Advertisement

- Japan

- /

- Personal Products

- /

- TSE:4911

Shiseido (TSE:4911): Exploring Valuation After Prolonged Share Price Weakness

Kshitija Bhandaru

Reviewed by Simply Wall St

For investors with an eye on Shiseido Company (TSE:4911), the company’s latest stock performance might spark a fresh round of debate. While there is no particular headline event in the spotlight today, the recent moves in the share price could be interpreted as a possible inflection point or simply the ongoing result of global consumer sector dynamics. With Shiseido’s long-standing presence and recent financial swings, it is understandable if you are wondering whether the market is signaling a potential shift in sentiment.

Looking back over the year, Shiseido’s shares have faced a downtrend, falling over 23% in the past 12 months and sliding further year-to-date. Shorter-term momentum has remained subdued, with only minor movement in the past month. This trend comes against a backdrop of modest annual revenue growth, but also a notable turnaround in net income even as the broader consumer sector has dealt with shifting consumer demand and cost pressures.

Given the degree of decline and the current muted sentiment, is Shiseido positioned as an undervalued opportunity, or is the market already pricing in the company’s future growth prospects?

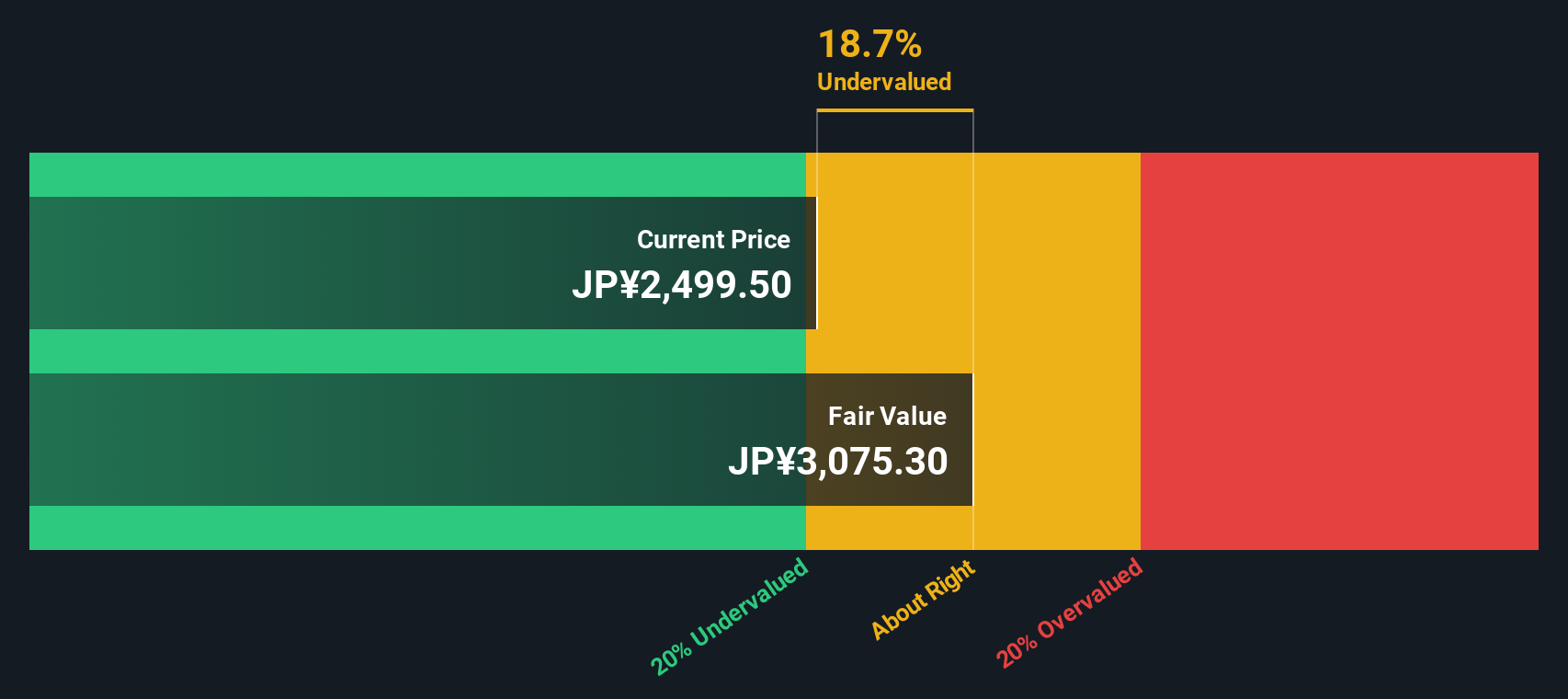

Most Popular Narrative: 7.6% Undervalued

According to the most widely followed narrative, Shiseido’s shares are currently undervalued relative to their calculated fair value, based on consensus analyst forecasts and a discount rate of 6.5%. The narrative emphasizes the company’s prospects for earnings recovery and margin expansion, factoring in structural reforms and long-term growth projections.

Accelerated structural reforms, including significant fixed cost reductions, workforce optimization (notably in the Americas), and enhanced global cost management are expected to drive sustained margin expansion and improved return on invested capital. These factors support higher net margins and earnings. Shiseido's focus on scaling its prestige and luxury skincare brands such as Clé de Peau Beauté, NARS, and ULTIMUNE, aligns with rising demand for premium beauty among an expanding Asian middle class and global aging populations. This demand is expected to raise average selling prices (ASPs) and drive medium to long-term revenue growth.

Curious what’s fueling this valuation upside? This story hinges on pivotal earnings projections and a big leap in future profit margins. But there’s more going on beneath the surface, from bullish growth bets to bold assumptions about a sector in flux. Uncover which financial forecasts have driven analysts to call Shiseido undervalued in this narrative.

Result: Fair Value of ¥2,604 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent weak sales in key regions, along with heavy reliance on ongoing restructuring, could challenge the optimistic outlook for Shiseido’s margin recovery and growth.

Find out about the key risks to this Shiseido Company narrative.Another View: What Does Our DCF Model Say?

Taking a different approach, our DCF model also suggests Shiseido is undervalued at current prices. This method uses cash flows and longer-range assumptions. However, does it really capture the risks or optimism in the forecasts?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Shiseido Company Narrative

If you see the numbers differently or want to dig into the data first-hand, you can craft your own view in just a few minutes. Do it your way.

A great starting point for your Shiseido Company research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Winning Investment Ideas?

Smart investors always keep an eye out for the next big opportunity. Don’t let great stocks pass you by. Use these advanced screens to spark fresh investing momentum today:

- Unearth potential value by sizing up unique opportunities in the market with undervalued stocks based on cash flows right at your fingertips.

- Fuel your watchlist with the innovators transforming healthcare. Start by scanning a universe of breakthroughs through healthcare AI stocks.

- Supercharge your income portfolio with stocks that offer strong, consistent yields thanks to dividend stocks with yields > 3% for reliable returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About TSE:4911

Shiseido Company

Engages in the production and sale of cosmetics in Japan and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor