- Japan

- /

- Metals and Mining

- /

- TSE:5610

Daiwa Heavy Industry Co., Ltd.'s (TSE:5610) Shares Climb 47% But Its Business Is Yet to Catch Up

The Daiwa Heavy Industry Co., Ltd. (TSE:5610) share price has done very well over the last month, posting an excellent gain of 47%. The last 30 days bring the annual gain to a very sharp 72%.

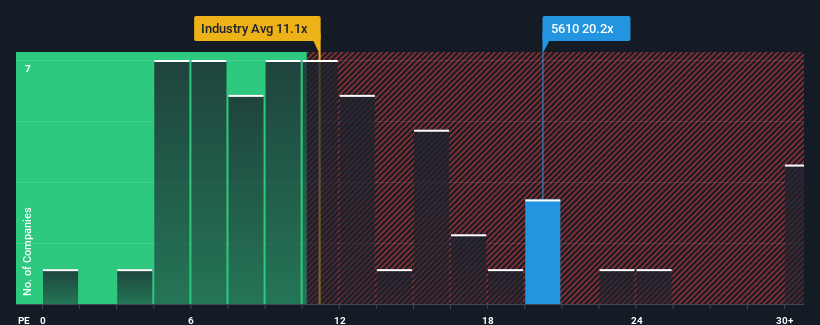

After such a large jump in price, Daiwa Heavy Industry may be sending bearish signals at the moment with its price-to-earnings (or "P/E") ratio of 20.2x, since almost half of all companies in Japan have P/E ratios under 14x and even P/E's lower than 9x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

With earnings growth that's exceedingly strong of late, Daiwa Heavy Industry has been doing very well. It seems that many are expecting the strong earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

See our latest analysis for Daiwa Heavy Industry

How Is Daiwa Heavy Industry's Growth Trending?

There's an inherent assumption that a company should outperform the market for P/E ratios like Daiwa Heavy Industry's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 38% gain to the company's bottom line. Still, EPS has barely risen at all from three years ago in total, which is not ideal. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 9.7% shows it's noticeably less attractive on an annualised basis.

In light of this, it's alarming that Daiwa Heavy Industry's P/E sits above the majority of other companies. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with recent growth rates.

The Bottom Line On Daiwa Heavy Industry's P/E

Daiwa Heavy Industry shares have received a push in the right direction, but its P/E is elevated too. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Daiwa Heavy Industry currently trades on a much higher than expected P/E since its recent three-year growth is lower than the wider market forecast. When we see weak earnings with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Before you settle on your opinion, we've discovered 2 warning signs for Daiwa Heavy Industry (1 can't be ignored!) that you should be aware of.

Of course, you might also be able to find a better stock than Daiwa Heavy Industry. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5610

Daiwa Heavy Industry

Manufactures and sells various products for industrial machinery and housing equipment in Japan.

Mediocre balance sheet low.