Nihon Kohden Corporation (TSE:6849) will pay a dividend of ¥16.00 on the 27th of June. This means the annual payment is 1.5% of the current stock price, which is above the average for the industry.

Check out our latest analysis for Nihon Kohden

Nihon Kohden's Payment Could Potentially Have Solid Earnings Coverage

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Before this announcement, Nihon Kohden was paying out 80% of earnings, but a comparatively small 65% of free cash flows. In general, cash flows are more important than earnings, so we are comfortable that the dividend will be sustainable going forward, especially with so much cash left over for reinvestment.

Looking forward, earnings per share is forecast to rise by 20.5% over the next year. Under the assumption that the dividend will continue along recent trends, we think the payout ratio could be 47% which would be quite comfortable going to take the dividend forward.

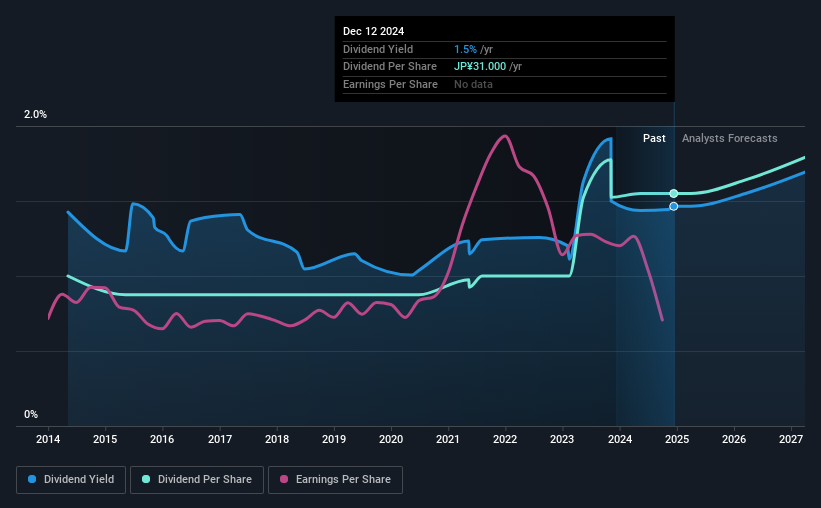

Nihon Kohden Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The annual payment during the last 10 years was ¥20.00 in 2014, and the most recent fiscal year payment was ¥31.00. This works out to be a compound annual growth rate (CAGR) of approximately 4.5% a year over that time. While the consistency in the dividend payments is impressive, we think the relatively slow rate of growth is less attractive.

Dividend Growth May Be Hard To Achieve

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. However, things aren't all that rosy. Over the past five years, it looks as though Nihon Kohden's EPS has declined at around 2.7% a year. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth. Earnings are predicted to grow over the next year, but we would remain cautious until a track record of earnings growth is established.

In Summary

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. The company has been bring in plenty of cash to cover the dividend, but we don't necessarily think that makes it a great dividend stock. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. As an example, we've identified 2 warning signs for Nihon Kohden that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Nihon Kohden might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6849

Nihon Kohden

Engages in development, manufacturing, sale, maintenance, and consultation of medical electronic equipment, and related systems and products in Japan, Americas, Europe, rest of Asia, and internationally.

Flawless balance sheet average dividend payer.