- Japan

- /

- Entertainment

- /

- TSE:3758

We Wouldn't Be Too Quick To Buy Aeria Inc. (TYO:3758) Before It Goes Ex-Dividend

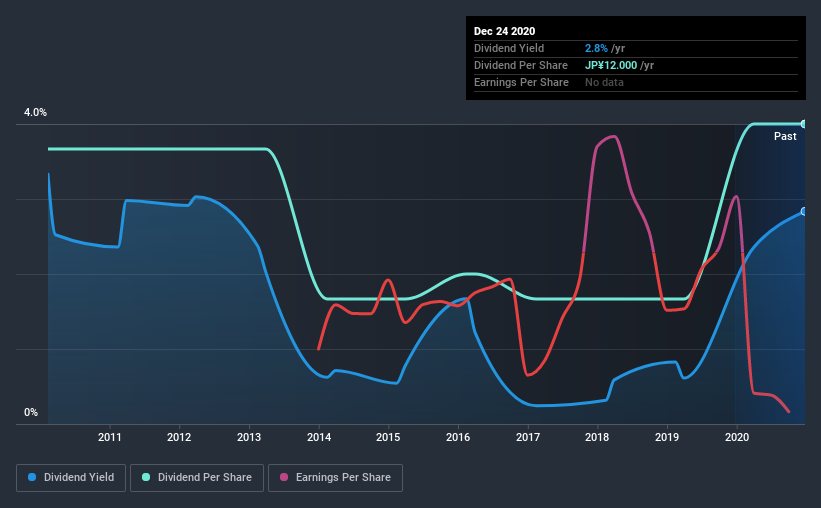

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Aeria Inc. (TYO:3758) is about to trade ex-dividend in the next 4 days. If you purchase the stock on or after the 29th of December, you won't be eligible to receive this dividend, when it is paid on the 31st of March.

Aeria's upcoming dividend is JP¥5.00 a share, following on from the last 12 months, when the company distributed a total of JP¥12.00 per share to shareholders. Looking at the last 12 months of distributions, Aeria has a trailing yield of approximately 2.8% on its current stock price of ¥423. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to investigate whether Aeria can afford its dividend, and if the dividend could grow.

Check out our latest analysis for Aeria

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Aeria reported a loss after tax last year, which means it's paying a dividend despite being unprofitable. While this might be a one-off event, this is unlikely to be sustainable in the long term. Considering the lack of profitability, we also need to check if the company generated enough cash flow to cover the dividend payment. If Aeria didn't generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. It paid out 6.5% of its free cash flow as dividends last year, which is conservatively low.

Click here to see how much of its profit Aeria paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If earnings fall far enough, the company could be forced to cut its dividend. Aeria reported a loss last year, and the general trend suggests its earnings have also been declining in recent years, making us wonder if the dividend is at risk.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. In the last 10 years, Aeria has lifted its dividend by approximately 0.9% a year on average.

Get our latest analysis on Aeria's balance sheet health here.

To Sum It Up

From a dividend perspective, should investors buy or avoid Aeria? First, it's not great to see the company paying a dividend despite being loss-making over the last year. On the plus side, the dividend was covered by free cash flow." It's not the most attractive proposition from a dividend perspective, and we'd probably give this one a miss for now.

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with Aeria. Every company has risks, and we've spotted 4 warning signs for Aeria (of which 1 doesn't sit too well with us!) you should know about.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade Aeria, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade Aeria, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSE:3758

Mediocre balance sheet and slightly overvalued.

Market Insights

Community Narratives