In a week marked by cautious earnings reports and economic data, global markets have experienced fluctuations, with major indices like the Nasdaq Composite and S&P MidCap 400 reaching record highs before retreating. Amidst this volatility, growth stocks have lagged behind value shares, as investors navigate an environment of mixed economic signals and geopolitical uncertainties. In such conditions, companies with significant insider ownership often attract attention due to the confidence their leaders demonstrate in their long-term potential. This article explores three growth companies where insiders hold substantial stakes, suggesting a strong alignment between management interests and shareholder value.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Laopu Gold (SEHK:6181) | 36.4% | 33% |

| Medley (TSE:4480) | 34% | 30.4% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.7% | 49.1% |

| Findi (ASX:FND) | 34.8% | 64.8% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

Let's take a closer look at a couple of our picks from the screened companies.

China Youran Dairy Group (SEHK:9858)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: China Youran Dairy Group Limited is an investment holding company that operates as an integrated provider of products and services in the upstream dairy industry in the People's Republic of China, with a market cap of HK$5.49 billion.

Operations: The company's revenue is derived from two main segments: the Raw Milk Business, which generated CN¥14.07 billion, and Comprehensive Ruminant Farming Solutions, contributing CN¥7.65 billion.

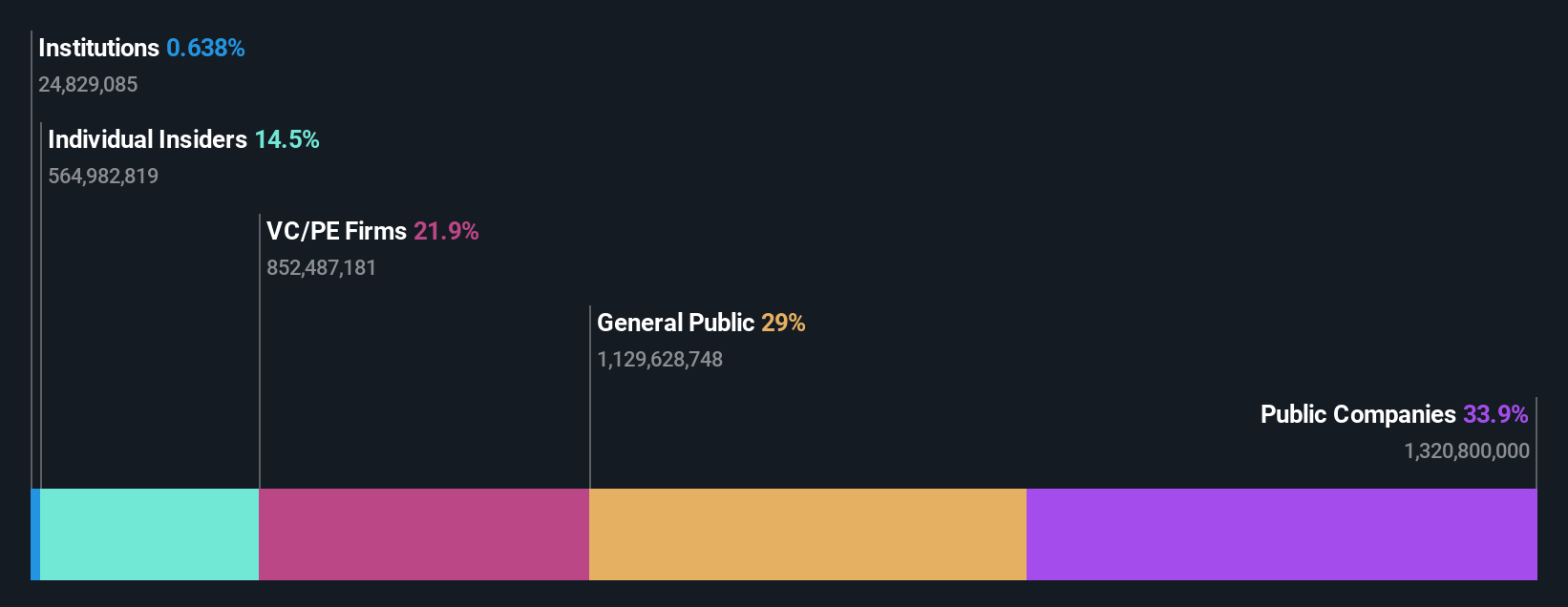

Insider Ownership: 14.5%

China Youran Dairy Group's revenue is projected to grow at 9% annually, outpacing the Hong Kong market average. Despite past shareholder dilution and high debt levels, the company is trading at a good value compared to peers. Analysts expect profitability within three years, with earnings forecasted to increase significantly by 90.27% annually. Recent results showed improved performance with sales reaching CNY 10 billion and a reduced net loss of CNY 330.87 million for H1 2024.

- Click here and access our complete growth analysis report to understand the dynamics of China Youran Dairy Group.

- Our valuation report unveils the possibility China Youran Dairy Group's shares may be trading at a discount.

Changzhou Tenglong AutoPartsCo.Ltd (SHSE:603158)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Changzhou Tenglong AutoPartsCo., Ltd. is engaged in the research, development, manufacturing, and sale of auto parts both in China and internationally, with a market cap of CN¥4.05 billion.

Operations: The company's revenue segments focus on the research, development, manufacturing, and sale of auto parts in both domestic and international markets.

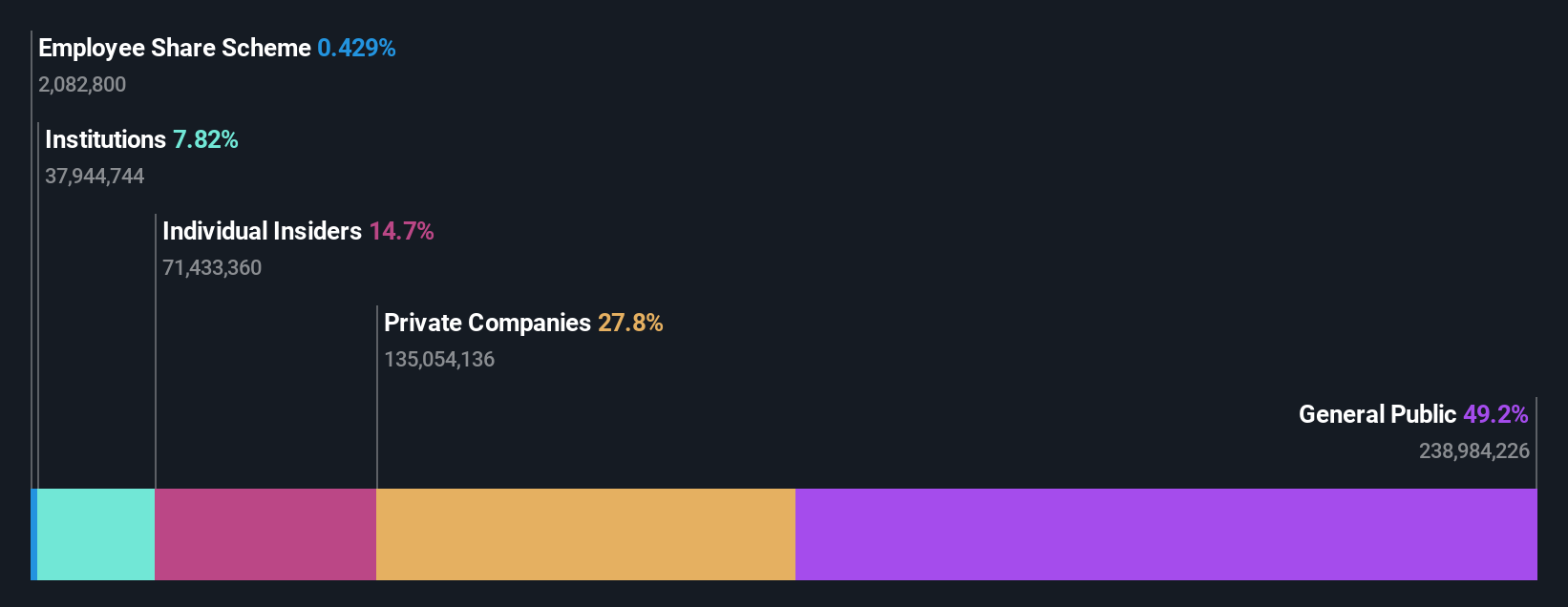

Insider Ownership: 16.7%

Changzhou Tenglong AutoPartsCo.,Ltd. demonstrates potential for growth, with recent earnings showing a net income increase to CNY 236.43 million from CNY 140.39 million year-on-year. The company's revenue is forecasted to grow at 27.7% annually, surpassing the CN market average of 14%. Despite trading at a favorable price-to-earnings ratio of 13.9x compared to the market's 34.4x, its dividend yield is not well supported by free cash flows and insider ownership data is limited.

- Navigate through the intricacies of Changzhou Tenglong AutoPartsCo.Ltd with our comprehensive analyst estimates report here.

- Our comprehensive valuation report raises the possibility that Changzhou Tenglong AutoPartsCo.Ltd is priced lower than what may be justified by its financials.

NEXTAGE (TSE:3186)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: NEXTAGE Co., Ltd. operates in Japan, focusing on the sale of new and used cars, with a market cap of ¥122.62 billion.

Operations: The company's revenue is primarily derived from its automobile sales and related ancillary businesses, totaling ¥515.65 billion.

Insider Ownership: 38.3%

NEXTAGE's earnings are expected to grow significantly at 25% annually, outpacing the JP market growth of 8.9%. Despite trading at a substantial discount of 64.4% below its estimated fair value, its profit margins have declined from last year. The company's revenue is projected to increase by 10.9% per year, faster than the market but not exceptionally high. However, dividends remain unsustainable due to inadequate free cash flow coverage and there is no recent insider trading activity reported.

- Get an in-depth perspective on NEXTAGE's performance by reading our analyst estimates report here.

- Upon reviewing our latest valuation report, NEXTAGE's share price might be too pessimistic.

Turning Ideas Into Actions

- Embark on your investment journey to our 1528 Fast Growing Companies With High Insider Ownership selection here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:9858

China Youran Dairy Group

An investment holding company, operates as an integrated provider of products and services in the upstream dairy industry in the People's Republic of China.

Reasonable growth potential and fair value.