Advertisement

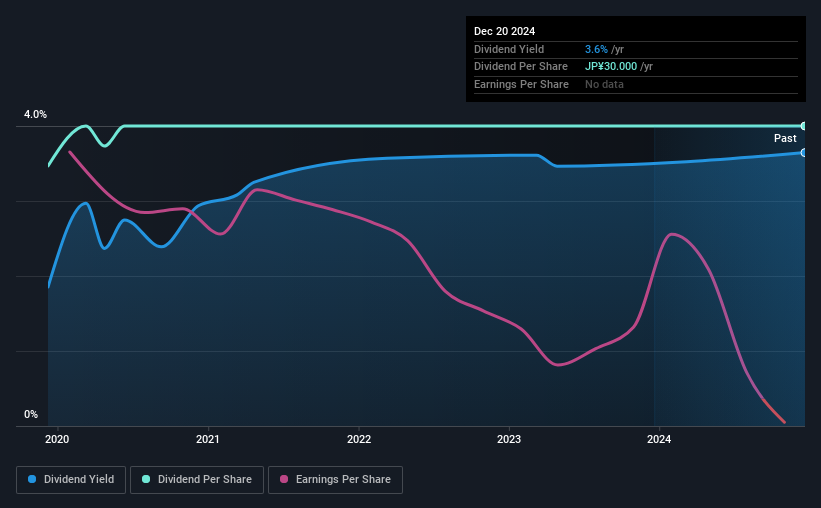

Casa Inc. (TSE:7196) has announced that it will pay a dividend of ¥30.00 per share on the 30th of April. This means the dividend yield will be fairly typical at 3.6%.

View our latest analysis for Casa

Casa's Distributions May Be Difficult To Sustain

We aren't too impressed by dividend yields unless they can be sustained over time. While Casa is not profitable, it is paying out less than 75% of its free cash flow, which means that there is plenty left over for reinvestment into the business. In general, cash flows are more important than the more traditional measures of profit so we feel pretty comfortable with the dividend at this level.

EPS has fallen by an average of 32.7% in the past, so this could continue over the next year. While this means that the company will be unprofitable, we generally believe cash flows are more important, and the current cash payout ratio is quite healthy, which gives us comfort.

Casa Is Still Building Its Track Record

Casa's dividend has been pretty stable for a little while now, but we will continue to be cautious until it has been demonstrated for a few more years. The annual payment during the last 5 years was ¥26.00 in 2019, and the most recent fiscal year payment was ¥30.00. This works out to be a compound annual growth rate (CAGR) of approximately 2.9% a year over that time. We like that the dividend hasn't been shrinking. However we're conscious that the company hasn't got an overly long track record of dividend payments yet, which makes us wary of relying on its dividend income.

The Dividend Has Limited Growth Potential

The company's investors will be pleased to have been receiving dividend income for some time. However, initial appearances might be deceiving. Casa's earnings per share has shrunk at 33% a year over the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future.

The Dividend Could Prove To Be Unreliable

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Casa's payments, as there could be some issues with sustaining them into the future. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. This company is not in the top tier of income providing stocks.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Case in point: We've spotted 3 warning signs for Casa (of which 1 is a bit concerning!) you should know about. Is Casa not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7196

Slight with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor