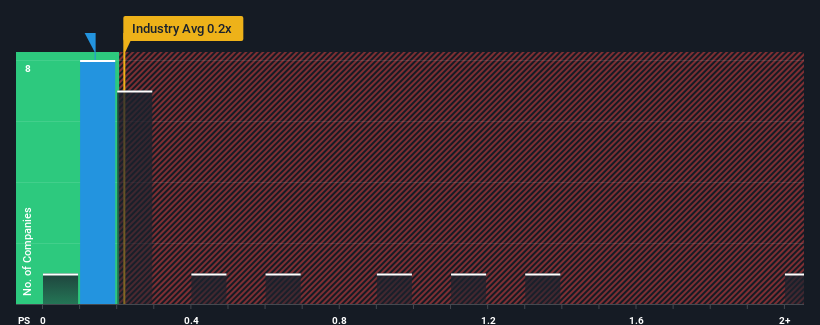

It's not a stretch to say that Nippon Seiro Co., Ltd.'s (TSE:5010) price-to-sales (or "P/S") ratio of 0.1x right now seems quite "middle-of-the-road" for companies in the Oil and Gas industry in Japan, where the median P/S ratio is around 0.2x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

See our latest analysis for Nippon Seiro

How Nippon Seiro Has Been Performing

For instance, Nippon Seiro's receding revenue in recent times would have to be some food for thought. Perhaps investors believe the recent revenue performance is enough to keep in line with the industry, which is keeping the P/S from dropping off. If you like the company, you'd at least be hoping this is the case so that you could potentially pick up some stock while it's not quite in favour.

Although there are no analyst estimates available for Nippon Seiro, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The P/S Ratio?

The only time you'd be comfortable seeing a P/S like Nippon Seiro's is when the company's growth is tracking the industry closely.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 44%. The last three years don't look nice either as the company has shrunk revenue by 2.4% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

It's interesting to note that the rest of the industry is similarly expected to decline by 1.1% over the next year, which is just as bad as the company's recent medium-term revenue decline.

With this in mind, it's no surprise that Nippon Seiro's P/S is similar to its industry peers. Nonetheless, there's no guarantee the P/S has found a floor yet with recent revenue going backwards, despite the industry heading down in unison. Maintaining these prices will be difficult to achieve as a continuation of recent revenue trends is likely to weigh down the shares eventually.

The Final Word

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Nippon Seiro revealed its three-year contraction in revenue is resulting in a P/S that matches the industry, given the industry is also set to shrink at a similar rate. Right now shareholders are comfortable with the P/S as they seem confident future revenue won't throw up any further unpleasant surprises. Although, we are concerned whether the company's performance will worsen relative to other industry players under these tough industry conditions. In the meantime, unless the company's relative performance changes, the share price should find support at these levels.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Nippon Seiro (at least 1 which makes us a bit uncomfortable), and understanding these should be part of your investment process.

If these risks are making you reconsider your opinion on Nippon Seiro, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Nippon Seiro might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:5010

Nippon Seiro

Manufactures, processes, and sells petroleum waxes, physically and chemically converted wax products, and fuel oil in Japan, North America, rest of Asia, and internationally.

Good value with acceptable track record.