Something seems to have caught the market’s eye with ROHM (TSE:6963) lately, even though there isn’t a headline-grabbing event behind the recent move. That alone can pique the interest of current shareholders debating whether to hold, buy, or trim their positions. Sometimes, when a stock moves without a major news announcement, it raises a bigger question: does the market know something we don’t, or is it simply a repricing based on fundamentals?

Taking a step back, ROHM has seen steady momentum recently. Over the past year, shares have gained 45%, with nearly 25% growth in the past three months and a 38% return year-to-date. The longer-term view is a bit more mixed, as the past three years were negative overall, but the stock has bounced back this year with renewed interest. Perhaps investors are repositioning in anticipation of future growth or improved profitability.

After a move like this, it is only fair to wonder: is the current price still a bargain, or are investors already paying up for all that upside?

Advertisement

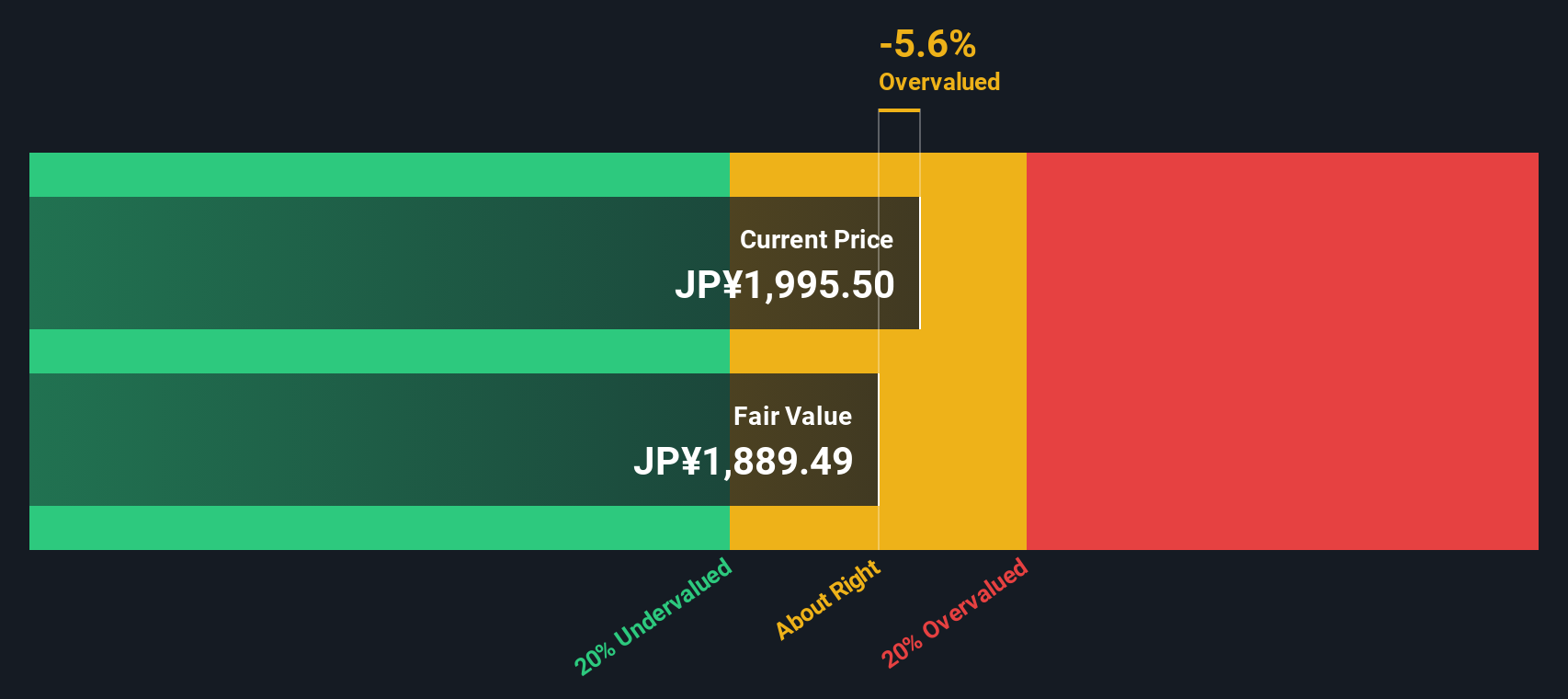

Most Popular Narrative: 4% Overvalued

According to the most widely followed narrative, ROHM’s shares are trading slightly above fair value based on current consensus forecasts and risk assumptions.

ROHM is planning to increase its production capacity and efficiency for SiC (silicon carbide) power devices, correlating with expected battery EV market growth. This should enhance revenue and earnings as demand eventually picks up. The company is implementing a new organizational structure to better cater to customer needs and market applications. This aims to improve sales and potentially increase net margins by offering more integrated, solution-based proposals.

What makes analysts think ROHM deserves its premium price? It is all in their bold long-term assumptions about future profits and revenue momentum. Want to peek into the projected transformation, powered by new technologies and strategic changes, that could reshape the company’s margins and valuation? The full narrative reveals the big financial bets underpinning today’s fair value.

However, persistent declines in industrial demand or unachieved cost reductions could put pressure on ROHM’s turnaround hopes and cast doubt on the bullish narrative.

Another View: SWS DCF Model Puts the Spotlight on Value

Switching gears, our DCF model takes a more cautious approach, suggesting the stock is currently priced above what its future cash flows might justify. Could the market be betting too far ahead?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ROHM for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own ROHM Narrative

Of course, if you see the market differently or want to dig into the details yourself, you can craft your own perspective in just a few minutes. Do it your way

Smart investors never stop at just one stock. Take the next step and find your edge in today’s markets using these powerful screening ideas from Simply Wall Street:

Uncover tomorrow’s overlooked gems with penny stocks with strong financials. This tool helps identify financially strong up-and-comers that have plenty of room to surprise on the upside.

Zero in on high-yielding opportunities by using dividend stocks with yields > 3% to spot companies offering stable dividends above 3% for those seeking consistent income streams.

Catch the wave of technological disruption with AI penny stocks, which highlights ambitious companies leading advancements in artificial intelligence innovation and growth potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies