Three Japanese Stocks That Might Be Trading Below Their Intrinsic Value

Reviewed by Simply Wall St

Japan’s stock markets have shown mixed performance recently, with the Nikkei 225 Index gaining 0.5% while the broader TOPIX Index declined by 1.0%. Amid these fluctuations and a hawkish outlook from the Bank of Japan, investors may find opportunities in stocks that are trading below their intrinsic value. Identifying undervalued stocks often involves looking for companies with solid fundamentals that are currently overlooked or underappreciated by the market. In this article, we will explore three Japanese stocks that might be trading below their intrinsic value and could offer potential for long-term growth.

Top 10 Undervalued Stocks Based On Cash Flows In Japan

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Hagiwara Electric Holdings (TSE:7467) | ¥3470.00 | ¥6770.20 | 48.7% |

| Kotobuki Spirits (TSE:2222) | ¥1719.00 | ¥3434.73 | 50% |

| Plus Alpha ConsultingLtd (TSE:4071) | ¥2087.00 | ¥4159.22 | 49.8% |

| Stella Chemifa (TSE:4109) | ¥4170.00 | ¥8128.08 | 48.7% |

| I-PEX (TSE:6640) | ¥1496.00 | ¥2889.72 | 48.2% |

| Ohara (TSE:5218) | ¥1298.00 | ¥2594.00 | 50% |

| West Holdings (TSE:1407) | ¥2613.00 | ¥5098.07 | 48.7% |

| Infomart (TSE:2492) | ¥317.00 | ¥616.94 | 48.6% |

| SHIFT (TSE:3697) | ¥11825.00 | ¥23318.09 | 49.3% |

| Visional (TSE:4194) | ¥8640.00 | ¥17014.04 | 49.2% |

Let's uncover some gems from our specialized screener.

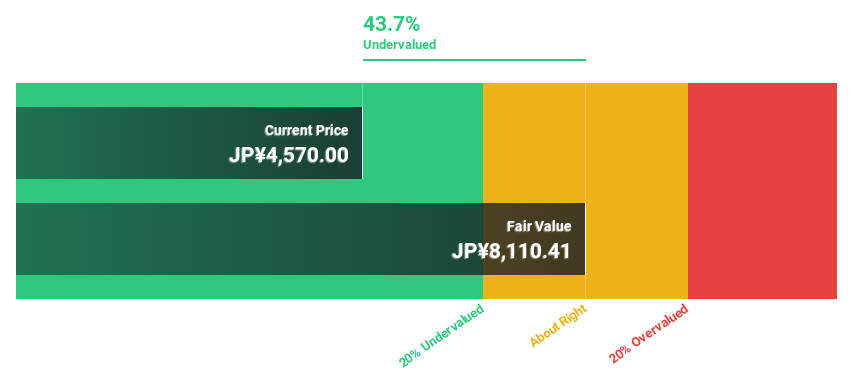

Stella Chemifa (TSE:4109)

Overview: Stella Chemifa Corporation manufactures and sells inorganic fluorine compounds both in Japan and internationally, with a market cap of ¥50.22 billion.

Operations: The company's revenue segments include High-Purity Chemical at ¥27.44 billion and Transportation at ¥7.60 billion.

Estimated Discount To Fair Value: 48.7%

Stella Chemifa, trading at ¥4170, is significantly undervalued based on discounted cash flow analysis with an estimated fair value of ¥8128.08. Despite a dividend cut to JPY 85.00 per share for the fiscal year ending March 31, 2025, its earnings are projected to grow by 23.49% annually over the next three years, outpacing the Japanese market's growth rate. However, its current dividend yield of 4.08% is not well covered by earnings or free cash flows.

- Upon reviewing our latest growth report, Stella Chemifa's projected financial performance appears quite optimistic.

- Click to explore a detailed breakdown of our findings in Stella Chemifa's balance sheet health report.

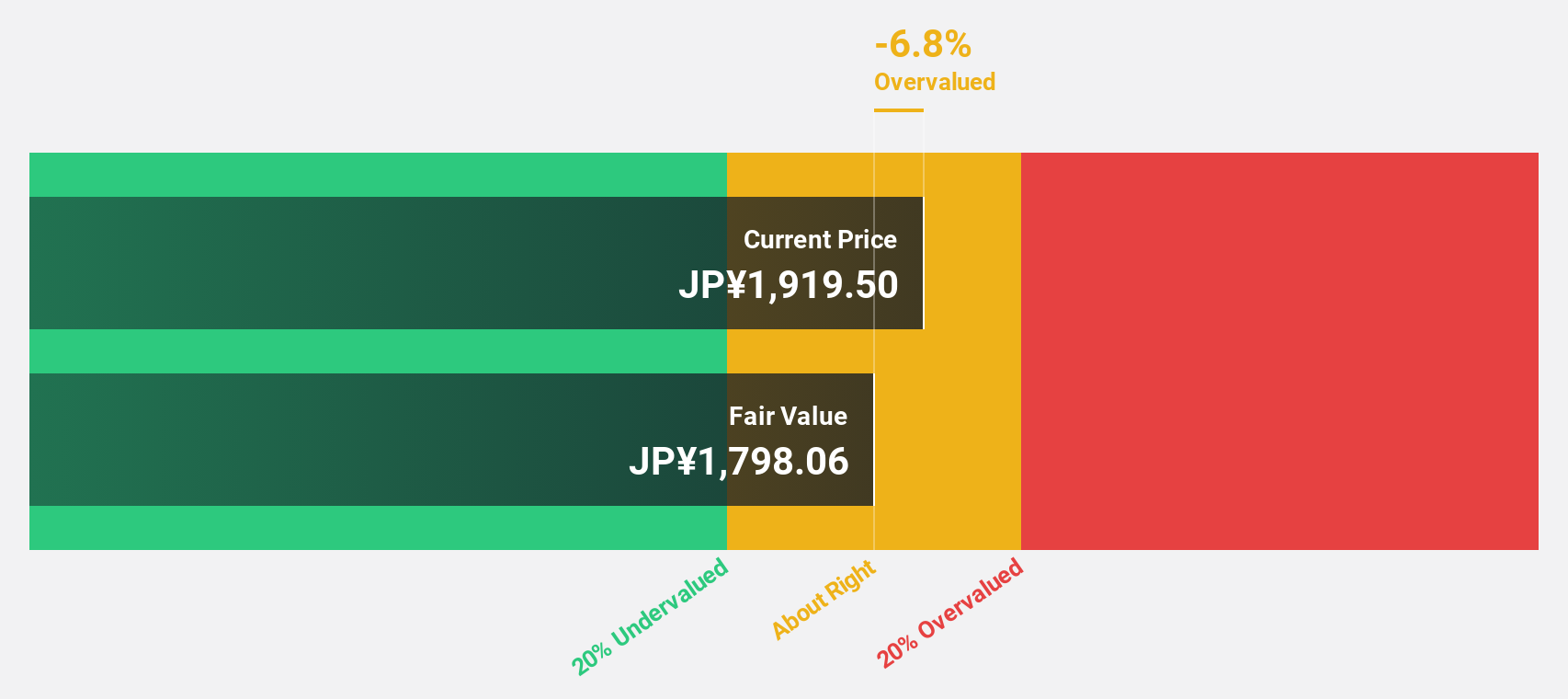

PARK24 (TSE:4666)

Overview: PARK24 Co., Ltd. operates and manages parking facilities in Japan and internationally, with a market cap of ¥303.49 billion.

Operations: The company's revenue segments include parking facility operations in Japan and internationally.

Estimated Discount To Fair Value: 17.6%

PARK24, trading at ¥1779, is undervalued based on discounted cash flow analysis with an estimated fair value of ¥2158.73. Its earnings are forecast to grow 12.89% annually, outpacing the Japanese market's 8.7%. Recent strategic alliances include a pilot rideshare service with Uber Japan and Royal Limousine Co., Ltd., potentially increasing vehicle usage and revenue streams despite the company's high debt levels.

- Our earnings growth report unveils the potential for significant increases in PARK24's future results.

- Click here and access our complete balance sheet health report to understand the dynamics of PARK24.

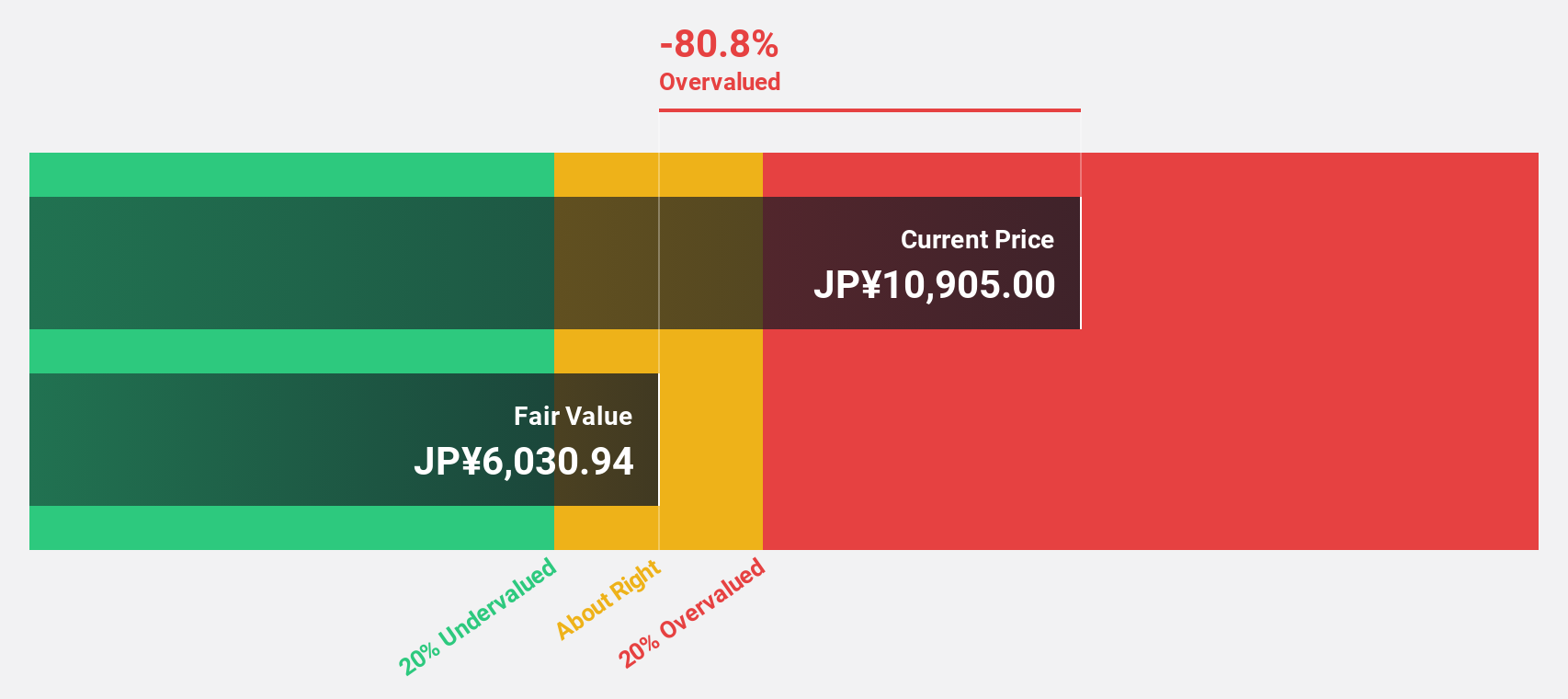

Kawasaki Heavy Industries (TSE:7012)

Overview: Kawasaki Heavy Industries, Ltd. operates in aerospace systems, energy solutions and marine engineering, precision machinery and robotics, rolling stock, and motorcycle and engine businesses globally with a market cap of ¥823.77 billion.

Operations: The company's revenue segments include Aerospace Business (¥435.40 billion), Power Sports & Engine (¥594.38 billion), Energy Solutions & Marine (¥388.09 billion), Precision Machinery / Robot (¥249.35 billion), and Vehicle (¥196.26 billion).

Estimated Discount To Fair Value: 27.5%

Kawasaki Heavy Industries is trading at ¥4918, significantly below its estimated fair value of ¥6779.2, indicating it may be undervalued based on discounted cash flows. Despite lower profit margins this year (1.7% vs 3.2%), earnings are forecast to grow 22.25% annually, outpacing the Japanese market's 8.6%. However, debt coverage by operating cash flow remains a concern, and the stock has experienced high volatility recently despite its addition to the S&P Japan Mid Cap 100 index in June 2024.

- The growth report we've compiled suggests that Kawasaki Heavy Industries' future prospects could be on the up.

- Delve into the full analysis health report here for a deeper understanding of Kawasaki Heavy Industries.

Summing It All Up

- Embark on your investment journey to our 80 Undervalued Japanese Stocks Based On Cash Flows selection here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kawasaki Heavy Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7012

Kawasaki Heavy Industries

Engages in aerospace systems, energy solution and marine engineering, precision machinery and robot, rolling stock, and motorcycle and engine businesses in Japan and internationally.

Solid track record and good value.