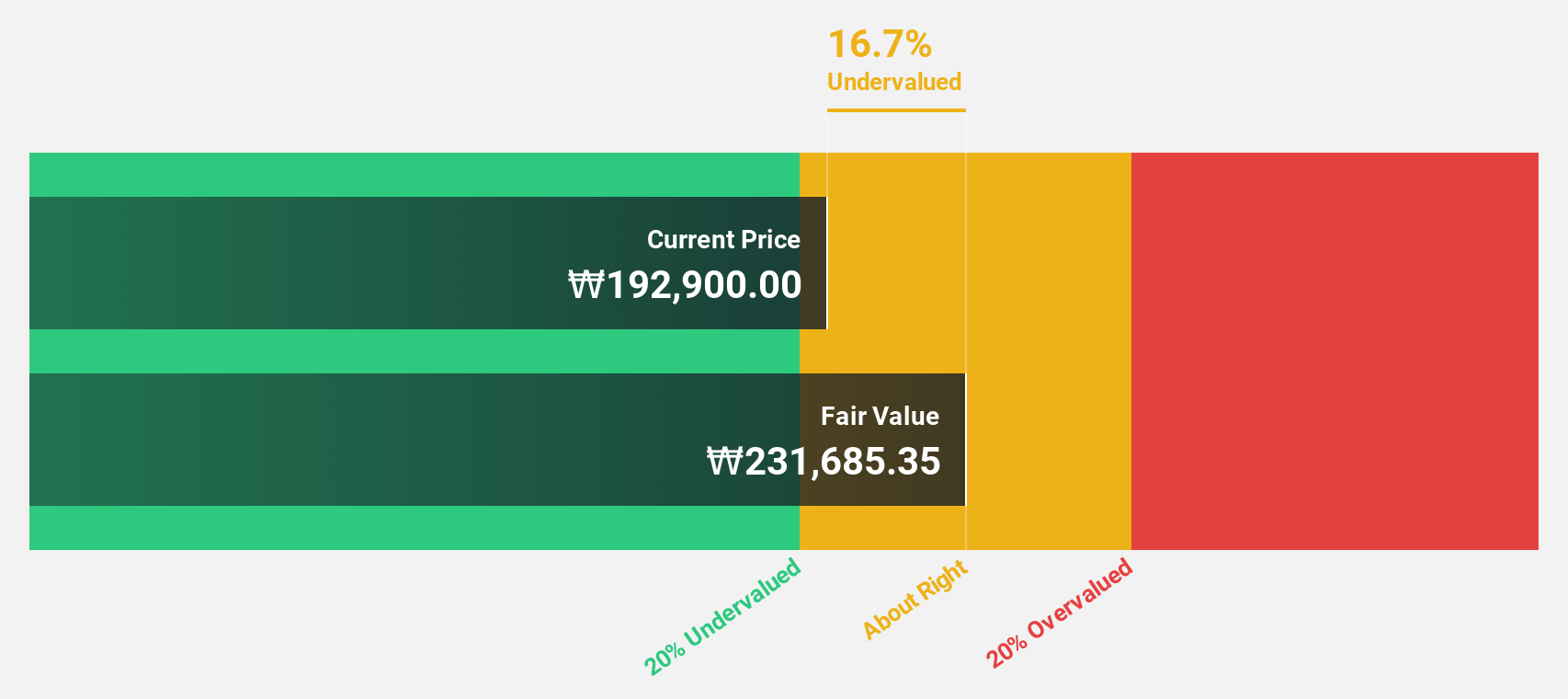

Hyundai Rotem (KOSE:A064350)

Overview: Hyundai Rotem Company manufactures and sells railway vehicles, defense systems, and plants and machinery both in South Korea and internationally, with a market cap of ₩5.71 trillion.

Operations: The company's revenue segments are comprised of the Rail Solution segment at ₩1.49 trillion, the Defense Solution segment at ₩1.89 trillion, and the Plant Segment at ₩550.99 million.

Estimated Discount To Fair Value: 48.9%

Hyundai Rotem is trading at ₩55,600, substantially below its estimated fair value of ₩108,856, making it highly undervalued based on discounted cash flow analysis. The company's revenue grew to ₩2.94 trillion for the first nine months of 2024 from ₩2.60 trillion a year earlier. Despite earnings growth forecasts lagging behind the broader Korean market, Hyundai Rotem's significant earnings increase of 29.7% last year underscores its potential as an undervalued investment opportunity.

- In light of our recent growth report, it seems possible that Hyundai Rotem's financial performance will exceed current levels.

- Unlock comprehensive insights into our analysis of Hyundai Rotem stock in this financial health report.

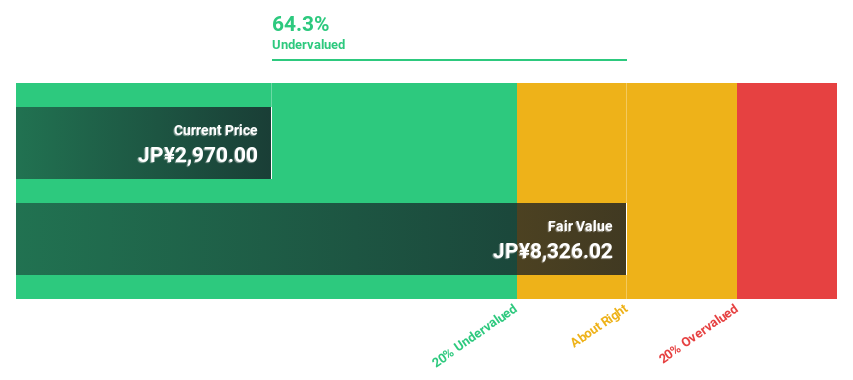

Tri Chemical Laboratories (TSE:4369)

Overview: Tri Chemical Laboratories Inc. specializes in producing chemical products for semiconductors, coatings, optical fibers, solar cells, and compound semiconductors with a market cap of ¥91.80 billion.

Operations: The company's revenue is primarily derived from its High-Purity Chemical Compound Business for Manufacturing Semiconductors, which generated ¥16.14 billion.

Estimated Discount To Fair Value: 47.2%

Tri Chemical Laboratories is trading at ¥3,110, well below its estimated fair value of ¥5,890.33, highlighting its undervaluation based on discounted cash flow analysis. Analysts predict a 53.5% rise in stock price, supported by revenue growth forecasts of 22.4% annually—outpacing the JP market's 4.2%. Despite high share price volatility and a forecasted low return on equity of 19.7%, earnings are expected to grow significantly at 31% per year over three years.

- Our earnings growth report unveils the potential for significant increases in Tri Chemical Laboratories' future results.

- Get an in-depth perspective on Tri Chemical Laboratories' balance sheet by reading our health report here.

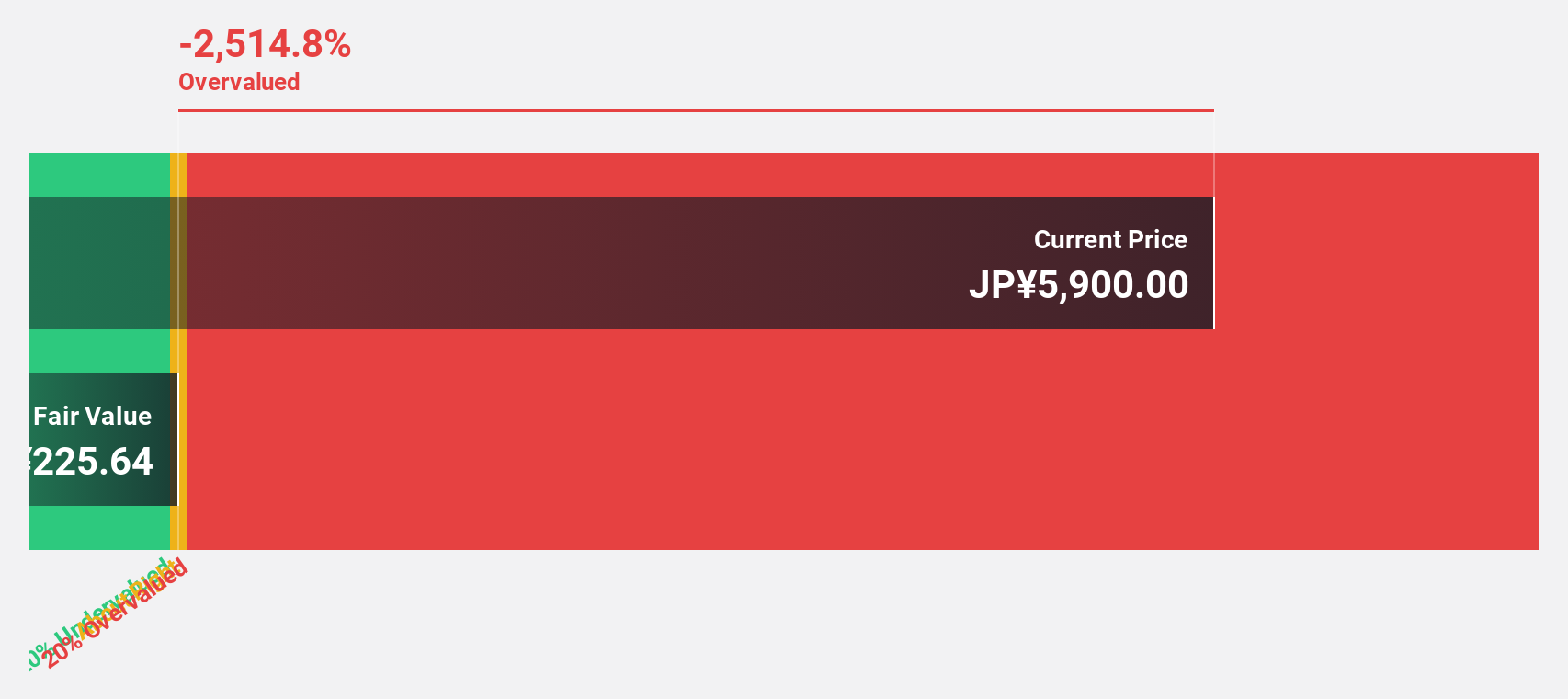

Shinko Electric Industries (TSE:6967)

Overview: Shinko Electric Industries Co., Ltd. develops, produces, and sells various semiconductor packages in Japan with a market cap of ¥771.93 billion.

Operations: The company's revenue segments include Metal Package at ¥78.65 billion and Plastic Package at ¥126.93 billion.

Estimated Discount To Fair Value: 49.4%

Shinko Electric Industries is trading at ¥5,869, significantly below its fair value estimate of ¥11,606.47, indicating strong undervaluation based on discounted cash flow analysis. Earnings are projected to grow 21.7% annually over the next three years—outpacing the Japanese market's growth rate of 7.8%. However, revenue growth is slower at 8.2% per year and return on equity is forecasted to be modest at 12.7%. Recent guidance anticipates net sales of ¥243.3 billion for fiscal year ending March 2025.

- Our growth report here indicates Shinko Electric Industries may be poised for an improving outlook.

- Click here to discover the nuances of Shinko Electric Industries with our detailed financial health report.

Taking Advantage

- Investigate our full lineup of 896 Undervalued Stocks Based On Cash Flows right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hyundai Rotem might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A064350

Hyundai Rotem

Manufactures and sells railway vehicles, defense systems, and plants and machinery in South Korea and internationally.

Flawless balance sheet and good value.