Advertisement

- Japan

- /

- Real Estate

- /

- TSE:3003

Should Hulic’s Raised Outlook and Dividend Hike Prompt a Closer Look From TSE:3003 Investors?

Simply Wall St

Reviewed by Sasha Jovanovic

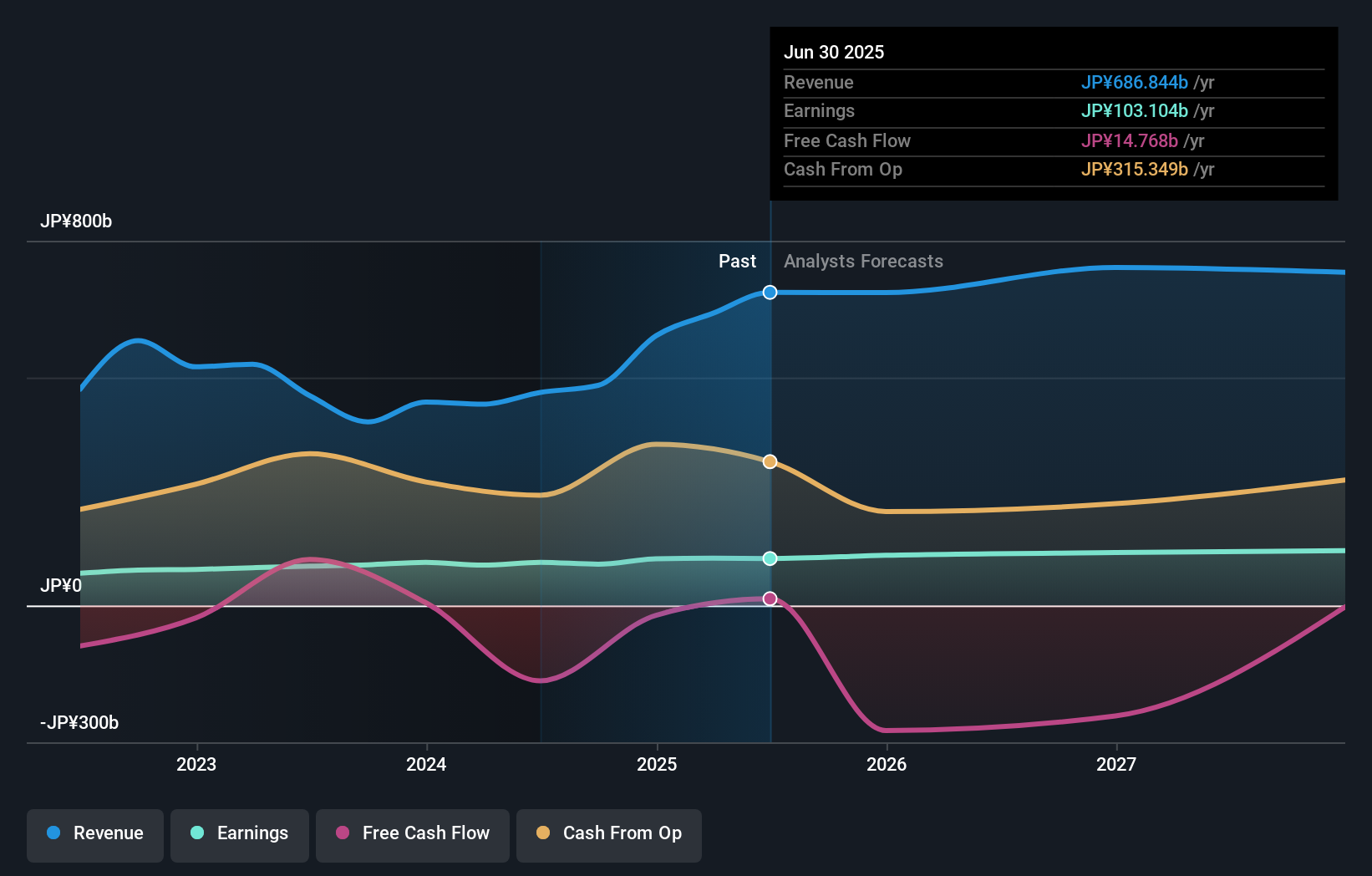

- Hulic Co., Ltd. recently updated its outlook for the fiscal year ending December 31, 2025, raising guidance for operating revenue to ¥710 billion, operating profit to ¥183 billion, and earnings per share to ¥147.43, along with announcing a higher annual dividend of ¥31.50 per share.

- This revision reflects the positive impact of property sales that did not meet the company’s holding criteria, signaling confidence in Hulic’s ability to drive profitability and return more capital to shareholders.

- With operating profit guidance lifted by ¥5 billion, we’ll explore what this means for Hulic’s investment narrative and future financial outlook.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

What Is Hulic's Investment Narrative?

To be a Hulic shareholder, you really need to believe in the company’s ability to consistently reposition its portfolio and boost returns, even as the broader real estate sector faces uneven growth. The recent upward revision to Hulic’s earnings and dividend guidance is a meaningful signal, reflecting the impact of disciplined property sales and renewed optimism for near-term results. This smoother path for profit growth, along with a stronger dividend, stands out as a short-term catalyst that might ease some of the pressure that came from lagging sector performance and moderate growth forecasts. However, it will also heighten focus on execution risks and the sustainability of free cash flows, especially since coverage for the higher dividend remains an open question. The risk profile has shifted somewhat: positive momentum could ease concerns about underperformance, but cash flow constraints deserve new scrutiny. On the other hand, risks to the dividend's sustainability remain highly relevant for investors to note.

Hulic's shares have been on the rise but are still potentially undervalued by 44%. Find out what it's worth.Exploring Other Perspectives

Explore another fair value estimate on Hulic - why the stock might be worth just ¥2911!

Build Your Own Hulic Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Hulic research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Hulic research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hulic's overall financial health at a glance.

Looking For Alternative Opportunities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hulic might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3003

Hulic

Engages in the holding, leasing, brokerage, and sale of real estate properties in Japan.

Good value average dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor