Advertisement

- Japan

- /

- Metals and Mining

- /

- TSE:5713

Why Sumitomo Metal Mining (TSE:5713) Is Up 8.7% After Goldman Sachs Upgrades and Raises Earnings Outlook

Simply Wall St

Reviewed by Sasha Jovanovic

- Goldman Sachs recently upgraded Sumitomo Metal Mining from Sell to Neutral and increased its earnings outlook, referencing a revised valuation base year during their analyst update.

- This shift by a major financial institution highlights evolving sentiment toward the company's projected financial performance and prospects.

- We'll examine how Goldman Sachs' improved earnings estimates and outlook could influence Sumitomo Metal Mining's investment story.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

What Is Sumitomo Metal Mining's Investment Narrative?

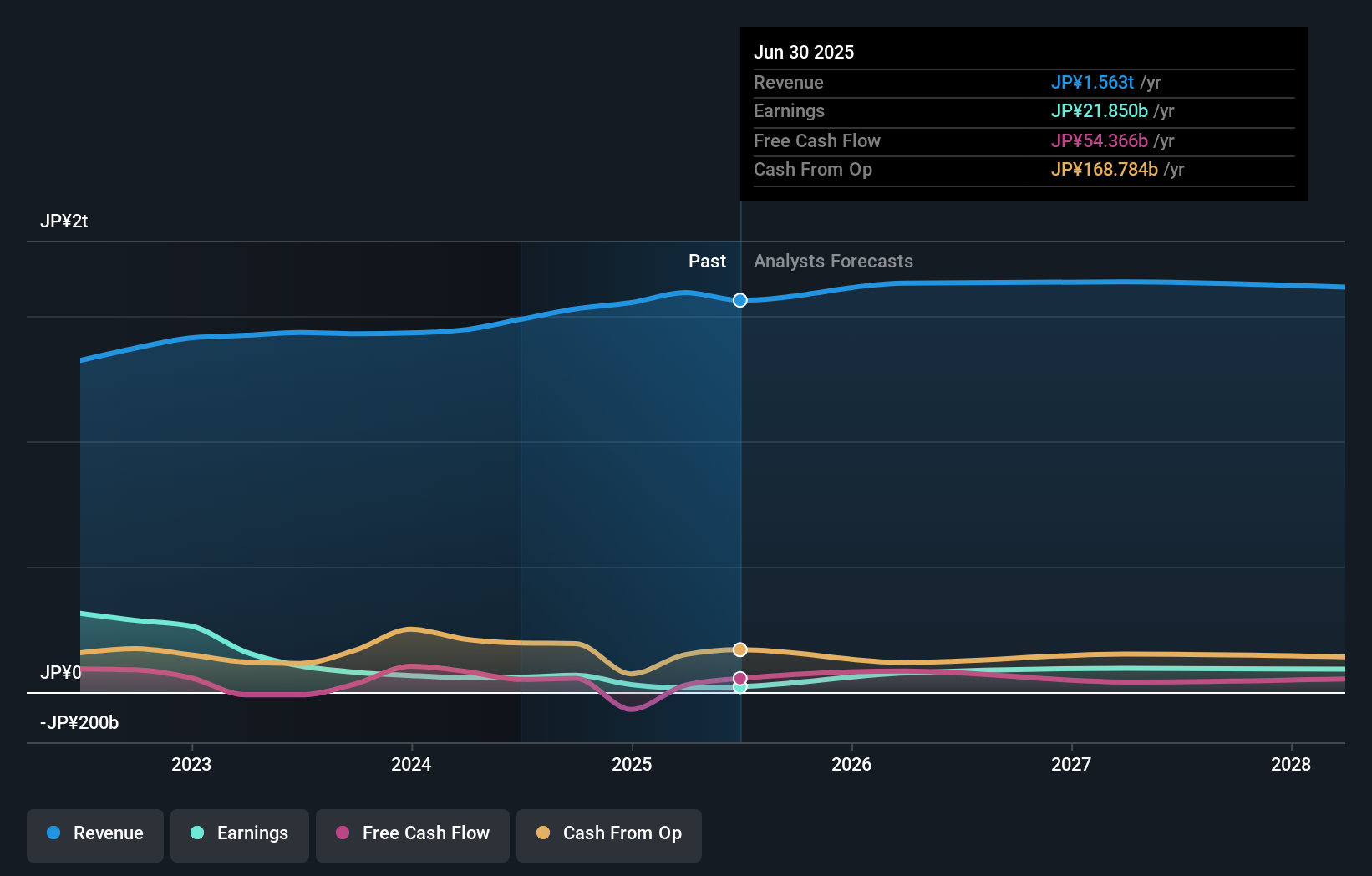

To be a shareholder in Sumitomo Metal Mining, you need confidence in the company's ability to capitalize on demand for metals like copper, nickel, and gold, while skillfully navigating commodity price swings, operational execution, and capital-intensive project risks. The recent Goldman Sachs upgrade from Sell to Neutral, along with a price target increase, does mark a shift in short-term sentiment, suggesting greater confidence in the company’s near-term profit outlook, likely influenced by improved earnings forecasts and more robust project valuations. However, this upgrade alone does not fundamentally change the key catalysts or risks on the table. The biggest short-term catalysts remain the company's performance in ramping up new projects and strategic alliances, such as its stake in the Winu copper-gold project and battery material initiatives. Meanwhile, profit margins and earnings coverage for dividends remain points of concern, as does a price-to-earnings ratio that is still well above industry averages. While analyst sentiment may provide some near-term momentum, the underlying challenges around profitability and effective management remain significant risks, and the overall risk/reward calculation has not shifted dramatically in light of the recent upgrade.

By contrast, the volatility in profit margins is still something investors need to keep on their radar.

Exploring Other Perspectives

Explore another fair value estimate on Sumitomo Metal Mining - why the stock might be worth just ¥7022!

Build Your Own Sumitomo Metal Mining Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Sumitomo Metal Mining research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Sumitomo Metal Mining research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sumitomo Metal Mining's overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5713

Sumitomo Metal Mining

Engages in mining, smelting, and refining non-ferrous metals in Japan and internationally.

Adequate balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative