- Japan

- /

- Metals and Mining

- /

- TSE:5445

Highlighting Three Dividend Stocks For December 2024

Reviewed by Simply Wall St

As global markets navigate a landscape marked by central banks' rate adjustments and mixed economic signals, investors are increasingly turning their attention to the stability offered by dividend stocks. In this context of fluctuating indices and economic uncertainties, a good dividend stock is often characterized by its ability to provide consistent returns through reliable payouts, making it a potentially attractive option for those seeking income in unpredictable times.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Guaranty Trust Holding (NGSE:GTCO) | 7.12% | ★★★★★★ |

| Peoples Bancorp (NasdaqGS:PEBO) | 4.62% | ★★★★★★ |

| Yamato Kogyo (TSE:5444) | 4.00% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.35% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.41% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 3.96% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.36% | ★★★★★★ |

| E J Holdings (TSE:2153) | 3.83% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 5.67% | ★★★★★★ |

| Premier Financial (NasdaqGS:PFC) | 4.44% | ★★★★★★ |

Click here to see the full list of 1829 stocks from our Top Dividend Stocks screener.

Let's dive into some prime choices out of the screener.

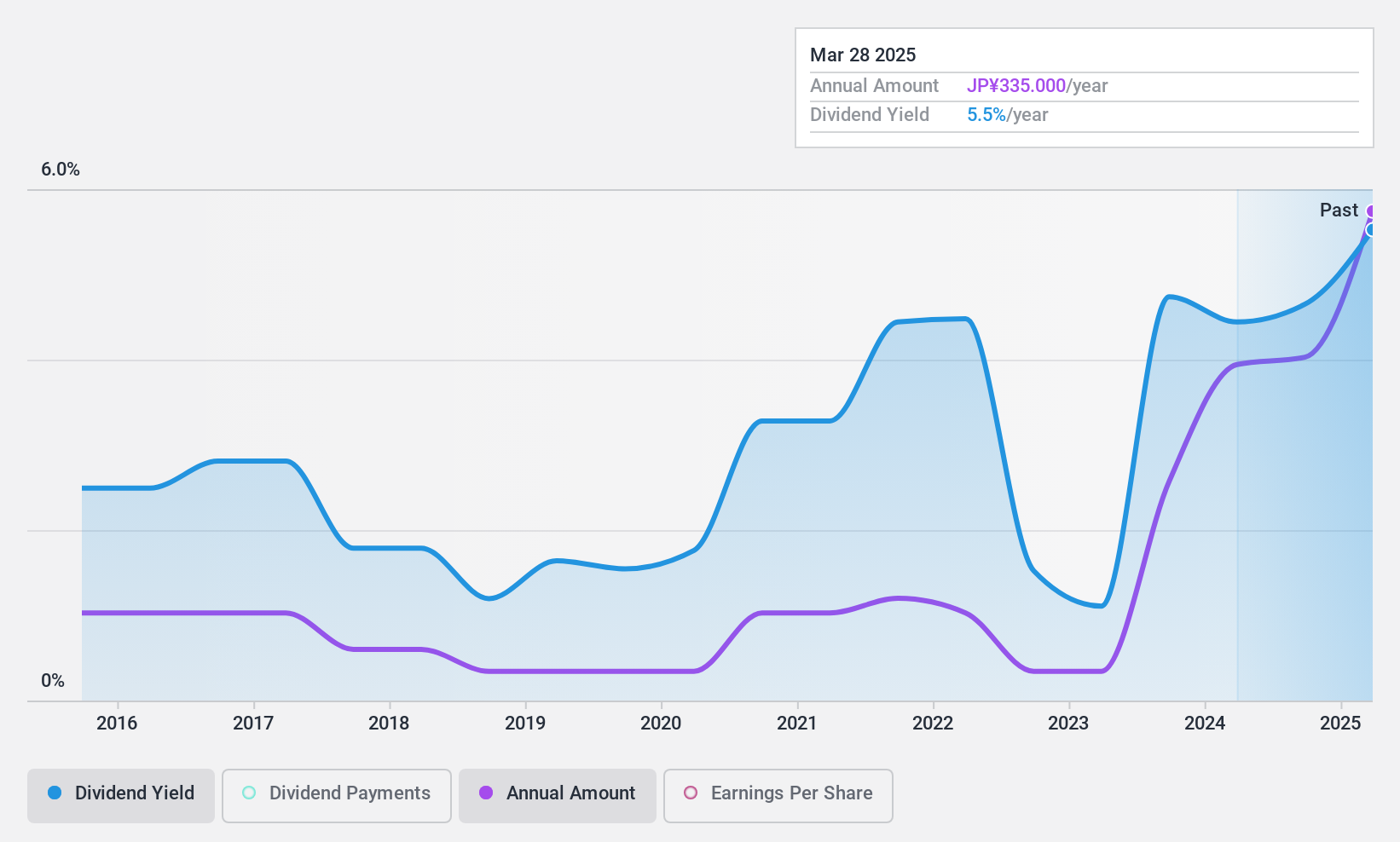

Ashimori Industry (TSE:3526)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Ashimori Industry Co., Ltd. manufactures and sells automotive safety systems in Japan and internationally, with a market cap of approximately ¥15.44 billion.

Operations: Ashimori Industry Co., Ltd. generates revenue primarily from its Automotive Safety Parts Business, which accounts for ¥51.79 billion, and its Functional Product Business, contributing ¥19.91 billion.

Dividend Yield: 3.9%

Ashimori Industry's dividends are well covered by both earnings and cash flows, with payout ratios of 27.3% and 25.7%, respectively. Despite a top-tier dividend yield of 3.9% in the Japanese market, the company's dividend history is unreliable due to volatility over the past decade. However, recent earnings growth of 72.4% suggests potential for future stability, though large one-off items have impacted financial results. The stock's P/E ratio of 7x indicates good value compared to the market average.

- Take a closer look at Ashimori Industry's potential here in our dividend report.

- Our valuation report unveils the possibility Ashimori Industry's shares may be trading at a premium.

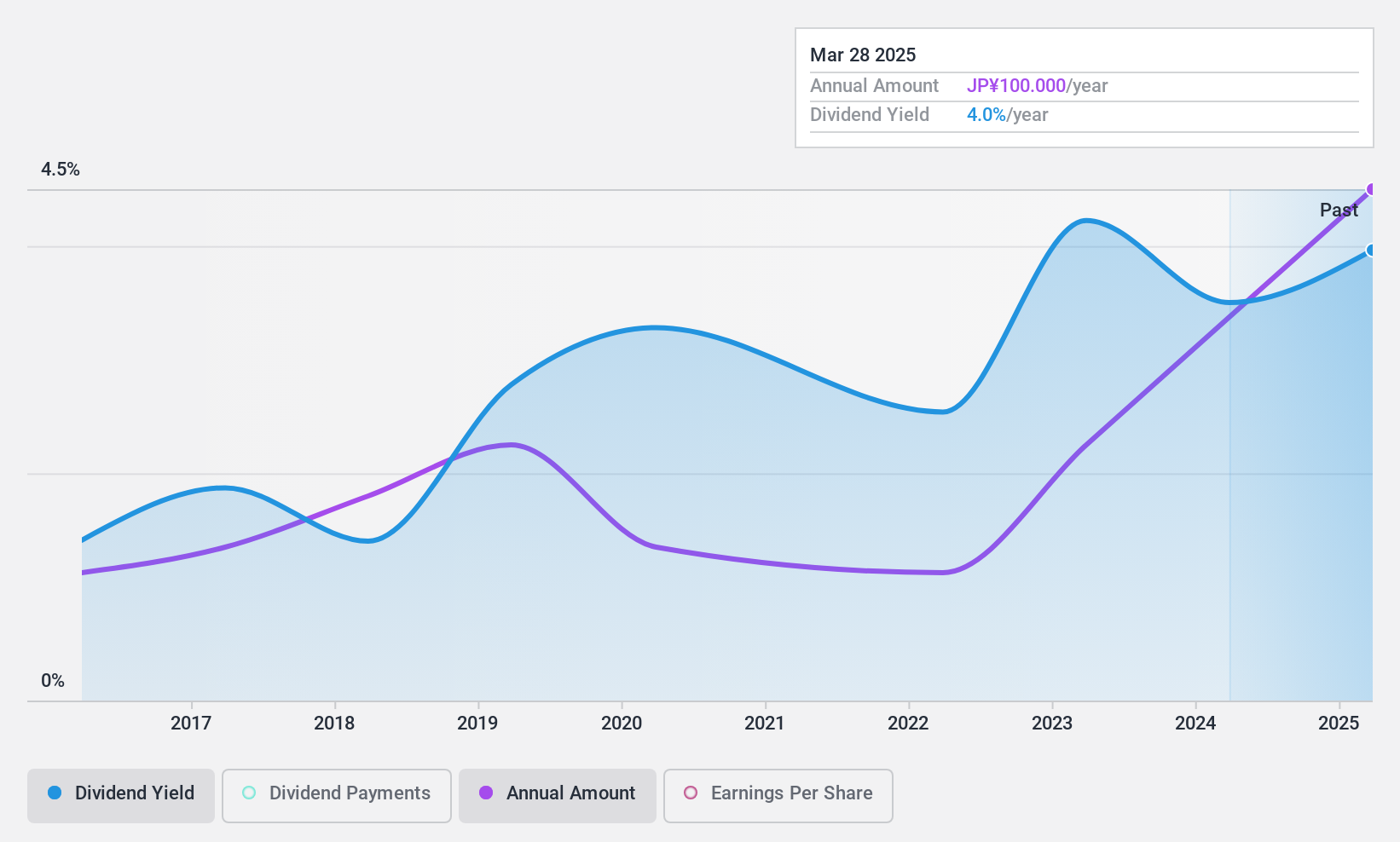

Tokyo Tekko (TSE:5445)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Tokyo Tekko Co., Ltd. manufactures and sells steel products for the construction industry in Japan, with a market cap of ¥56.75 billion.

Operations: Tokyo Tekko Co., Ltd.'s revenue primarily comes from its steel products tailored for the construction sector.

Dividend Yield: 5.2%

Tokyo Tekko's dividend payments are well covered by earnings and cash flows, with payout ratios of 20.2% and 32.8%, respectively. Despite a top-tier yield of 5.18% in Japan, the dividends have been volatile over the past decade, raising concerns about reliability. The recent share buyback program worth ¥500 million aims to enhance shareholder returns and improve capital efficiency amid business environment changes, potentially supporting future dividend stability despite past volatility.

- Unlock comprehensive insights into our analysis of Tokyo Tekko stock in this dividend report.

- Our comprehensive valuation report raises the possibility that Tokyo Tekko is priced lower than what may be justified by its financials.

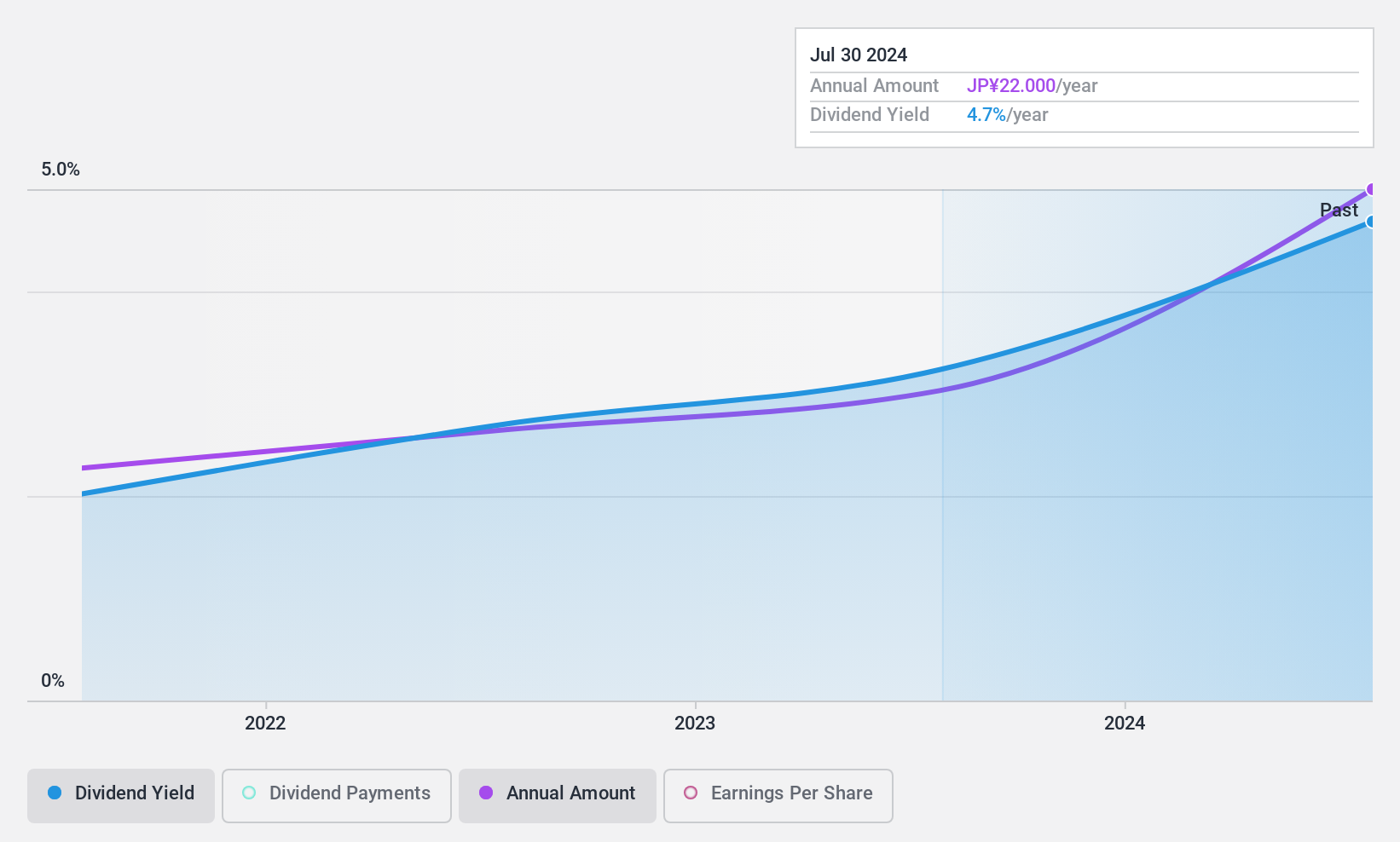

i-mobileLtd (TSE:6535)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: i-mobile Co., Ltd. operates in the Internet advertising sector in Japan and has a market cap of ¥31.81 billion.

Operations: i-mobile Co., Ltd. generates its revenue primarily from the Internet advertising sector in Japan.

Dividend Yield: 4.7%

i-mobile Ltd. has increased its dividend payments over the past four years, offering a top-tier yield of 4.71% in Japan. While dividends are well covered by earnings and cash flows, with payout ratios of 84.4% and 45%, respectively, profit margins have declined from last year. The company trades at a significant discount to its estimated fair value, but its short dividend history may raise concerns about long-term reliability despite stable payments so far.

- Navigate through the intricacies of i-mobileLtd with our comprehensive dividend report here.

- Upon reviewing our latest valuation report, i-mobileLtd's share price might be too pessimistic.

Make It Happen

- Unlock our comprehensive list of 1829 Top Dividend Stocks by clicking here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tokyo Tekko might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5445

Tokyo Tekko

Engages in the manufacture and sale of steel products for the construction industry in Japan.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Community Narratives