What Wel-Dish.Incorporated's (TSE:2901) 28% Share Price Gain Is Not Telling You

Despite an already strong run, Wel-Dish.Incorporated (TSE:2901) shares have been powering on, with a gain of 28% in the last thirty days. The annual gain comes to 203% following the latest surge, making investors sit up and take notice.

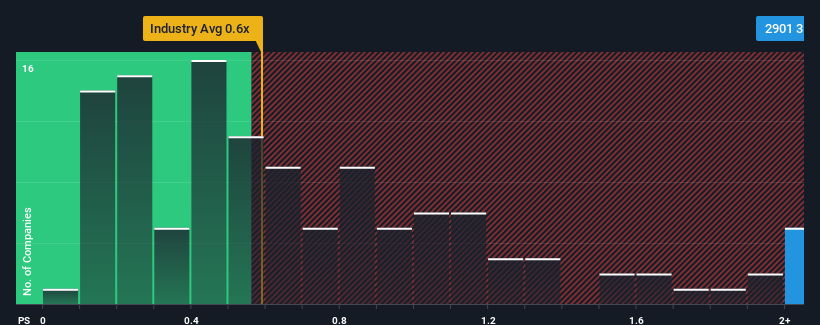

Following the firm bounce in price, you could be forgiven for thinking Wel-Dish.Incorporated is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 3.6x, considering almost half the companies in Japan's Food industry have P/S ratios below 0.6x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

Check out our latest analysis for Wel-Dish.Incorporated

How Wel-Dish.Incorporated Has Been Performing

As an illustration, revenue has deteriorated at Wel-Dish.Incorporated over the last year, which is not ideal at all. Perhaps the market believes the company can do enough to outperform the rest of the industry in the near future, which is keeping the P/S ratio high. If not, then existing shareholders may be quite nervous about the viability of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Wel-Dish.Incorporated's earnings, revenue and cash flow.How Is Wel-Dish.Incorporated's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as steep as Wel-Dish.Incorporated's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered a frustrating 25% decrease to the company's top line. As a result, revenue from three years ago have also fallen 24% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Comparing that to the industry, which is predicted to deliver 4.3% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

In light of this, it's alarming that Wel-Dish.Incorporated's P/S sits above the majority of other companies. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

What We Can Learn From Wel-Dish.Incorporated's P/S?

The strong share price surge has lead to Wel-Dish.Incorporated's P/S soaring as well. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Wel-Dish.Incorporated currently trades on a much higher than expected P/S since its recent revenues have been in decline over the medium-term. When we see revenue heading backwards and underperforming the industry forecasts, we feel the possibility of the share price declining is very real, bringing the P/S back into the realm of reasonability. Unless the the circumstances surrounding the recent medium-term improve, it wouldn't be wrong to expect a a difficult period ahead for the company's shareholders.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Wel-Dish.Incorporated, and understanding them should be part of your investment process.

If these risks are making you reconsider your opinion on Wel-Dish.Incorporated, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Wel-Dish.Incorporated might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:2901

Wel-Dish.Incorporated

Develops, manufactures, imports, and sells food and beverages primarily in Japan.

Adequate balance sheet slight.