Advertisement

- Japan

- /

- Residential REITs

- /

- TSE:3269

Advance Residence Investment (TSE:3269): Valuation Check After New Loan Deals and Property Acquisition Move

Simply Wall St

Reviewed by Simply Wall St

Advance Residence Investment (TSE:3269) just lined up two new loans, including a seven year fixed rate facility, to both refinance obligations and help fund its latest property acquisition, reshaping its balance sheet mix.

See our latest analysis for Advance Residence Investment.

The timing of these loans lines up with a reasonably solid backdrop, with a year to date share price return of 16.12% and a one year total shareholder return of 21.68%, suggesting steady momentum rather than a sudden sentiment shift.

If this kind of balance sheet reshaping has your attention, it might also be worth exploring fast growing stocks with high insider ownership as a way to spot other compelling stories building in the background.

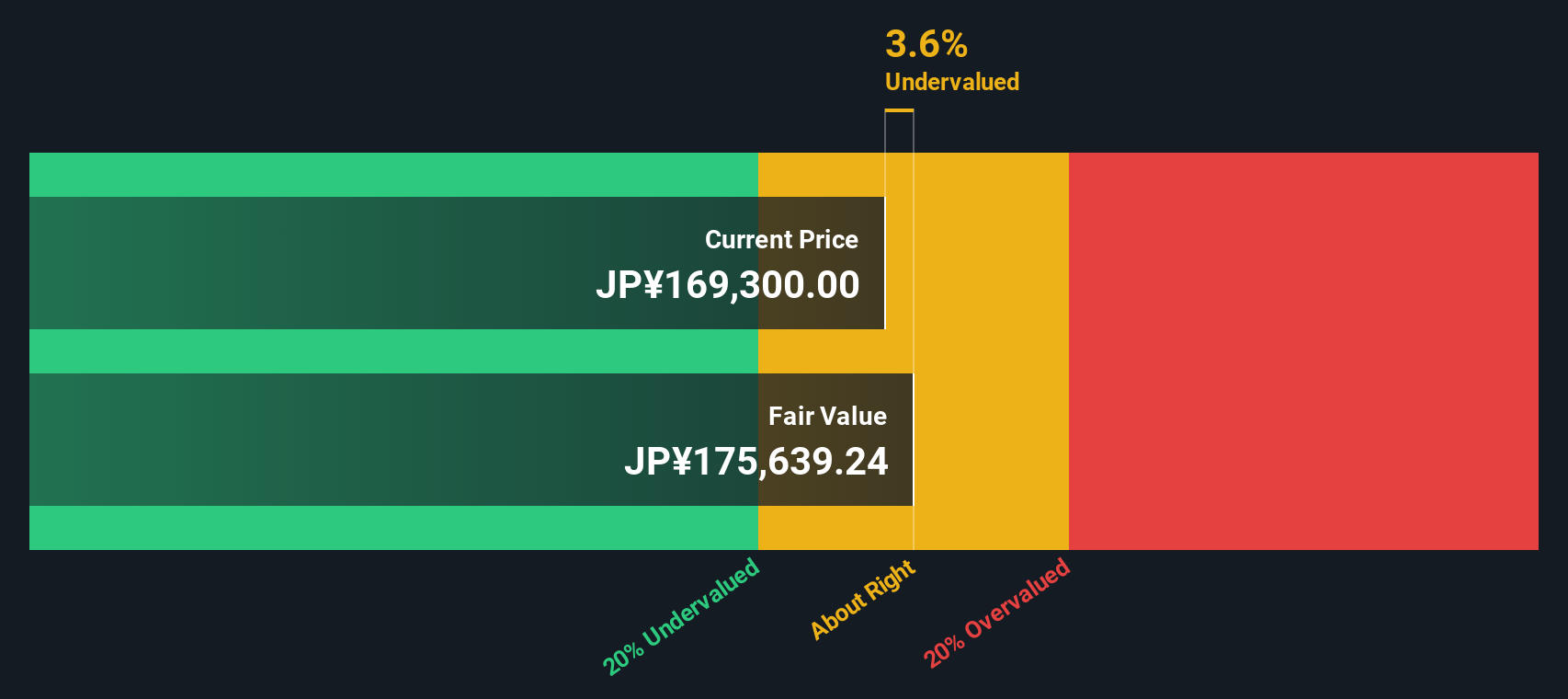

Yet with valuations sitting modestly above analyst targets while intrinsic metrics hint at a discount, investors face a key question: is Advance Residence still a buying opportunity, or is the market already pricing in its future growth?

Most Popular Narrative: 4.2% Overvalued

Compared with the narrative fair value of ¥164,143, Advance Residence Investment's last close at ¥171,100 bakes in a small valuation premium that hinges on precise earnings and margin assumptions.

The analysts have a consensus price target of ¥160687.5 for Advance Residence Investment based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥179000.0, and the most bearish reporting a price target of just ¥138000.0.

Want to see what justifies paying above that fair value line? The narrative leans on steady earnings, firmer margins, and a future profit multiple that assumes muted top line growth but resilient demand. Curious which exact trade offs between revenue, profitability, and discount rate make this premium look acceptable on paper?

Result: Fair Value of ¥164,143 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, higher floating rate exposure and reliance on property sales mean that a turn in interest rates or real estate demand could quickly undercut this valuation premium.

Find out about the key risks to this Advance Residence Investment narrative.

Another View: Cash Flow Says Cheap, Not Costly

While the narrative fair value flags Advance Residence as 4.2% overvalued, our DCF model presents a different picture, suggesting fair value of ¥191,549 versus the current ¥171,100 share price. That 10.7% gap implies investors may be underpaying for long term cash flows. Which lens do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Advance Residence Investment for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 932 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Advance Residence Investment Narrative

If you would rather examine the numbers yourself and reach your own conclusion, you can quickly assemble a custom narrative in just a few minutes, Do it your way.

A great starting point for your Advance Residence Investment research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Advance Residence might be on your radar, but ignoring other opportunities could cost you the next big move. Let the Simply Wall St Screener work for you.

- Capture asymmetrical upside by targeting beaten down names with solid fundamentals through these 3570 penny stocks with strong financials before the broader market catches on.

- Capitalize on structural growth in automation and smart data by narrowing in on these 24 AI penny stocks positioned at the heart of this technological shift.

- Lock in potential bargains by filtering for companies trading below their estimated cash flow value using these 932 undervalued stocks based on cash flows while prices still look attractive.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3269

Advance Residence Investment

Advance Residence Investment Corporation is the largest J-REIT specializing in residential properties and is managed by ITOCHU REIT Management Co., Ltd.

Acceptable track record second-rate dividend payer.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

10 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Marvell Technology ·

The Great Strategy Swap – Selling "Old Auto" to Buy "Future Light"

Fair Value:US$155.3740.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on NVIDIA ·

Not a Bubble, But the "Industrial Revolution 4.0" Engine

Fair Value:US$294.9238.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.6% undervalued

946 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.2% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative