- Japan

- /

- Hospitality

- /

- TSE:7604

Additional Considerations Required While Assessing UMENOHANA's (TSE:7604) Strong Earnings

Despite posting some strong earnings, the market for UMENOHANA Co., Ltd.'s (TSE:7604) stock hasn't moved much. We did some digging, and we found some concerning factors in the details.

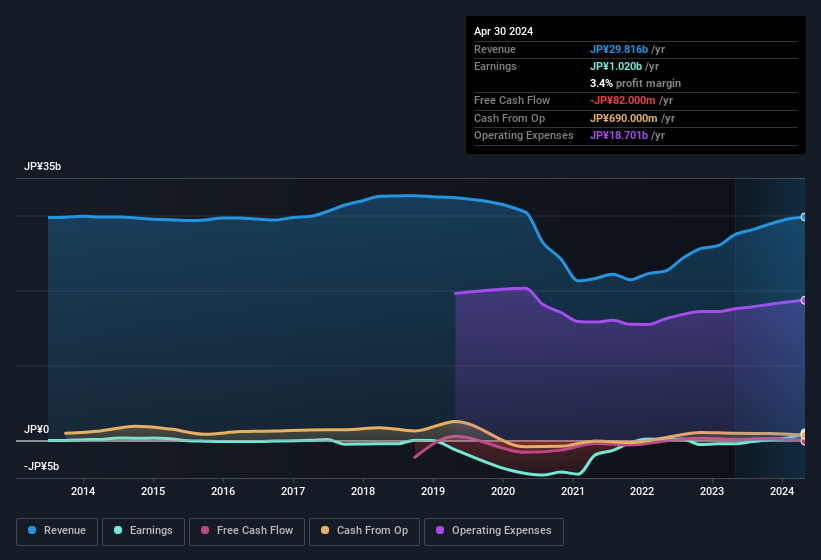

View our latest analysis for UMENOHANA

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. UMENOHANA expanded the number of shares on issue by 8.8% over the last year. As a result, its net income is now split between a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out UMENOHANA's historical EPS growth by clicking on this link.

How Is Dilution Impacting UMENOHANA's Earnings Per Share (EPS)?

UMENOHANA was losing money three years ago. And even focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). Therefore, the dilution is having a noteworthy influence on shareholder returns.

In the long term, if UMENOHANA's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of UMENOHANA.

How Do Unusual Items Influence Profit?

Finally, we should also consider the fact that unusual items boosted UMENOHANA's net profit by JP¥267m over the last year. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. And that's as you'd expect, given these boosts are described as 'unusual'. We can see that UMENOHANA's positive unusual items were quite significant relative to its profit in the year to April 2024. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On UMENOHANA's Profit Performance

To sum it all up, UMENOHANA got a nice boost to profit from unusual items; without that, its statutory results would have looked worse. And furthermore, it went and issued plenty of new shares, ensuring that each shareholder (who did not tip more money in) now owns a smaller proportion of the company. For the reasons mentioned above, we think that a perfunctory glance at UMENOHANA's statutory profits might make it look better than it really is on an underlying level. If you want to do dive deeper into UMENOHANA, you'd also look into what risks it is currently facing. For example, we've found that UMENOHANA has 4 warning signs (1 is a bit concerning!) that deserve your attention before going any further with your analysis.

Our examination of UMENOHANA has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

If you're looking to trade Umenohana GroupLtd, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7604

Umenohana GroupLtd

UMEN Umenohana Group Co.,Ltd. engages in the restaurant business in Japan.

Questionable track record unattractive dividend payer.

Market Insights

Community Narratives