Advertisement

RACCOON HOLDINGS (TSE:3031) Is Reducing Its Dividend To ¥5.00

RACCOON HOLDINGS, Inc. (TSE:3031) has announced that on 24th of July, it will be paying a dividend of¥5.00, which a reduction from last year's comparable dividend. This means the annual payment is 1.7% of the current stock price, which is above the average for the industry.

Check out our latest analysis for RACCOON HOLDINGS

RACCOON HOLDINGS' Earnings Easily Cover The Distributions

If the payments aren't sustainable, a high yield for a few years won't matter that much. Prior to this announcement, the company was paying out 95% of what it was earning, however the dividend was quite comfortably covered by free cash flows at a cash payout ratio of only 22%. Generally, we think cash is more important than accounting measures of profit, so with the cash flows easily covering the dividend, we don't think there is much reason to worry.

Looking forward, earnings per share is forecast to rise exponentially over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 26%, which would make us comfortable with the dividend's sustainability, despite the levels currently being elevated.

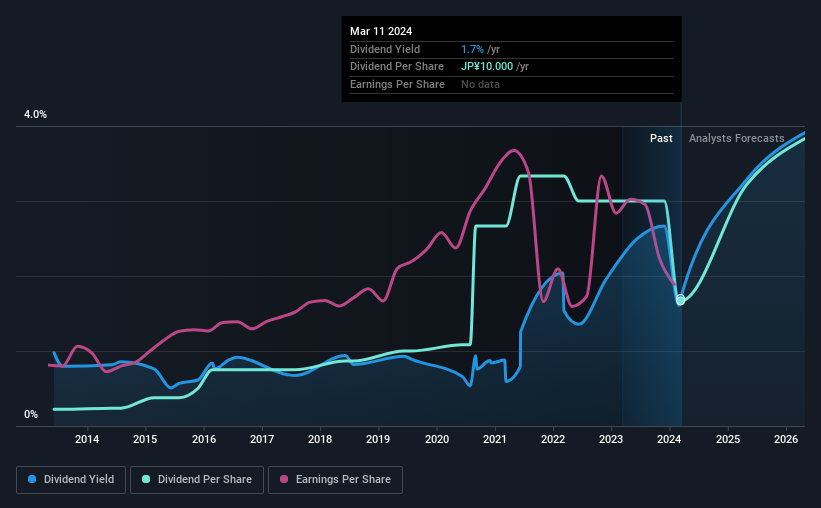

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. Since 2014, the dividend has gone from ¥1.33 total annually to ¥10.00. This works out to be a compound annual growth rate (CAGR) of approximately 22% a year over that time. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

The Dividend's Growth Prospects Are Limited

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Earnings have grown at around 2.8% a year for the past five years, which isn't massive but still better than seeing them shrink. The company is paying out a lot of its profits, even though it is growing those profits pretty slowly. This gives limited room for the company to raise the dividend in the future.

In Summary

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've picked out 4 warning signs for RACCOON HOLDINGS that investors should know about before committing capital to this stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3031

RACCOON HOLDINGS

RACCOON HOLDINGS, Inc. creates and provides infrastructure BtoB transactions in Japan.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor