- Japan

- /

- Food and Staples Retail

- /

- TSE:8198

Undiscovered Gems Promising Stocks To Watch In December 2024

Reviewed by Simply Wall St

As global markets navigate a period of uncertainty marked by cautious Federal Reserve commentary and political tensions, small-cap stocks have been particularly impacted, with indices like the S&P 600 experiencing notable declines. Amid these challenges, discerning investors are on the lookout for undiscovered gems—stocks that demonstrate resilience and potential for growth despite broader market volatility.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Central Forest Group | NA | 6.85% | 15.11% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Standard Bank | 0.13% | 27.78% | 30.36% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| PBA Holdings Bhd | 1.86% | 7.41% | 40.17% | ★★★★★☆ |

| First National Bank of Botswana | 24.77% | 10.64% | 15.30% | ★★★★★☆ |

| Pure Cycle | 5.31% | -4.44% | -5.74% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| DIRTT Environmental Solutions | 58.73% | -5.34% | -5.43% | ★★★★☆☆ |

| Krom Bank Indonesia | NA | 40.04% | 35.44% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

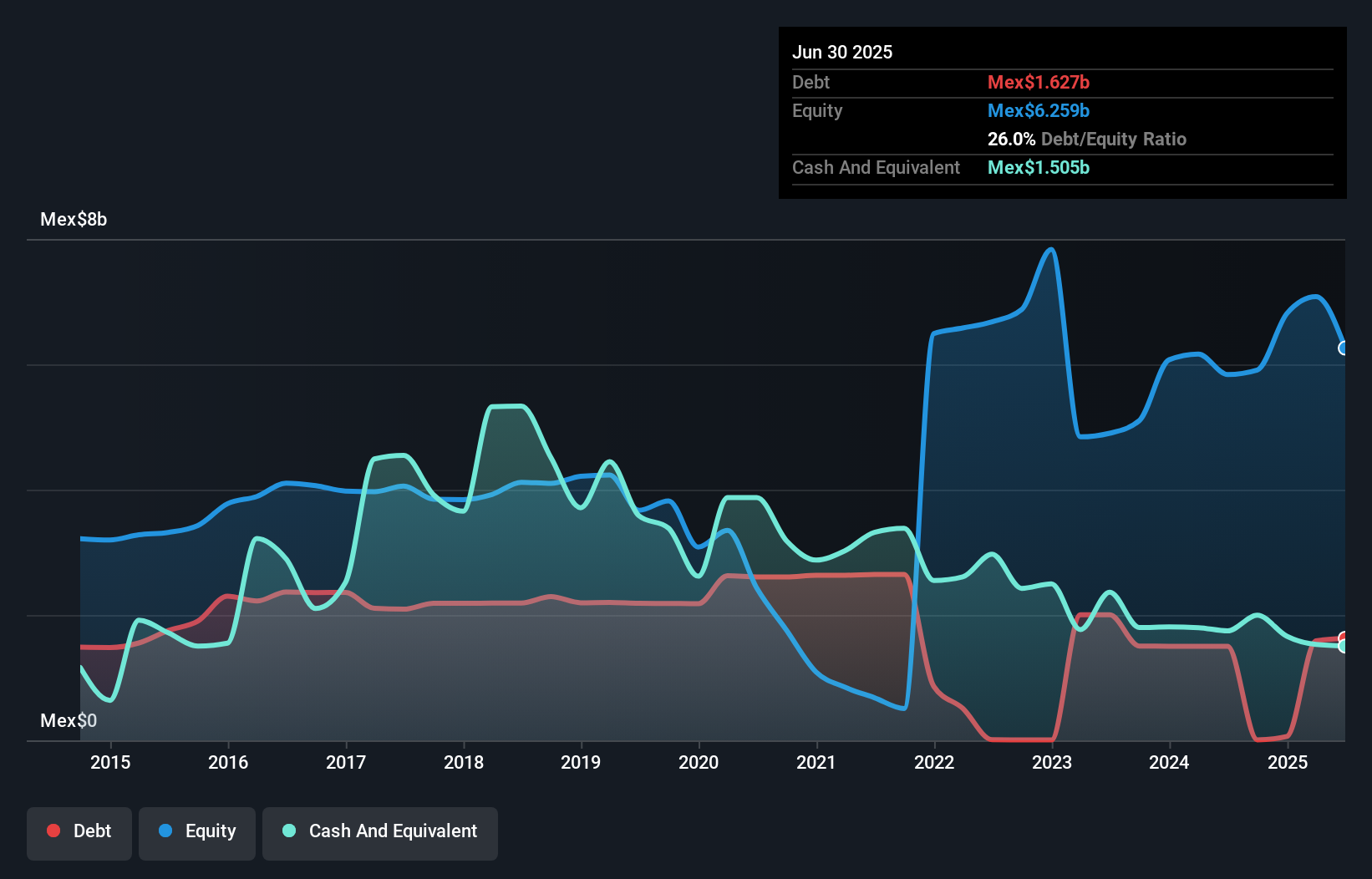

Corporación Interamericana de Entretenimiento. de (BMV:CIE B)

Simply Wall St Value Rating: ★★★★★☆

Overview: Corporación Interamericana de Entretenimiento, S.A.B. operates as a leading entertainment company in Latin America, with a market cap of approximately MX$15.38 billion.

Operations: CIE generates revenue primarily from special events, totaling MX$4.88 billion, complemented by other businesses contributing MX$312.22 million.

Corporación Interamericana de Entretenimiento, known for its niche in the entertainment sector, reported third-quarter sales of MX$383 million, slightly up from last year. Despite a dip in quarterly net income to MX$117 million, nine-month figures show net income soaring to MX$528 million. The company's earnings growth of 21% outpaces the industry average and reflects high-quality past earnings. With a debt-to-equity ratio dropping from 57% to just 0.1% over five years and cash exceeding total debt, financial stability seems solid. A price-to-earnings ratio of 10.4x suggests good value compared to the broader market's 11.7x benchmark.

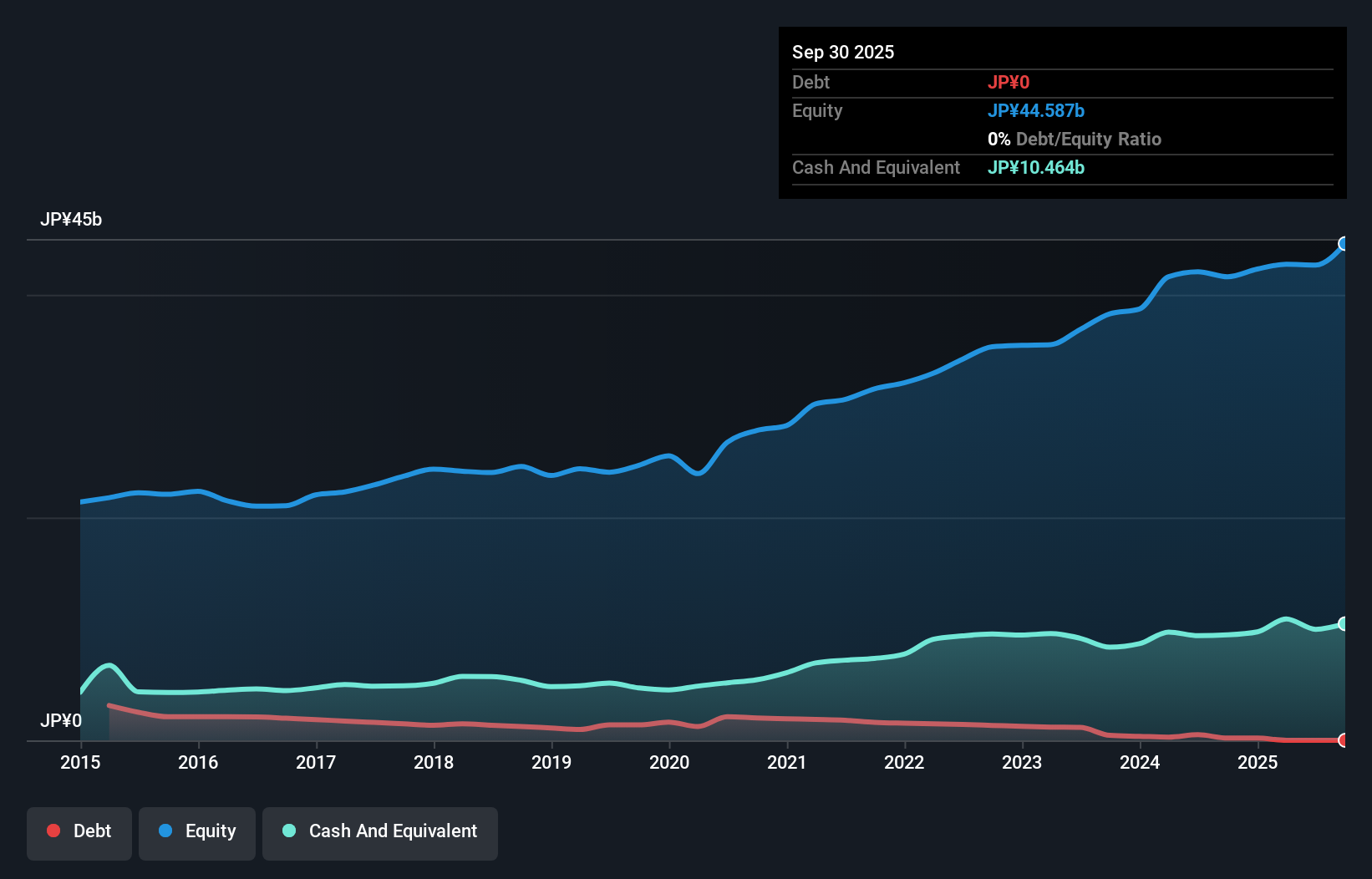

Shofu (TSE:7979)

Simply Wall St Value Rating: ★★★★★★

Overview: Shofu Inc. is a global manufacturer and seller of dental materials and equipment with a market cap of ¥77.81 billion.

Operations: The company generates revenue primarily from the sale of dental materials and equipment. Its financial performance is highlighted by a net profit margin of 6.5%, indicating efficient cost management relative to its revenue streams.

Shofu, a notable player in the dental materials industry, has shown impressive financial resilience. Over the past year, earnings surged by 74%, outpacing the broader Medical Equipment sector's 6% growth. The company is set to deliver JPY 38.39 billion in net sales and JPY 5.29 billion in operating income for fiscal year ending March 2025. Recently, Shofu increased its dividend from JPY 20 to JPY 36 per share for Q2 of this fiscal year, reflecting strong cash flow management and commitment to shareholder returns. Despite a volatile share price recently, Shofu's robust earnings growth positions it well within its niche market segment.

- Delve into the full analysis health report here for a deeper understanding of Shofu.

Gain insights into Shofu's historical performance by reviewing our past performance report.

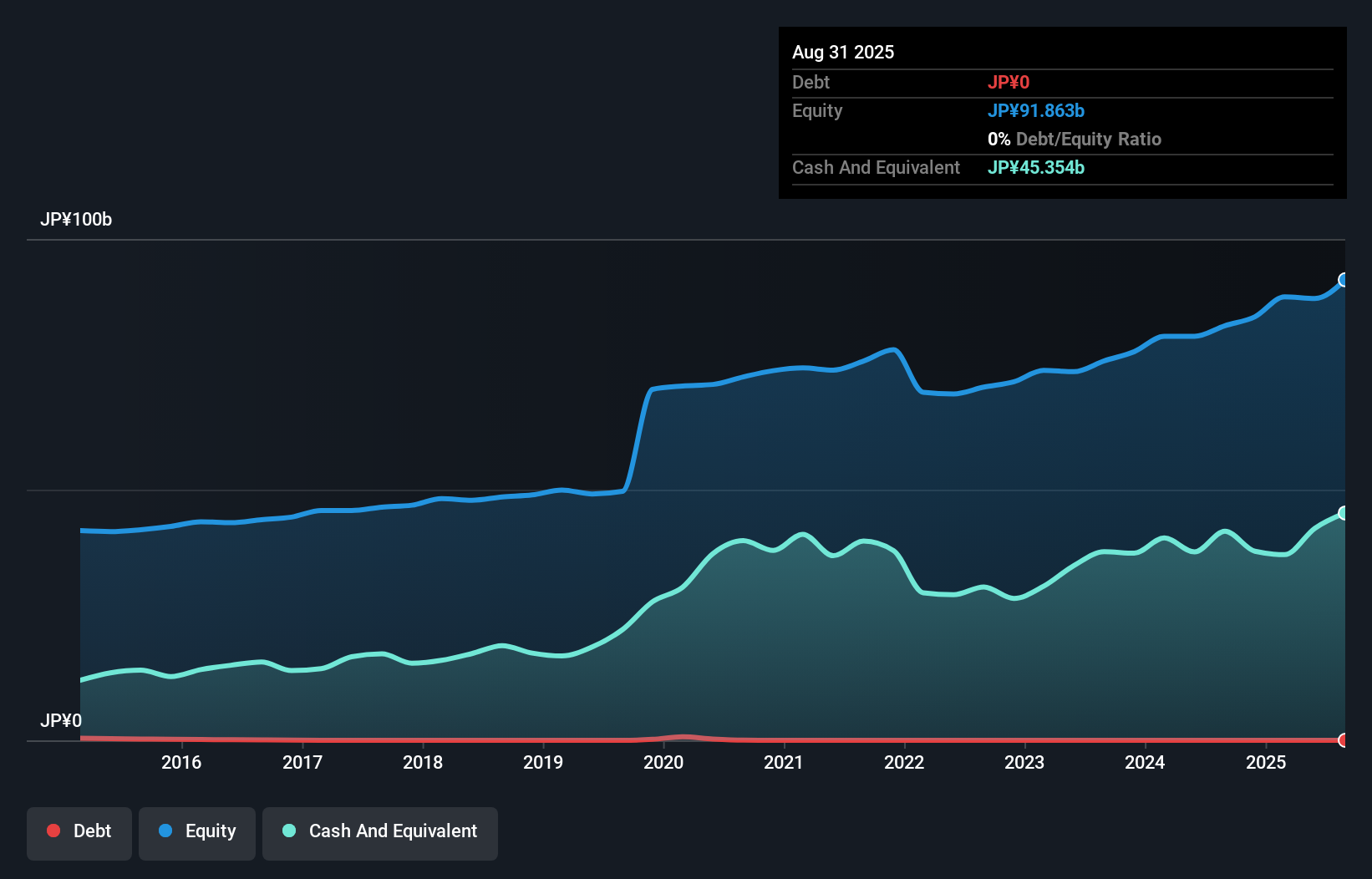

Maxvalu TokaiLtd (TSE:8198)

Simply Wall St Value Rating: ★★★★★★

Overview: Maxvalu Tokai Co., Ltd. operates and manages a chain of supermarkets in Japan with a market capitalization of ¥104.09 billion.

Operations: The company generates its revenue primarily from operating a chain of supermarkets in Japan. With a market capitalization of ¥104.09 billion, the financial performance is influenced by various cost components and profit margins.

Maxvalu Tokai, a nimble player in the retail sector, showcases impressive financial health with high-quality earnings and positive free cash flow. The company is debt-free, eliminating concerns over interest payments. Over the past year, its earnings surged by 27%, outpacing the industry average of 11%. Recent sales data reveals a robust performance with November's all-store sales at 104% and same-store sales at 103%. Trading significantly below its estimated fair value by 64%, Maxvalu Tokai seems poised for potential appreciation. This blend of solid growth metrics and attractive valuation makes it an intriguing prospect in today's market landscape.

- Get an in-depth perspective on Maxvalu TokaiLtd's performance by reading our health report here.

Gain insights into Maxvalu TokaiLtd's past trends and performance with our Past report.

Taking Advantage

- Take a closer look at our Undiscovered Gems With Strong Fundamentals list of 4633 companies by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8198

Flawless balance sheet established dividend payer.