JCR Pharmaceuticals Co., Ltd. (TSE:4552) Shares May Have Slumped 28% But Getting In Cheap Is Still Unlikely

Unfortunately for some shareholders, the JCR Pharmaceuticals Co., Ltd. (TSE:4552) share price has dived 28% in the last thirty days, prolonging recent pain. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 60% loss during that time.

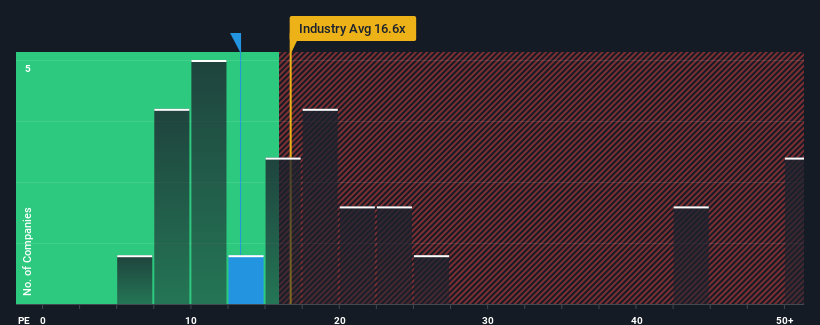

In spite of the heavy fall in price, you could still be forgiven for feeling indifferent about JCR Pharmaceuticals' P/E ratio of 13.3x, since the median price-to-earnings (or "P/E") ratio in Japan is also close to 14x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

With earnings growth that's superior to most other companies of late, JCR Pharmaceuticals has been doing relatively well. One possibility is that the P/E is moderate because investors think this strong earnings performance might be about to tail off. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

View our latest analysis for JCR Pharmaceuticals

Does Growth Match The P/E?

The only time you'd be comfortable seeing a P/E like JCR Pharmaceuticals' is when the company's growth is tracking the market closely.

If we review the last year of earnings growth, the company posted a terrific increase of 45%. However, this wasn't enough as the latest three year period has seen a very unpleasant 21% drop in EPS in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next three years should bring diminished returns, with earnings decreasing 13% each year as estimated by the seven analysts watching the company. Meanwhile, the broader market is forecast to expand by 9.1% per annum, which paints a poor picture.

With this information, we find it concerning that JCR Pharmaceuticals is trading at a fairly similar P/E to the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the negative growth outlook.

What We Can Learn From JCR Pharmaceuticals' P/E?

With its share price falling into a hole, the P/E for JCR Pharmaceuticals looks quite average now. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that JCR Pharmaceuticals currently trades on a higher than expected P/E for a company whose earnings are forecast to decline. When we see a poor outlook with earnings heading backwards, we suspect share price is at risk of declining, sending the moderate P/E lower. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

We don't want to rain on the parade too much, but we did also find 1 warning sign for JCR Pharmaceuticals that you need to be mindful of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4552

JCR Pharmaceuticals

Engages in the research, development, manufacture, import and export, and sale of pharmaceutical products, regenerative medicines, and drug substances in Japan.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Community Narratives