Advertisement

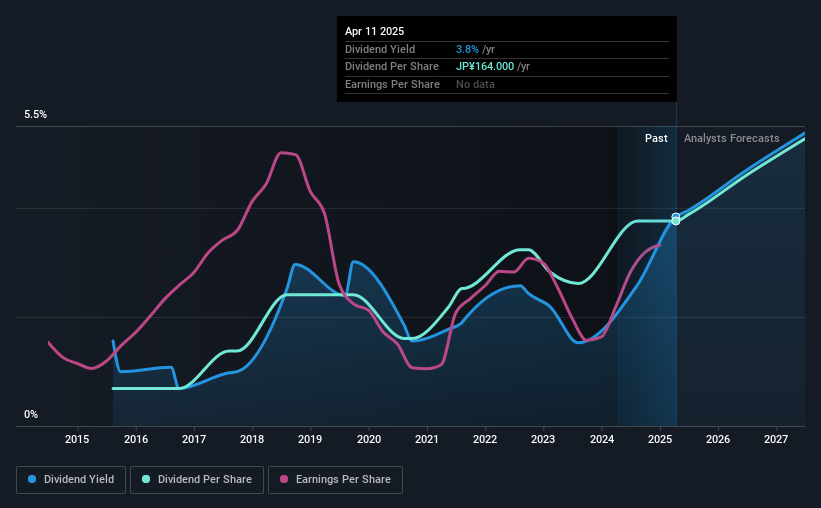

ULVAC, Inc. (TSE:6728) will increase its dividend from last year's comparable payment on the 30th of September to ¥164.00. This makes the dividend yield 3.8%, which is above the industry average.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. ULVAC's stock price has reduced by 32% in the last 3 months, which is not ideal for investors and can explain a sharp increase in the dividend yield.

ULVAC's Projected Earnings Seem Likely To Cover Future Distributions

If the payments aren't sustainable, a high yield for a few years won't matter that much. Before making this announcement, ULVAC was paying a whopping 226% as a dividend, but this only made up 30% of its overall earnings. While the business may be attempting to set a balanced dividend policy, a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

Looking forward, earnings per share is forecast to rise by 12.8% over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 35%, which is in the range that makes us comfortable with the sustainability of the dividend.

View our latest analysis for ULVAC

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2015, the annual payment back then was ¥30.00, compared to the most recent full-year payment of ¥164.00. This implies that the company grew its distributions at a yearly rate of about 19% over that duration. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

ULVAC Could Grow Its Dividend

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. ULVAC has impressed us by growing EPS at 9.3% per year over the past five years. A low payout ratio and decent growth suggests that the company is reinvesting well, and it also has plenty of room to increase the dividend over time.

Our Thoughts On ULVAC's Dividend

Overall, we always like to see the dividend being raised, but we don't think ULVAC will make a great income stock. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. For example, we've picked out 1 warning sign for ULVAC that investors should know about before committing capital to this stock. Is ULVAC not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6728

ULVAC

Engages in vacuum equipment and applications business in Japan and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.9% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.1% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|36.0% overvalued

DA

Community Contributor