ARIAKE JAPAN Co., Ltd. (TSE:2815) Stock Goes Ex-Dividend In Just Three Days

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see ARIAKE JAPAN Co., Ltd. (TSE:2815) is about to trade ex-dividend in the next 3 days. The ex-dividend date is two business days before a company's record date in most cases, which is the date on which the company determines which shareholders are entitled to receive a dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade can take two business days or more to settle. In other words, investors can purchase ARIAKE JAPAN's shares before the 28th of March in order to be eligible for the dividend, which will be paid on the 24th of June.

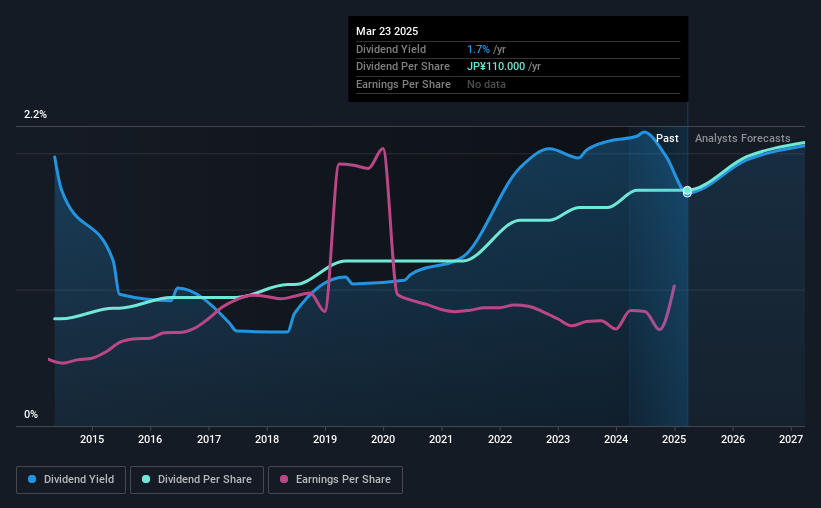

The company's next dividend payment will be JP¥90.00 per share, on the back of last year when the company paid a total of JP¥110 to shareholders. Calculating the last year's worth of payments shows that ARIAKE JAPAN has a trailing yield of 1.7% on the current share price of JP¥6440.00. If you buy this business for its dividend, you should have an idea of whether ARIAKE JAPAN's dividend is reliable and sustainable. We need to see whether the dividend is covered by earnings and if it's growing.

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. ARIAKE JAPAN paid out a comfortable 39% of its profit last year. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Fortunately, it paid out only 30% of its free cash flow in the past year.

It's positive to see that ARIAKE JAPAN's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

See our latest analysis for ARIAKE JAPAN

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. With that in mind, we're discomforted by ARIAKE JAPAN's 12% per annum decline in earnings in the past five years. Such a sharp decline casts doubt on the future sustainability of the dividend.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the last 10 years, ARIAKE JAPAN has lifted its dividend by approximately 8.2% a year on average.

The Bottom Line

Should investors buy ARIAKE JAPAN for the upcoming dividend? ARIAKE JAPAN has comfortably low cash and profit payout ratios, which may mean the dividend is sustainable even in the face of a sharp decline in earnings per share. Still, we consider declining earnings to be a warning sign. Overall, it's not a bad combination, but we feel that there are likely more attractive dividend prospects out there.

Wondering what the future holds for ARIAKE JAPAN? See what the three analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

If you're looking to trade ARIAKE JAPAN, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:2815

ARIAKE JAPAN

Manufactures, processes, and sells natural seasoning products with extracts from chicken, pork, beef, and other fresh livestock ingredients.

Flawless balance sheet with proven track record and pays a dividend.