It's not a stretch to say that Daito Trust Construction Co.,Ltd.'s (TSE:1878) price-to-earnings (or "P/E") ratio of 15x right now seems quite "middle-of-the-road" compared to the market in Japan, where the median P/E ratio is around 15x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

With earnings growth that's superior to most other companies of late, Daito Trust ConstructionLtd has been doing relatively well. One possibility is that the P/E is moderate because investors think this strong earnings performance might be about to tail off. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

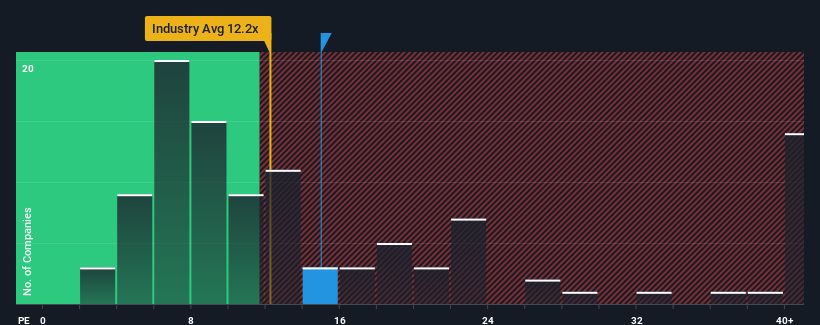

View our latest analysis for Daito Trust ConstructionLtd

Does Growth Match The P/E?

The only time you'd be comfortable seeing a P/E like Daito Trust ConstructionLtd's is when the company's growth is tracking the market closely.

If we review the last year of earnings growth, the company posted a terrific increase of 30%. However, this wasn't enough as the latest three year period has seen a very unpleasant 2.4% drop in EPS in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 10% per year during the coming three years according to the eight analysts following the company. That's shaping up to be similar to the 10% each year growth forecast for the broader market.

In light of this, it's understandable that Daito Trust ConstructionLtd's P/E sits in line with the majority of other companies. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Daito Trust ConstructionLtd maintains its moderate P/E off the back of its forecast growth being in line with the wider market, as expected. At this stage investors feel the potential for an improvement or deterioration in earnings isn't great enough to justify a high or low P/E ratio. It's hard to see the share price moving strongly in either direction in the near future under these circumstances.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Daito Trust ConstructionLtd with six simple checks.

If you're unsure about the strength of Daito Trust ConstructionLtd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:1878

Daito Trust ConstructionLtd

Designs, constructs, and rents apartments and condominiums in Japan.

Flawless balance sheet 6 star dividend payer.

Market Insights

Community Narratives