- Japan

- /

- Metals and Mining

- /

- TSE:5481

Earnings Tell The Story For Sanyo Special Steel Co., Ltd. (TSE:5481) As Its Stock Soars 30%

Despite an already strong run, Sanyo Special Steel Co., Ltd. (TSE:5481) shares have been powering on, with a gain of 30% in the last thirty days. Taking a wider view, although not as strong as the last month, the full year gain of 13% is also fairly reasonable.

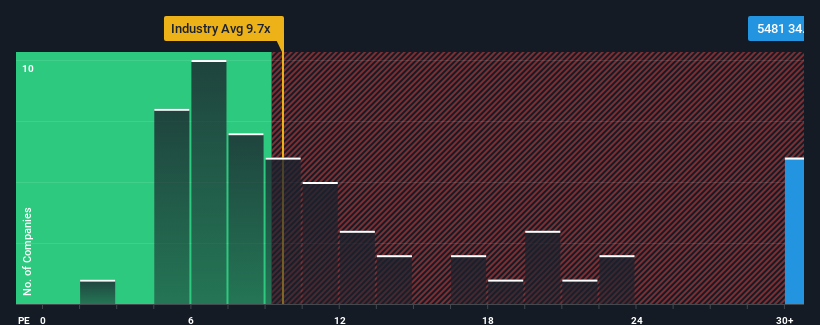

After such a large jump in price, Sanyo Special Steel's price-to-earnings (or "P/E") ratio of 34.2x might make it look like a strong sell right now compared to the market in Japan, where around half of the companies have P/E ratios below 13x and even P/E's below 9x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Sanyo Special Steel could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Check out our latest analysis for Sanyo Special Steel

Is There Enough Growth For Sanyo Special Steel?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Sanyo Special Steel's to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 68%. This means it has also seen a slide in earnings over the longer-term as EPS is down 56% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 50% per annum during the coming three years according to the lone analyst following the company. That's shaping up to be materially higher than the 9.9% per annum growth forecast for the broader market.

In light of this, it's understandable that Sanyo Special Steel's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Sanyo Special Steel's P/E?

The strong share price surge has got Sanyo Special Steel's P/E rushing to great heights as well. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Sanyo Special Steel's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Before you take the next step, you should know about the 3 warning signs for Sanyo Special Steel (1 is potentially serious!) that we have uncovered.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:5481

Sanyo Special Steel

Manufactures and sells special steel products in Japan and internationally.

Flawless balance sheet average dividend payer.

Market Insights

Community Narratives