Dentsu Group Inc.'s (TSE:4324) investors are due to receive a payment of ¥69.75 per share on 12th of September. This means the annual payment is 3.3% of the current stock price, which is above the average for the industry.

See our latest analysis for Dentsu Group

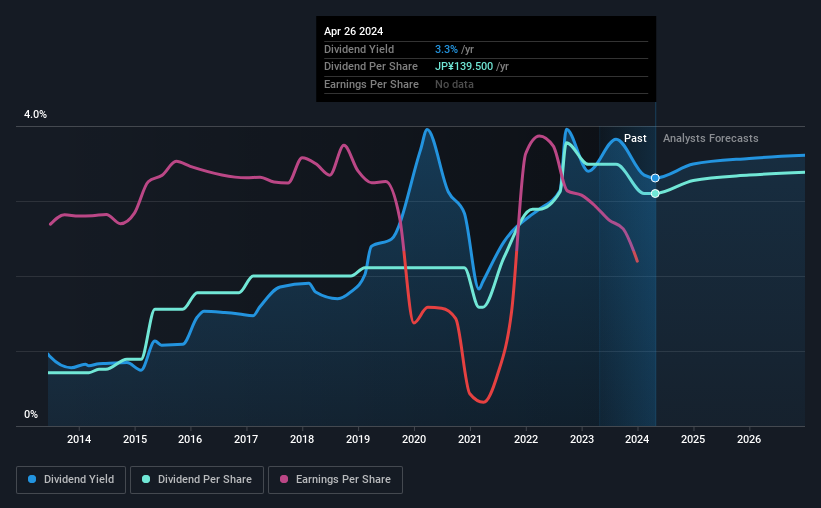

Dentsu Group's Distributions May Be Difficult To Sustain

A big dividend yield for a few years doesn't mean much if it can't be sustained. Dentsu Group is not generating a profit, and despite this is paying out most of its free cash flow as a dividend. Paying a dividend while unprofitable is generally considered an aggressive policy, and with limited funds retained for reinvestment, growth may be slow.

Analysts expect the EPS to grow by 32.3% over the next 12 months. The company seems to be going down the right path, but it will take a little bit longer than a year to cross over into profitability. Unfortunately, for the dividend to continue at current levels the company definitely needs to get there sooner rather than later.

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. Since 2014, the annual payment back then was ¥32.00, compared to the most recent full-year payment of ¥139.50. This means that it has been growing its distributions at 16% per annum over that time. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

The Company Could Face Some Challenges Growing The Dividend

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Dentsu Group has impressed us by growing EPS at 11% per year over the past five years. It's not great that the company is not turning a profit, but the decent growth in recent years is certainly a positive sign. As long as the company becomes profitable soon, it is on a trajectory that could see it being a solid dividend payer.

The Dividend Could Prove To Be Unreliable

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. Strong earnings growth means Dentsu Group has the potential to be a good dividend stock in the future, despite the current payments being at elevated levels. We don't think Dentsu Group is a great stock to add to your portfolio if income is your focus.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For instance, we've picked out 1 warning sign for Dentsu Group that investors should take into consideration. Is Dentsu Group not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4324

Dentsu Group

Operates in the advertising business in Japan, the Americas, Europe, the Middle East and Africa, and the Asia Pacific.

Undervalued with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives