Advertisement

- Japan

- /

- Real Estate

- /

- TSE:8923

Tosei Corporation Just Missed Earnings And Its Revenue Numbers Were Weaker Than Expected

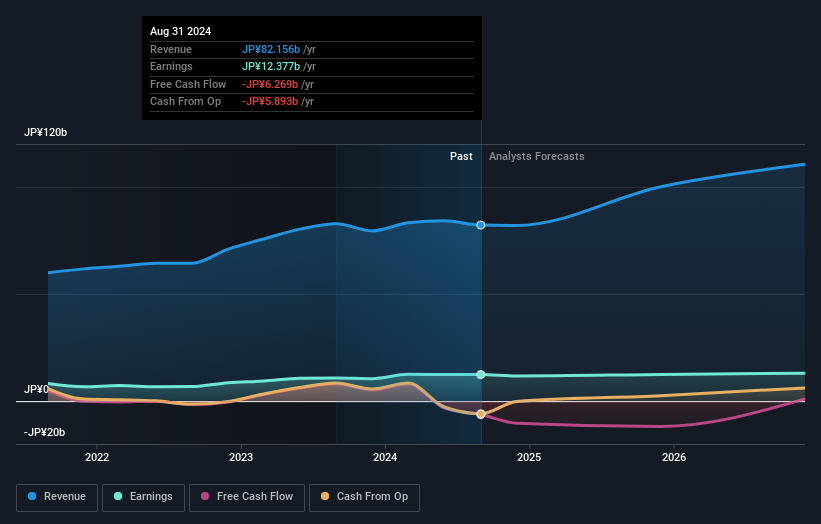

As you might know, Tosei Corporation (TSE:8923) last week released its latest third-quarter, and things did not turn out so great for shareholders. Results look to have been somewhat negative - revenue fell 10.0% short of analyst estimates at JP¥12b, and statutory earnings of JP¥24.00 per share missed forecasts by 6.1%. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Tosei after the latest results.

Check out our latest analysis for Tosei

Taking into account the latest results, the current consensus from Tosei's four analysts is for revenues of JP¥100.1b in 2025. This would reflect a sizeable 22% increase on its revenue over the past 12 months. Statutory per share are forecast to be JP¥260, approximately in line with the last 12 months. Before this earnings report, the analysts had been forecasting revenues of JP¥105.1b and earnings per share (EPS) of JP¥259 in 2025. So it looks like the analysts have become a bit less optimistic after the latest results announcement, with revenues expected to fall even as the company is supposed to maintain EPS.

The average price target was steady at JP¥2,815even though revenue estimates declined; likely suggesting the analysts place a higher value on earnings. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Tosei analyst has a price target of JP¥2,930 per share, while the most pessimistic values it at JP¥2,700. With such a narrow range of valuations, the analysts apparently share similar views on what they think the business is worth.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that Tosei's rate of growth is expected to accelerate meaningfully, with the forecast 17% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 6.2% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 4.1% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Tosei to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. They also downgraded Tosei's revenue estimates, but industry data suggests that it is expected to grow faster than the wider industry. Even so, earnings are more important to the intrinsic value of the business. The consensus price target held steady at JP¥2,815, with the latest estimates not enough to have an impact on their price targets.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple Tosei analysts - going out to 2026, and you can see them free on our platform here.

Before you take the next step you should know about the 2 warning signs for Tosei (1 is a bit concerning!) that we have uncovered.

Valuation is complex, but we're here to simplify it.

Discover if Tosei might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8923

Tosei

Operates in the revitalization, development, rental, fund and consulting, property management, and hotel businesses in Japan.

Fair value with acceptable track record.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4039.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6087.9% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.57.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15082.3% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative