Ohsho Food Service (TSE:9936) has been turning heads lately after some swift changes in its share price dynamics, likely prompting investors to ask if there is something more under the surface. The company, well known for its restaurant chain presence across Japan, has not issued any major announcements or revealed unexpected news. However, the recent move is giving some market watchers pause. It is one of those moments that raise the classic question: is a shift in momentum a signal, or just market noise?

Looking at the numbers, the stock has seen a strong run, gaining nearly 39% over the past year and rising 26% year-to-date. The last three months alone delivered a healthy boost, despite a recent pullback in the past month. Broadly speaking, Ohsho Food Service’s performance looks impressive compared to many consumer-facing peers. Yet, short-term drops can challenge investors’ confidence when weighing future returns and risk.

With the stock’s powerful gains and a slight retreat on the charts, investors may be asking whether Ohsho Food Service is undervalued or if markets are already confidently pricing in whatever future growth the company has in store.

Advertisement

Price-to-Earnings of 23.3x: Is it justified?

Ohsho Food Service is currently trading at a price-to-earnings (P/E) ratio of 23.3x, just below the Japanese hospitality industry average of 23.7x. This places the company's valuation in line with peers and suggests investors are valuing its earnings similarly to other companies in the sector.

The price-to-earnings (P/E) ratio compares a company’s current share price to its per-share earnings. In the restaurant and hospitality industry, this metric helps assess how the market is pricing future growth and profitability relative to rivals. A P/E close to the industry average generally indicates the market expects the company to deliver a similar earnings trajectory to its competitors.

Ohsho Food Service’s current P/E ratio appears justified, reflecting current earnings momentum and future growth expectations that broadly match those of its industry peers.

However, if trends persist, slowing revenue and net income growth could become concerns. This introduces the possibility of investor sentiment shifting away from optimism.

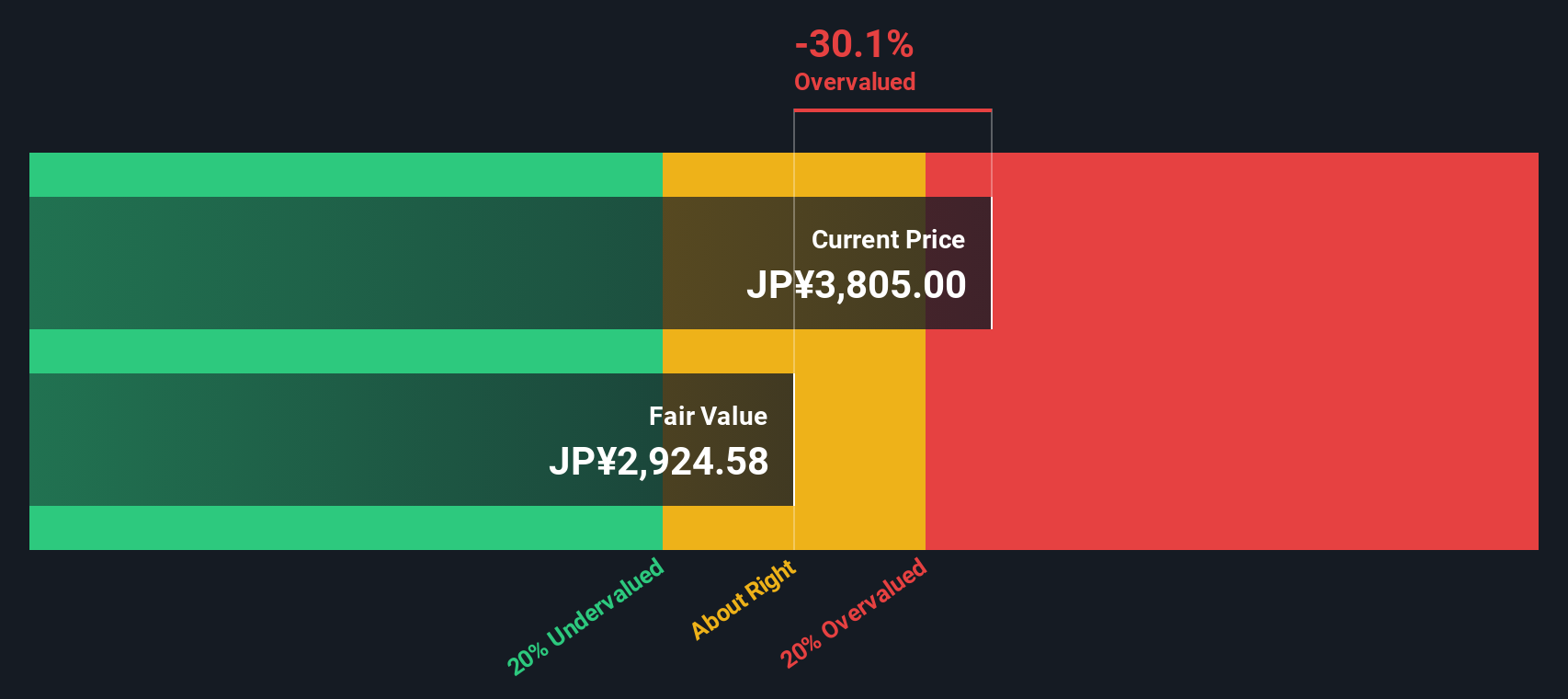

Another View: SWS DCF Model Offers a Different Perspective

Taking a step back from valuation ratios, the SWS DCF model instead looks at expected future cash flows to assess value. This approach suggests the shares may actually be overvalued at current prices, offering a contrasting outlook. Which method reflects reality best?

If you see things differently or want to dive deeper into the numbers, you can shape your own view in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Ohsho Food Service.

Ready for More Investment Opportunities?

Take charge of your portfolio. Don’t let the next big idea pass you by; these tailored stock picks could bring real growth, income, or innovation into your investments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies