Advertisement

- Japan

- /

- Specialty Stores

- /

- TSE:2681

3 Stocks That May Be Priced Below Their Estimated Value In December 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate the complexities of interest rate adjustments and political uncertainties, investors are keenly observing the implications for stock valuations. With U.S. stocks experiencing volatility due to cautious Federal Reserve commentary and looming government shutdown fears, opportunities may arise in identifying stocks that are priced below their estimated value. In such a climate, a good stock might be one that demonstrates strong fundamentals and resilience amidst economic fluctuations, potentially offering value when broader market sentiment is subdued.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| HangzhouS MedTech (SHSE:688581) | CN¥61.57 | CN¥123.87 | 50.3% |

| Shenzhen Lifotronic Technology (SHSE:688389) | CN¥15.39 | CN¥30.81 | 50.1% |

| Sudarshan Chemical Industries (BSE:506655) | ₹1133.35 | ₹2252.97 | 49.7% |

| Lindab International (OM:LIAB) | SEK226.40 | SEK450.98 | 49.8% |

| Absolent Air Care Group (OM:ABSO) | SEK255.00 | SEK509.76 | 50% |

| NCSOFT (KOSE:A036570) | ₩205500.00 | ₩409953.04 | 49.9% |

| STIF Société anonyme (ENXTPA:ALSTI) | €24.60 | €49.15 | 49.9% |

| Informa (LSE:INF) | £7.992 | £15.92 | 49.8% |

| Surgical Science Sweden (OM:SUS) | SEK159.10 | SEK317.10 | 49.8% |

| RENK Group (DB:R3NK) | €18.342 | €36.46 | 49.7% |

Let's dive into some prime choices out of the screener.

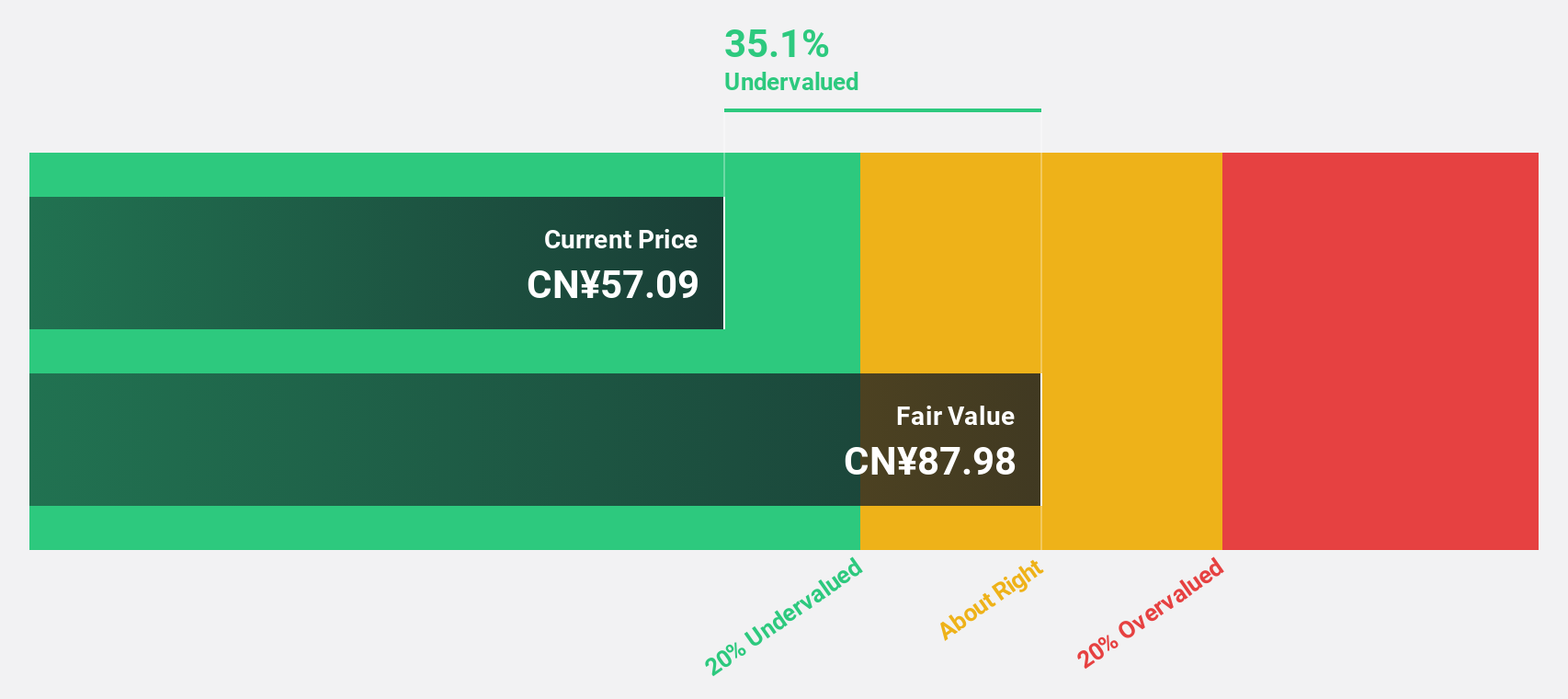

Ningbo Deye Technology Group (SHSE:605117)

Overview: Ningbo Deye Technology Group Co., Ltd. produces and sells heat exchangers, inverters, and dehumidifiers across China, the UK, the US, Germany, India, and internationally with a market cap of CN¥54.35 billion.

Operations: Ningbo Deye Technology Group's revenue is generated from the production and sales of heat exchangers, inverters, and dehumidifiers across various international markets including China, the UK, the US, Germany, and India.

Estimated Discount To Fair Value: 35%

Ningbo Deye Technology Group is trading at CN¥84.63, significantly below its estimated fair value of CN¥130.21, indicating potential undervaluation based on cash flows. Revenue growth is expected to outpace the market at 29.3% annually, with earnings projected to increase significantly by 26.5% per year over the next three years. Recent earnings reports show substantial improvement, with net income rising to CN¥2.24 billion from CN¥1.57 billion a year ago despite shareholder dilution concerns.

- Our expertly prepared growth report on Ningbo Deye Technology Group implies its future financial outlook may be stronger than recent results.

- Click here to discover the nuances of Ningbo Deye Technology Group with our detailed financial health report.

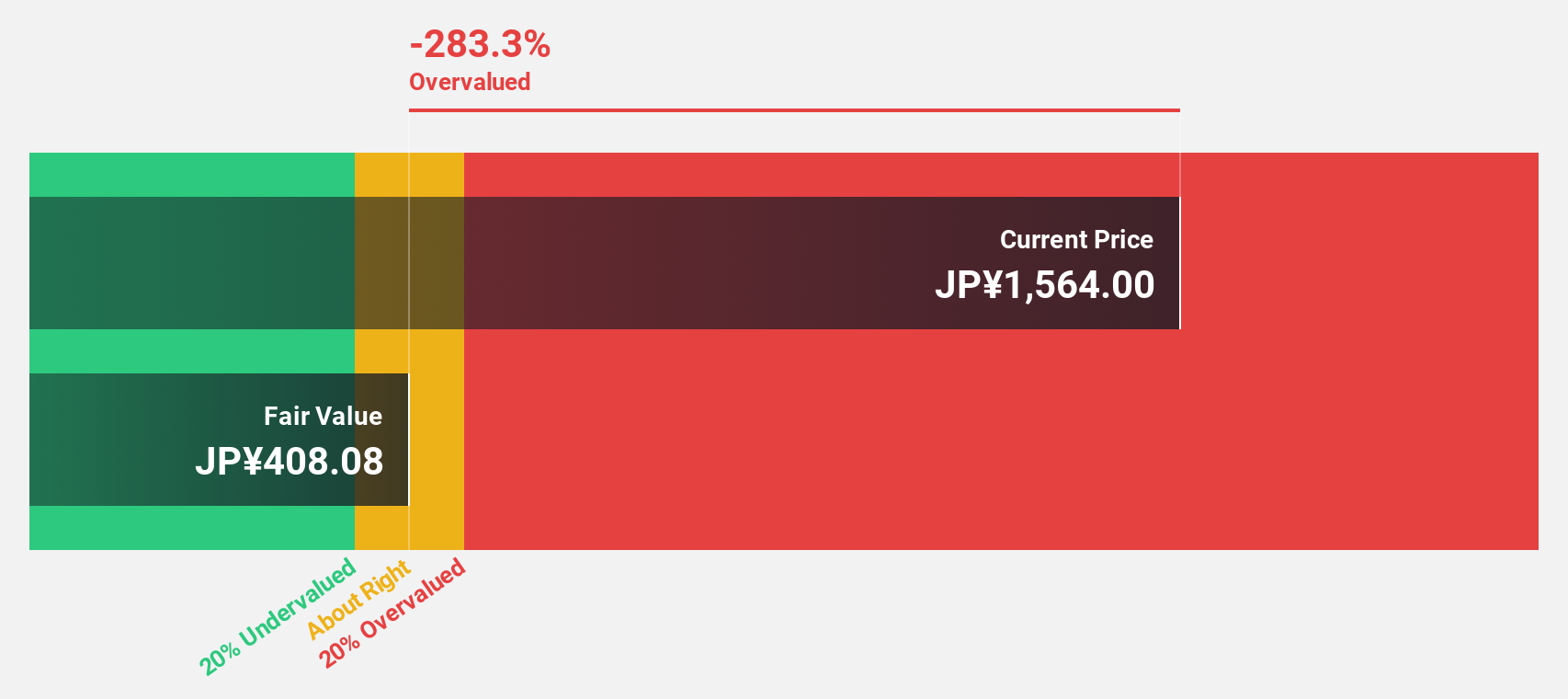

Geo Holdings (TSE:2681)

Overview: Geo Holdings Corporation operates in the amusement industry in Japan, with a market capitalization of ¥61.63 billion.

Operations: The company generates revenue from Retail Services amounting to ¥417.81 million.

Estimated Discount To Fair Value: 24.4%

Geo Holdings is trading at ¥1586, 24.4% below its estimated fair value of ¥2098.65, highlighting potential undervaluation based on cash flows. Earnings are projected to grow significantly by 20.6% annually, outpacing the JP market's growth rate of 8%. However, the dividend yield of 2.14% is not well covered by free cash flows, and return on equity is forecasted to be low at 10.8% in three years despite recent dividend increases to ¥17 per share.

- According our earnings growth report, there's an indication that Geo Holdings might be ready to expand.

- Dive into the specifics of Geo Holdings here with our thorough financial health report.

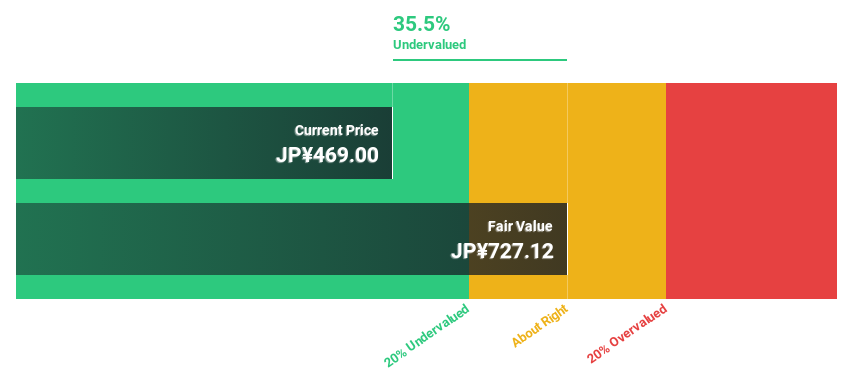

Solasto (TSE:6197)

Overview: Solasto Corporation offers medical outsourcing services to healthcare institutions in Japan and has a market capitalization of ¥42.72 billion.

Operations: The company's revenue is primarily derived from its Medical Business at ¥70.61 billion, followed by the Nursing Care Business at ¥55.20 billion, and the Children's Business at ¥10.32 billion.

Estimated Discount To Fair Value: 36.9%

Solasto is trading at ¥459, significantly below its estimated fair value of ¥727.57, indicating potential undervaluation based on cash flows. Despite earnings growth forecasts of 23.49% annually, surpassing the JP market's 8%, the dividend yield of 4.36% is not well covered by earnings. The company's debt coverage by operating cash flow is inadequate, and profit margins have decreased to 0.2% from last year's 3.9%.

- The growth report we've compiled suggests that Solasto's future prospects could be on the up.

- Delve into the full analysis health report here for a deeper understanding of Solasto.

Turning Ideas Into Actions

- Take a closer look at our Undervalued Stocks Based On Cash Flows list of 871 companies by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:2681

Undervalued with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|17.0% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|11.8% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|81.8% undervalued

NO

Community Contributor